California’s corporate leaders face mounting legal and financial risks that can threaten both their companies and personal wealth. Directors and officers insurance in California has become essential protection against lawsuits, regulatory actions, and defense costs that can quickly spiral out of control.

At Tower Insurance Associates, Inc., we’ve seen firsthand how the right coverage shields leadership teams from devastating financial exposure. This guide walks you through what this insurance covers, why it matters in California’s complex business environment, and how to select the right policy for your organization.

What Directors and Officers Insurance Actually Covers

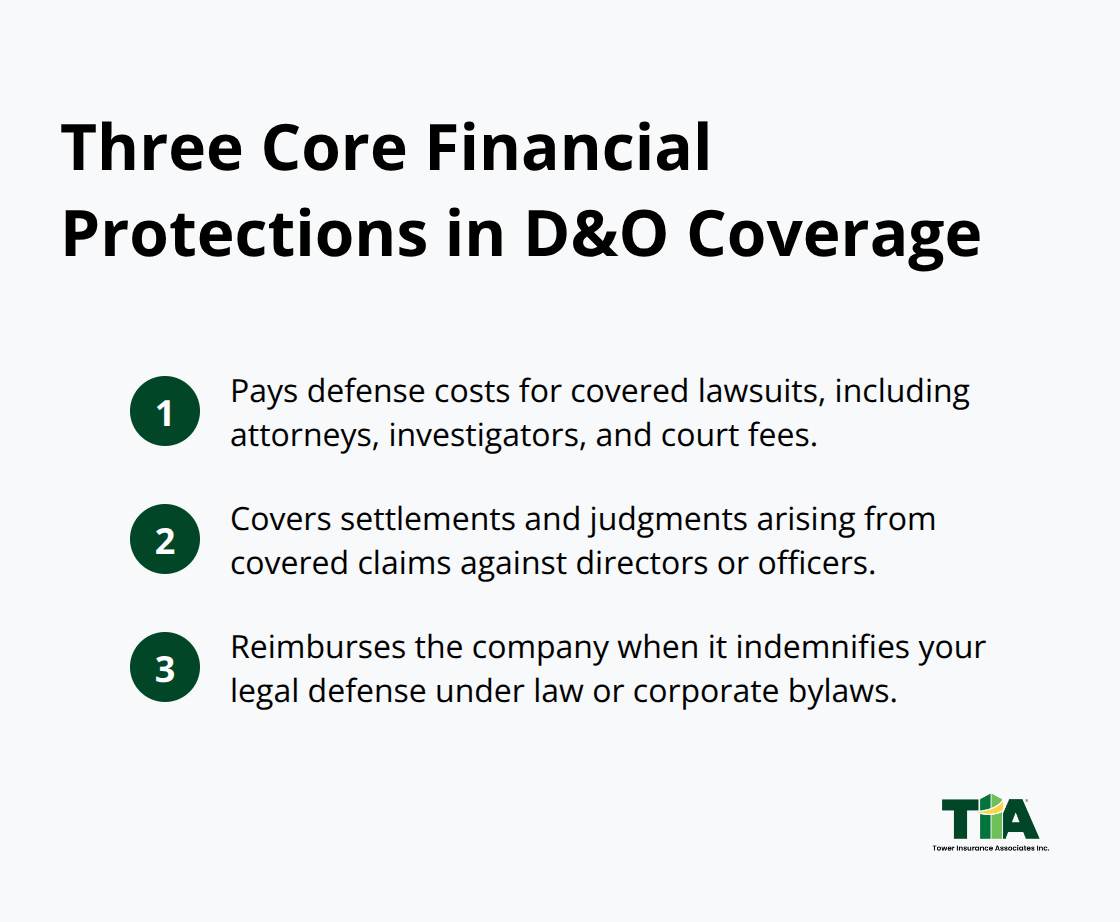

Three Core Financial Protections

Directors and officers insurance protects your personal assets when leadership decisions create legal exposure. The coverage responds to three distinct financial threats that California executives face regularly. First, it covers defense costs when you face a lawsuit for alleged wrongdoing in your role as a director or officer-this includes attorney fees, investigator expenses, and court costs that accumulate quickly in complex litigation.

Second, it pays settlements and judgments if you face liability for covered claims, protecting your personal wealth from seizure to satisfy a judgment. Third, it reimburses your company when the organization must cover your legal defense or indemnify you under state law or corporate bylaws, which happens frequently when boards lack sufficient personal resources to fund their own defense.

