Your leadership team faces real legal and financial risks every day. Directors and officers can be personally liable for company decisions, even when they act in good faith.

At Tower Insurance Associates, Inc., we see how LA D&O liability insurance protects business leaders from devastating personal losses. This guide walks you through what coverage you need and how to find the right policy for your company.

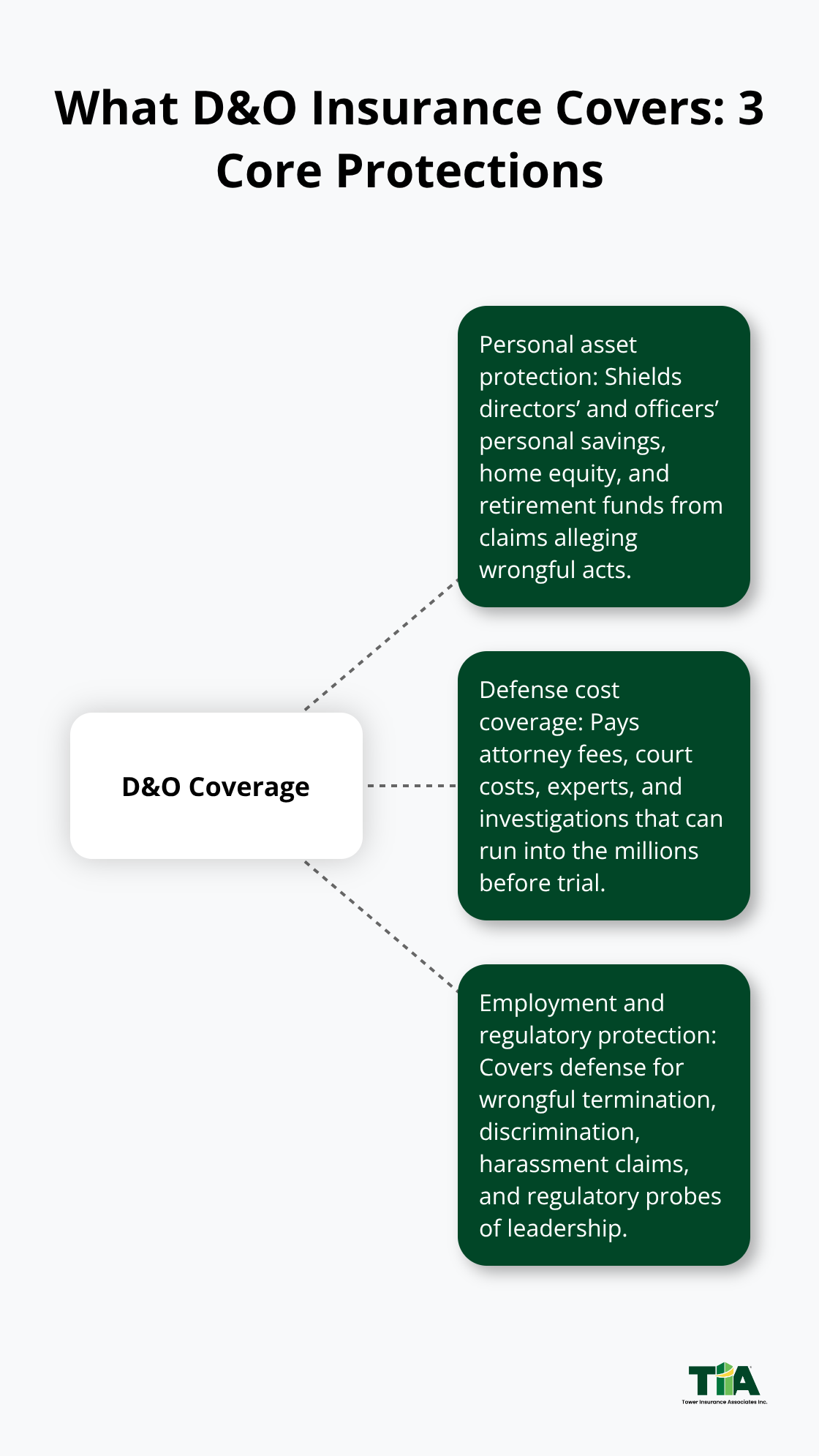

What D&O Insurance Actually Covers

D&O liability insurance protects your directors and officers from personal financial devastation when lawsuits target their leadership decisions. The policy covers three core areas that matter most to LA business leaders.

