Nonprofit board members and executives operate in a high-stakes environment where a single misstep can trigger lawsuits, regulatory investigations, and personal financial exposure. At Tower Insurance Associates, Inc., we’ve seen firsthand how nonprofit D&O insurance protects leaders from these mounting risks.

Your mission matters too much to let preventable legal battles derail your work. This guide walks you through what coverage you actually need and how to secure it.

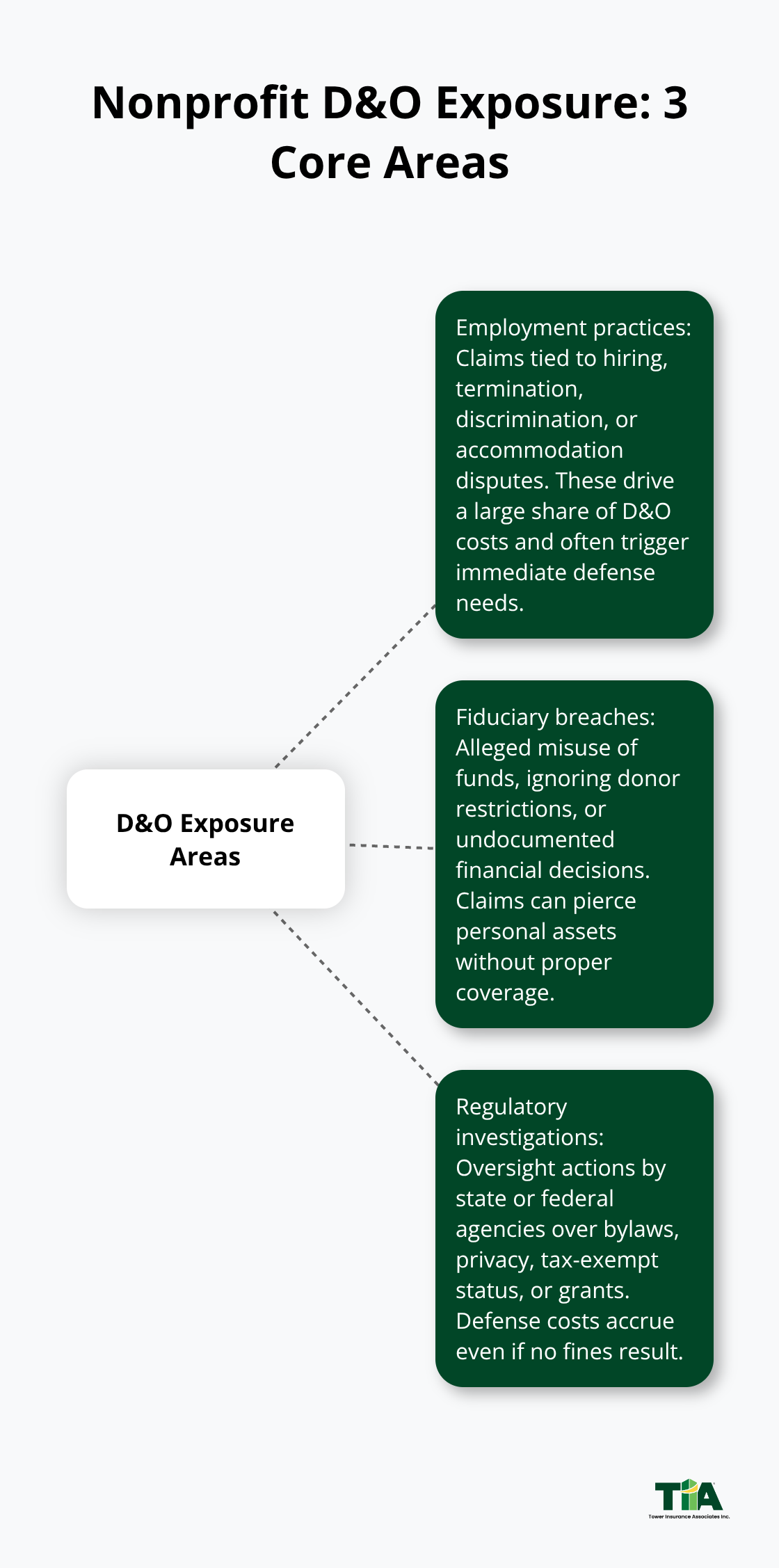

What D&O Insurance Actually Covers

D&O insurance protects nonprofit leaders from three categories of exposure that regulators, donors, and disgruntled employees actively pursue. Employment practices claims drive the largest share of D&O costs-most D&O claims are employment related.