What Your Policy Actually Covers

The scope of what your policy covers depends entirely on policy language, so specifics matter tremendously. Typical policies cover bad investment decisions, alleged conflicts of interest, inappropriate personnel decisions, unauthorized data breaches, and acts of gross negligence-essentially unintentional errors in judgment made in good faith. However, policies explicitly exclude criminal acts, willful wrongdoing, and illegal conduct, so coverage applies only when you acted without intent to harm. A critical distinction: policies don’t cover simply bad business decisions made in good faith that happen to fail financially, nor do they cover defense costs for criminal charges.

California’s “On Behalf Of” Standard Changes Everything

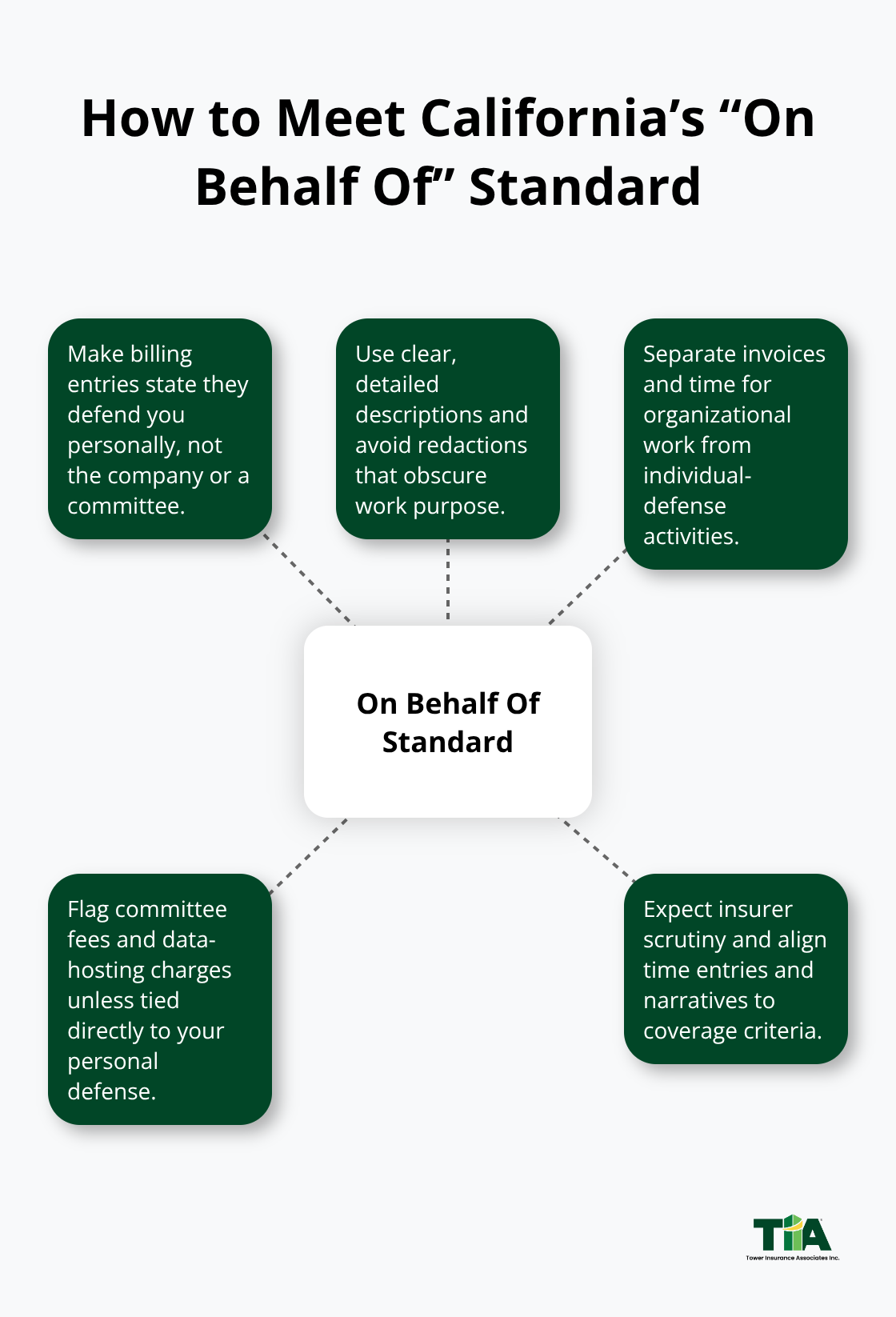

In California specifically, a 2025 ruling fundamentally altered how insurers interpret defense cost coverage. The court held that defense costs must be incurred directly on behalf of directors and officers to qualify for coverage-not on behalf of committees or the company itself. This means your billing descriptions and time entries must clearly document that costs were generated to defend you personally, not to protect the organization. The ruling emphasizes that redacted or vague billing entries face scrutiny from insurers, so maintaining detailed, non-redacted documentation of every legal expense is essential for claims approval.

This distinction matters because the court denied coverage for special committee fees and data hosting costs that lacked a clear connection to your personal defense. If your organization faces a covered claim, ensure that all billing entries specify exactly how each cost benefits you as a director or officer. Vague descriptions or redacted time entries will likely trigger coverage disputes and delay reimbursement when you need it most.

Moving Forward With Your Coverage Strategy

Understanding what your policy covers-and what it excludes-positions you to make informed decisions about your organization’s risk exposure. The next step involves assessing whether your current coverage limits and deductibles actually match the threats your leadership team faces in California’s evolving business environment.

Why California Leaders Face Growing Personal Liability Risk

Employment Decisions Trigger Personal Liability Claims

California’s litigation environment holds corporate leadership personally accountable for decisions made in their governance roles. Employment-related D&O claims frequently stem from board-driven hiring or firing decisions, perceived internal politics, and governance errors that seem minor until they trigger lawsuits. The Mark Thompson case, reported by The New York Times in 2016, illustrated how a single personnel decision can escalate into personal liability for executives. Beyond employment disputes, investor lawsuits represent a major D&O risk when funding structures fail to meet expectations or when executives withhold material information from shareholders. Fortune Magazine documented the GoPro investor lawsuit, where shareholders alleged that executives masked information that harmed the company’s valuation. These cases demonstrate that California courts hold directors personally accountable for governance failures and disclosure gaps, even when the underlying business decisions seemed reasonable at the time.