Personal Asset Protection Against Wrongful Acts

First, it shields personal assets when someone sues a director or officer for alleged wrongful acts-things like breach of fiduciary duty, mismanagement of company funds, or poor strategic decisions. Without this protection, leaders face the risk of personal bankruptcy even when the company has assets. A single lawsuit can threaten retirement accounts, home equity, and personal savings that have nothing to do with the company’s operations.

Defense Costs That Add Up Fast

Second, D&O covers defense costs, which is where the real money goes. Legal defense in a shareholder lawsuit or regulatory investigation easily runs $500,000 to $2 million before trial, according to industry data on corporate litigation expenses. Your policy pays attorney fees, court costs, expert witness fees, and investigative expenses so your leadership team doesn’t personally fund their own defense. This coverage matters because most directors and officers cannot absorb these costs without severe personal financial strain.

Employment Claims and Regulatory Investigations

Employment practices liability is now a standard part of D&O coverage, and it’s essential because wrongful termination, discrimination, and harassment claims against company leaders are exploding. California employment law is notoriously employee-friendly, and juries award substantial damages in these cases. A single employment claim costs $100,000 to $500,000 in defense and settlement expenses. Your D&O policy covers the legal defense when an employee sues a director or officer personally for these employment-related wrongful acts, which happens far more often than most LA business owners realize.

Regulatory investigations also fall under modern D&O coverage. If the SEC, California Department of Fair Employment and Housing, or another state agency investigates your leadership, the policy covers investigative costs and legal representation during the probe. This matters because regulatory defense costs accumulate quickly and can stretch into the hundreds of thousands before any settlement or resolution occurs. Your leaders need protection that covers both the investigation phase and any resulting claims.

Understanding what your D&O policy actually covers is only half the battle-knowing whether your company truly needs this protection is what separates prepared leadership teams from those caught off guard.

Why LA Businesses Face Real D&O Liability Risks

Shareholder and Employment Litigation Accelerates Against Leadership

Litigation against company leaders in Los Angeles has accelerated dramatically over the past decade. Shareholder lawsuits, employment disputes, and regulatory investigations target directors and officers as routine business risks that strike companies regardless of size or industry. California courts have consistently expanded liability standards for corporate leaders, making it easier for plaintiffs to file claims and harder for defendants to win early dismissals. A single wrongful termination claim against a director costs $150,000 to $400,000 in defense expenses alone, even before settlement or judgment. When employment claims combine with shareholder derivative suits or breach of fiduciary duty allegations, defense costs multiply rapidly. The State Bar of California reports that employment-related litigation surged 35 percent since 2015, and LA County courts handle a disproportionate share of these cases due to the region’s concentration of large employers and sophisticated plaintiff’s counsel. Your directors and officers cannot afford to ignore this trend.

California’s Aggressive Regulatory Investigations

California’s regulatory environment creates additional pressure on leadership teams that most LA business owners underestimate. The California Department of Fair Employment and Housing, Securities and Exchange Commission, California Labor Commissioner, and state attorney general’s office all investigate company leaders for alleged violations ranging from wage theft to securities fraud to discrimination. These investigations alone cost $200,000 to $750,000 in legal fees and expert costs before any settlement reaches completion. Unlike federal agencies, California regulators frequently pursue individual officers personally, not just the company. This means your CFO, CEO, or board members face personal liability for regulatory violations even when they acted on advice from counsel. The state’s strict liability standards for employment law violations mean that good-faith business decisions offer minimal protection.

Personal Assets Remain Vulnerable Without Coverage

Your leadership team’s personal assets-homes, investments, savings accounts-remain at risk unless D&O coverage explicitly protects them from regulatory and litigation threats. A director’s retirement account or home equity can vanish to pay legal defense costs that accumulate during investigations and lawsuits. Most LA company leaders fail to recognize that personal liability follows them even after they leave the company (many policies offer retroactive coverage for acts that occurred before the policy period if a claim is made during the policy period). The financial devastation from regulatory defense costs drains personal bank accounts and retirement savings faster than most executives anticipate. Your leadership team faces exposure that standard business insurance does not address, which is why understanding your D&O protection gap matters before a lawsuit or investigation arrives.

Why Coverage Gaps Create Catastrophic Exposure

Directors and officers who lack adequate D&O coverage face personal bankruptcy from litigation costs alone, regardless of whether they ultimately win or lose the case. Defense expenses accumulate before any verdict or settlement, forcing leaders to choose between personal financial ruin and inadequate legal representation. California’s plaintiff-friendly courts and aggressive regulatory agencies mean that LA business leaders operate in one of the nation’s highest-risk environments for personal liability claims. The combination of employment law exposure, shareholder litigation risk, and regulatory investigation costs creates a perfect storm that catches unprepared leadership teams off guard. Choosing the right D&O policy requires understanding your company’s specific risk profile and matching that exposure to appropriate coverage limits and deductibles.