A nonprofit director or officer can face lawsuits over hiring decisions, termination disputes, discrimination claims, or failure to accommodate staff needs. D&O coverage pays defense costs and settlements when these allegations arise, shielding personal assets from what often becomes an expensive legal battle. The average nonprofit D&O claim settles around $35,000, but roughly 10 percent of claims exceed $100,000 before settlement, making this coverage a practical safeguard rather than an optional luxury.

Employment Practices Claims Hit First

Employment practices allegations target nonprofit leaders over staff or volunteer issues with surprising frequency. A director faces personal liability when an employee claims retaliation for unpaid wages or when the organization fails to accommodate a staff member due to personal stress factors. These lawsuits can spiral quickly-defense costs alone consume thousands of dollars before any settlement occurs. D&O insurance covers these defense expenses and any resulting settlements, protecting the personal assets of board members and executives who made good-faith decisions that later face legal challenge.

Fiduciary Breaches Expose Personal Assets

Fiduciary duty violations occur when board members misuse donated funds, fail to follow donor restrictions, or make financial decisions without proper documentation and oversight. Regulators and donors scrutinize how nonprofits spend restricted gifts-if a donor specifies that money supports a specific program and leadership redirects those funds elsewhere, a fiduciary breach claim follows. D&O insurance covers defense costs and judgments in these cases, but the real protection comes from maintaining detailed financial records and board minutes that document decision-making. A single claim for breach of fiduciary duty can exceed the personal assets of directors and officers without insurance backing them, making this coverage cost-effective compared to the exposure.

Regulatory Investigations Demand Immediate Response

Regulatory investigations and fines represent a growing threat as state attorneys general and federal agencies intensify oversight of nonprofit operations. Noncompliance with bylaws, data privacy laws, tax-exempt requirements, or employment regulations can trigger costly legal action or board disqualification. D&O policies cover defense costs when agencies investigate alleged wrongdoing, whether the nonprofit ultimately faces fines or not. Cyber breaches, employment law violations, and grant compliance failures all generate regulatory exposure that nonprofit leaders often underestimate. Organizations that conduct annual risk assessments identify compliance gaps and use that information when applying for D&O coverage-insurers evaluate governance quality and risk controls when underwriting policies, and demonstrating proactive compliance helps secure better terms and lower premiums.

Understanding what D&O insurance covers sets the foundation for recognizing why nonprofit leaders face exposure that other sectors simply do not encounter. The next section examines the specific risks that make D&O protection essential for mission-driven organizations.

Why Nonprofit Leaders Face Unique Risks

Nonprofit board members and executives operate without the corporate safety nets that protect counterparts in for-profit sectors. Regulators view nonprofits with heightened scrutiny because public trust and tax-exempt status create a different accountability standard. State attorneys general increasingly investigate nonprofit operations for compliance with bylaws, data privacy laws, and employment regulations. Donors demand transparency about how their contributions are spent and will pursue legal action if restricted funds get redirected without authorization.

Personal Liability Extends Beyond Board Service

Board members carry personal liability that doesn’t disappear when they step down from their roles. A former director can face lawsuits years after leaving office if someone alleges a fiduciary breach or employment-related wrongdoing occurred during their tenure. This exposure extends beyond the organization’s finances to the personal assets of individual leaders. Without D&O insurance, a single claim for breach of fiduciary duty can exceed the personal assets of directors and officers, making this coverage cost-effective compared to the actual exposure.

Budget Constraints Create Governance Gaps

Budget constraints compound these risks because underfunded nonprofits often lack dedicated compliance staff, legal counsel, or robust financial controls. When a small nonprofit operates with a skeleton crew, governance gaps multiply. The organization might skip annual audits, fail to document board decisions properly, or miss regulatory filing deadlines simply because no one has capacity to manage these tasks. Insurers recognize this reality and adjust premiums accordingly-organizations with documented governance practices and regular financial reviews pay lower rates than those operating without formal risk controls.

Financial Pressure Drives Risky Decisions

The financial pressure to do more with less creates a dangerous incentive structure that regulators exploit in enforcement actions. A nonprofit director who redirects funds from one program to another in response to an urgent need faces fiduciary breach allegations even when motivated by mission. Employment decisions made quickly without HR documentation become discrimination claims. Grant spending that deviates slightly from approved budgets triggers compliance investigations. These situations demand immediate legal defense, and without D&O insurance, board members pay those defense costs from personal resources before any settlement or judgment occurs.