Regulatory Obligations Have Expanded Significantly

California’s regulatory environment creates mounting pressure on leadership teams. Since the Delaware Supreme Court’s Marchand v. Barnhill decision in 2019, boards must implement reporting mechanisms for monitoring mission-critical operations. The Boeing derivative lawsuit settlement of $237.5 million in November 2021 revealed the financial and governance costs of lacking robust monitoring for critical operations like flight safety. Wells Fargo and Abbott Laboratories face ongoing oversight breach cases that show courts persistently scrutinize board governance and hold directors liable after red flags are missed. ESG activism continues to pressure boards, with regulators scrutinizing environmental and social disclosures and investigating potential greenwashing. AI adoption introduces new governance risks as boards must balance technology adoption with ethical controls and prevent AI washing-where companies make unsubstantiated claims about AI capabilities. Beyond traditional governance challenges, cyberattacks have affected thousands of companies and government agencies, with California’s strict data privacy laws making compliance failures costly. These evolving obligations mean that directors and officers in California cannot rely on traditional governance practices alone.

Personal Assets Face Direct Exposure

California law permits shareholders and employees to pursue personal liability claims against directors and officers, exposing their savings, investments, and property to seizure. Without D&O insurance, you personally fund your legal defense even before a verdict is reached. Defense costs alone can reach hundreds of thousands of dollars in complex litigation involving securities claims or employment disputes. Your company may be unable or unwilling to indemnify you under its bylaws or state law, leaving you to shoulder the entire burden. The 2025 California court ruling on the “on behalf of” standard means that even when your company attempts to cover defense costs, insurers scrutinize billing entries and may deny reimbursement for costs deemed to benefit the organization rather than you personally. This creates a coverage gap where you face both the risk of personal liability and the risk that promised company reimbursement will be disputed or denied.

How Coverage Protects Your Financial Position

D&O insurance closes this gap by guaranteeing that your defense costs and any judgment receive coverage directly, without depending on your company’s financial health or willingness to indemnify. The right policy responds to the specific threats California leaders face-from employment disputes to investor claims to governance oversights-and protects your personal assets when your leadership decisions create legal exposure. Understanding your organization’s risk profile and selecting appropriate coverage limits becomes the next critical step in building a comprehensive protection strategy.