Selecting the Right D&O Coverage for Your LA Business

Identify Your Company’s Specific Risk Profile

Your company’s D&O insurance needs vary dramatically based on your business structure and operations. A tech startup with five board members faces entirely different exposures than a manufacturing company with thirty years of operations and a complex shareholder structure. Identify your company’s specific risk triggers to match coverage to actual threats. If your directors make frequent acquisitions, shareholder litigation exposure skyrockets. If you operate in healthcare or financial services, regulatory investigation costs become your primary concern. If you employ over fifty people, employment practices claims represent your biggest threat.

Understand Pricing and Coverage Limits

Mid-sized private companies in LA typically face annual D&O premiums between $25,000 and $45,000 for $50 million in revenue, while smaller firms pay around $5,000 annually and large public companies exceed $100,000. These numbers reflect industry standards, but your actual cost depends on whether your company has faced prior claims, how many directors and officers need coverage, and whether your industry attracts regulatory scrutiny. Different insurers price the same risk differently based on their claims experience and underwriting philosophy. One carrier might charge $30,000 for coverage while another quotes $50,000 for identical limits, simply because their portfolio data suggests different risk patterns in your industry.

Coverage limits matter more than premium price. A $5 million policy sounds adequate until you face a single shareholder derivative suit with $8 million in defense costs before trial. California companies should carry minimum limits of $10 million for Side A coverage, which protects directors and officers personally. Side B coverage, which reimburses the company for indemnified individuals, should match your Side A limits. Side C entity coverage protects the company from securities claims and shareholder disputes.

Most LA companies underestimate their deductible tolerance. A $50,000 deductible saves premium dollars but forces your leadership team to absorb that cost before coverage activates. When a regulatory investigation costs $200,000 in legal fees, that $50,000 deductible means your company or leaders fund the first quarter of defense expenses out of pocket. A $25,000 deductible typically makes more sense for private companies because it balances cost savings against real financial exposure.

Read Exclusions and Endorsements Carefully

Comparing policies requires reading the actual exclusions and endorsements, not just the summary sheet. Standard D&O policies exclude criminal acts, intentional misconduct, bodily injury, and property damage. But exclusions differ significantly across carriers regarding contract disputes, prior known conditions, and regulatory violations. One insurer might exclude all contract-related claims while another covers breach of contract claims that also involve fraud.

Exclusion language creates coverage gaps that policyholders should challenge rather than accept at face value. Courts have found that exclusions do not automatically bar coverage for all claims when some causes of action contain non-excluded elements like fraud. This shows the importance of understanding how your specific policy language applies to your actual exposures.

Partner with an Independent Insurance Agent

Work with an independent insurance agent who represents multiple carriers and understands LA’s specific business environment. Your agent should analyze your company’s board structure, industry classification, prior claims history, and regulatory exposure before recommending coverage. An agent familiar with California employment law knows that discrimination and harassment claims against directors cost substantially more to defend than similar claims in other states. An agent with experience in your specific industry recognizes emerging risks before they become problems. An independent agent representing multiple top-rated carriers can match your company’s unique risk profile to the right policy at competitive pricing.

Conclusion

LA D&O liability insurance protects your leadership team from personal financial devastation when lawsuits and regulatory investigations strike. The coverage addresses real threats that standard business insurance ignores: defense costs that reach $500,000 to $2 million, employment claims that drain personal assets, and regulatory investigations that target individual officers. Your directors and officers cannot make bold strategic decisions when they fear personal bankruptcy from litigation expenses.

Coverage limits matter more than premium savings, and exclusion language determines whether your policy actually covers the claims you face. A $10 million Side A limit protects personal assets adequately for most LA private companies, while Side B and Side C coverage shield the company from shareholder disputes and securities claims. Request quotes from at least two carriers because pricing varies dramatically for identical coverage.

Contact an independent insurance agent who represents multiple carriers and understands California’s aggressive regulatory environment and plaintiff-friendly courts. Your agent should analyze your board structure, industry classification, and prior claims history before recommending specific limits and deductibles. We at Tower Insurance Associates, Inc. help LA business leaders find tailored D&O coverage that matches their actual risk exposure at competitive pricing.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.