Risk Assessment Strengthens Coverage and Reduces Costs

Organizations that conduct annual risk assessments and maintain detailed financial records demonstrate to insurers that they take governance seriously, which translates to better coverage terms and lower premiums. This approach protects both the organization’s mission and the personal financial security of the leaders who drive that mission forward. The specific risks your nonprofit faces depend on your size, programs, and operational complexity-which is why selecting the right D&O policy requires a clear understanding of your organization’s actual exposure.

How to Choose the Right D&O Policy for Your Organization

Map Your Nonprofit’s Specific Risks First

Start by mapping your nonprofit’s specific governance and operational risks before comparing policies. A youth-serving organization faces different D&O exposures than a health clinic or arts nonprofit-your risk profile determines what coverage limits and endorsements you actually need. Conduct a risk assessment by reviewing your past three years of board minutes, employment decisions, financial transactions, and any regulatory interactions. This exercise reveals where your organization faces the highest exposure.

Identify which claims scenarios would hurt most: employment disputes with staff, donor restriction violations, data privacy breaches, or regulatory investigations. Organizations with documented governance practices and regular financial reviews pay lower premiums than those without formal risk controls, so the assessment itself becomes a cost-reduction tool.

Understand Policy Limits and Structure

Most nonprofit D&O policies operate on a claims-made basis with a retroactive date-this means the policy covers claims reported during the policy period for incidents that occurred after the retroactive date. If your retroactive date doesn’t match prior acts, you create a coverage gap for older incidents. Defense costs can be paid either inside or outside the policy limit; outside-the-limit defense is superior because it preserves your full limit for settlements and judgments.

Policy limits typically start at $1 million with aggregate limits up to $2 million, and umbrella options reach $5 million for higher-exposure programs. However, the right policy for your organization depends on factors like annual budget, number of employees, volunteer scale, and program complexity. A nonprofit with $2 million in annual revenue and ten staff members typically needs different coverage than one operating on $20 million with fifty employees across multiple locations.

Review Exclusions and Required Endorsements

Review exclusions carefully because standard policies exclude fraud, illegal acts, and certain professional services. Employment-related allegations represent 85% of Non-Profit Directors & Officers Liability claims, so verify that your policy covers these claims without broad exclusions.

If your nonprofit operates employee benefit plans or retirement accounts, add fiduciary liability coverage or an ERISA sublimit to protect against pension-related claims.

For organizations handling beneficiary interactions or managing volunteers, confirm that third-party harassment coverage is included. This protection matters because mission-driven organizations interact with vulnerable populations and face unique exposure from these relationships.

Partner with Nonprofit-Focused Insurance Advisors

Work exclusively with insurance advisors who specialize in nonprofit governance risks rather than generalist brokers. Ask prospective advisors about their experience with organizations similar to yours in size and mission, request references from current nonprofit clients, and confirm they represent carriers with A-rated financial strength. The advisor should discuss how your governance practices affect premiums and offer practical risk management resources.

When you meet with insurance advisors, bring your risk assessment findings along with audited financial statements, current bylaws, employee handbook, conflict-of-interest policies, and details about any prior claims or regulatory contact. Insurers evaluate these documents during underwriting to confirm that coverage aligns with your actual risk.

Schedule Annual Policy Reviews

Schedule policy reviews annually as your nonprofit’s programs and staffing evolve. Changes in employee count, new program launches, or expanded volunteer roles may require higher limits or additional endorsements. This proactive approach prevents coverage gaps and keeps your protection aligned with your organization’s current operations.

Final Thoughts

Nonprofit D&O insurance protects mission-driven leaders from the financial devastation that a single governance claim inflicts. Without this coverage, board members and executives face personal liability that threatens their savings and retirement accounts. Defense costs alone reach thousands of dollars before any settlement occurs, and roughly 10 percent of nonprofit D&O claims exceed $100,000, making this protection essential for your leadership team’s financial security.

Start with a risk assessment that reviews your board minutes, employment decisions, and financial records from the past three years. Gather your audited financial statements, bylaws, employee handbook, and conflict-of-interest policies before meeting with insurance advisors (these documents help insurers confirm that coverage aligns with your actual risk profile). Partner with an insurance advisor who specializes in nonprofit governance and request references from current nonprofit clients in your sector.

We at Tower Insurance Associates, Inc. understand the unique pressures nonprofit leaders face and help organizations secure tailored nonprofit D&O insurance coverage that fits their mission and budget. Contact us today to discuss how D&O insurance protects the leaders who drive your organization forward.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.