Selecting Coverage That Matches Your California Risk

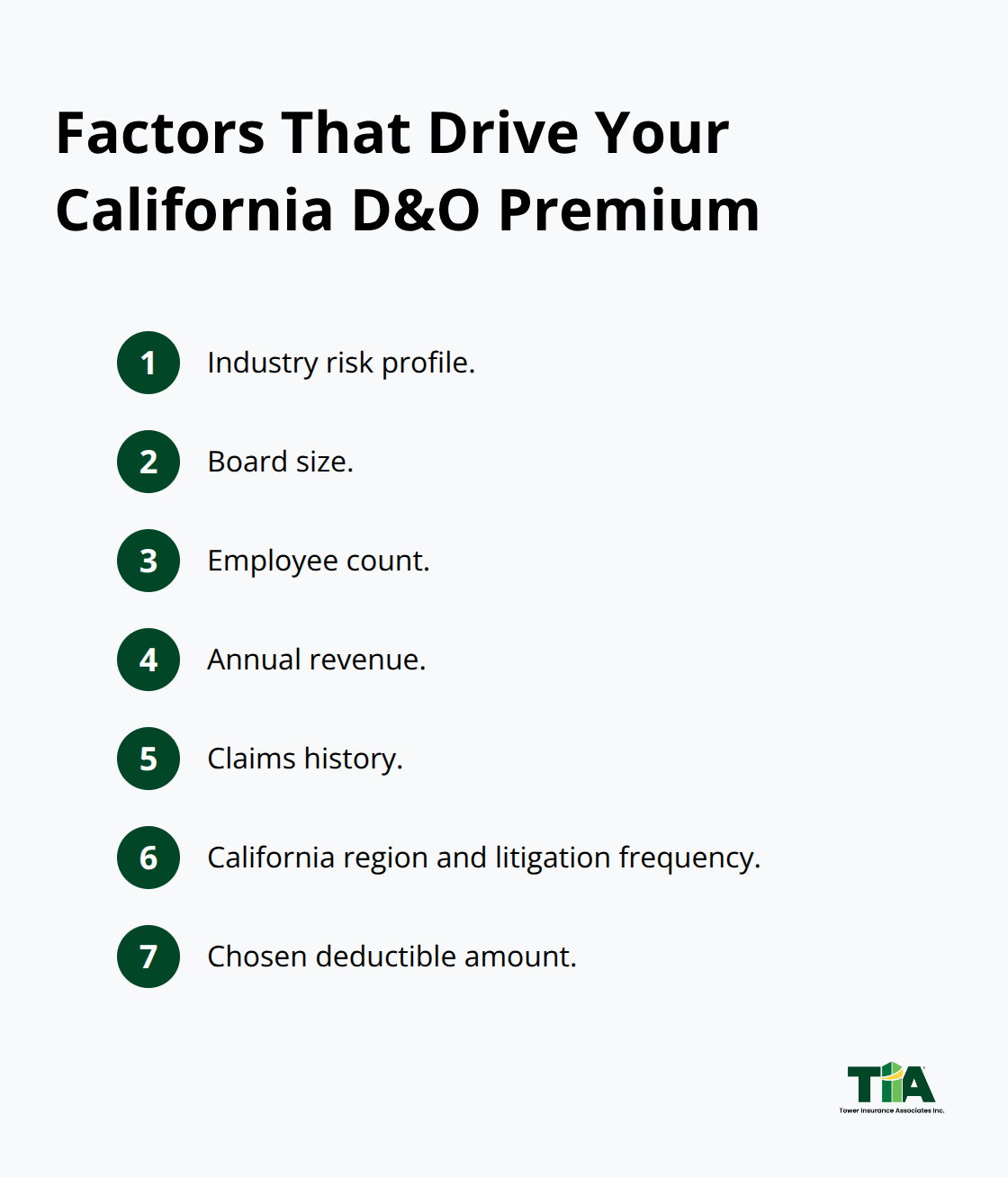

The typical D&O premium for small businesses runs about $138 per month according to industry data, but that figure masks enormous variation based on your specific situation. These differences reflect real risk differences, not arbitrary pricing, which means your first step involves honest assessment of where your organization actually sits on the risk spectrum. Start with your industry, board size, employee count, annual revenue, and claims history because insurers weight each factor heavily when calculating premiums. A manufacturing firm with 50 employees and $10 million in revenue faces fundamentally different exposure than a tech startup with 15 employees and $2 million in revenue, even if both operate in California.

Your location within California matters too since some regions experience higher litigation frequency than others, directly affecting your premium. The deductible you choose drives your monthly cost significantly, with most customers selecting around $2,500, though your company’s financial position should determine whether you can comfortably absorb that amount if a claim hits.

Matching Coverage Limits to Your Actual Exposure

Coverage limits come in two forms: per-occurrence limits that cover a single claim and aggregate limits that cap total claims in a year. You need both figures high enough to cover a realistic worst-case scenario for your organization. If your company faces potential investor lawsuits, employment disputes, and governance challenges simultaneously, aggregate limits become critical because multiple claims can exhaust per-occurrence limits quickly. California’s evolving regulatory environment means that legal defense alone can consume significant resources in complex litigation before any settlement or judgment. Consider your company’s ability to indemnify you under corporate bylaws or California law if insurance falls short, because that gap becomes your personal liability.

Reducing Premiums Through Proactive Risk Management

Proactive risk management directly reduces your premiums, with documented governance practices like formal decision processes, HR training programs, anti-harassment policies, and clear compliance protocols signaling lower risk to underwriters. A clean claims history matters enormously since companies with prior D&O claims pay significantly higher premiums than those with no history, making risk prevention your best cost-control strategy. Strong governance demonstrates to insurers that your organization takes fiduciary duties seriously and implements controls to prevent the types of claims that trigger expensive litigation. Companies that maintain detailed records of board decisions, document policy implementation, and respond promptly to potential compliance issues typically qualify for better rates than those with reactive governance structures.

Working With an Independent Broker to Find Competitive Pricing

Working with an independent insurance broker rather than a captive agent tied to a single carrier gives you access to multiple insurers and competitive quotes that reveal real market pricing. Independent brokers specializing in D&O coverage understand California’s specific regulatory requirements and can identify coverage gaps that general brokers miss. Tower Insurance Associates, Inc., an independent agency in Culver City, California, represents multiple top-rated carriers and can help you compare options across different insurers to find pricing and terms matching your organization’s risk profile. Getting quotes from at least three different carriers lets you see how different underwriters assess your risk and price accordingly, revealing whether you’re paying market rates or overpaying for similar coverage. Your broker should help you understand Side A, Side B, and Side C coverage variations so you know exactly who gets protected and how claims get paid rather than discovering gaps when you need the coverage.

Structuring Your Coverage for Maximum Protection and Savings

The cost-saving strategy of bundling D&O with other management liability coverages like employment practices liability insurance often yields meaningful discounts while closing protection gaps that standalone D&O policies leave open. Paying annual premiums upfront rather than monthly installments typically reduces your total cost, so factor that into your budget if your cash flow allows. California’s changing litigation landscape and evolving board governance obligations mean you should review your coverage annually rather than every three years, which keeps your limits and exclusions aligned with your actual risk exposure as your organization grows or faces new regulatory requirements.

Final Thoughts

Directors and officers insurance in California protects your personal assets from the legal and financial fallout of leadership decisions. The coverage responds to employment disputes, investor claims, governance oversights, and regulatory failures that California courts increasingly hold directors personally accountable for. Your defense costs alone can reach hundreds of thousands of dollars in complex litigation, and without proper coverage, you face that burden directly regardless of whether you ultimately prevail.

Selecting the right coverage requires honest assessment of your organization’s risk profile, industry exposure, board size, employee count, and claims history. Proactive governance practices like formal decision processes, documented HR policies, and compliance protocols directly reduce your premiums by signaling lower risk to underwriters. A clean claims history matters enormously since prior D&O claims significantly increase future premiums, making risk prevention your best cost-control strategy.

We at Tower Insurance Associates, Inc. represent multiple top-rated carriers and specialize in tailoring directors and officers insurance in California to match your organization’s specific risk exposure. Contact Tower Insurance Associates, Inc. to request competitive quotes from multiple carriers and discover how much your premiums could decrease through proactive risk management. Your leadership team deserves protection that matches the real threats California’s business environment creates.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.