One lawsuit can drain your business bank account and damage your reputation for years. At Tower Insurance Associates, Inc., we see small business owners underestimate how vulnerable they are to professional liability claims.

Your clients trust you with their money, their projects, and their success. Without the right coverage, a single error or missed deadline could cost you everything you’ve built.

What Professional Liability Actually Covers

Professional liability insurance protects your business when a client claims you made a mistake that cost them money. This isn’t about someone slipping on your office floor or damaging their property-general liability covers those situations. Professional liability specifically addresses errors, omissions, and negligence in the services you provide.

Real Examples of Professional Liability Claims

A bookkeeper’s clerical error costs a client thousands. A web developer’s code mistake causes lost sales. An accountant’s incorrect tax return creates tax penalties. All of these fall under professional liability coverage. The Hartford reports that standalone professional liability policies for small businesses average about $76 monthly, but costs vary significantly based on your industry and risk profile. Architects and engineers typically pay around $239 monthly, while healthcare professionals average $38 monthly and technology companies around $146 monthly. This variation reflects how directly you interact with clients and the financial consequences when things go wrong.

Legal Defense Costs You Cannot Ignore

One critical aspect many small business owners overlook is that professional liability covers your legal defense costs, not just settlements or judgments. If a client sues you and you win, your insurer still pays the attorneys, court fees, expert witnesses, and other defense expenses. Litigation costs accumulate fast. Most professional liability policies include a right and duty to defend, meaning the insurance company manages your legal defense from the start, which removes that burden from you during an already stressful situation. Without this coverage, you’d pay these costs out of pocket regardless of whether you ultimately win the case.

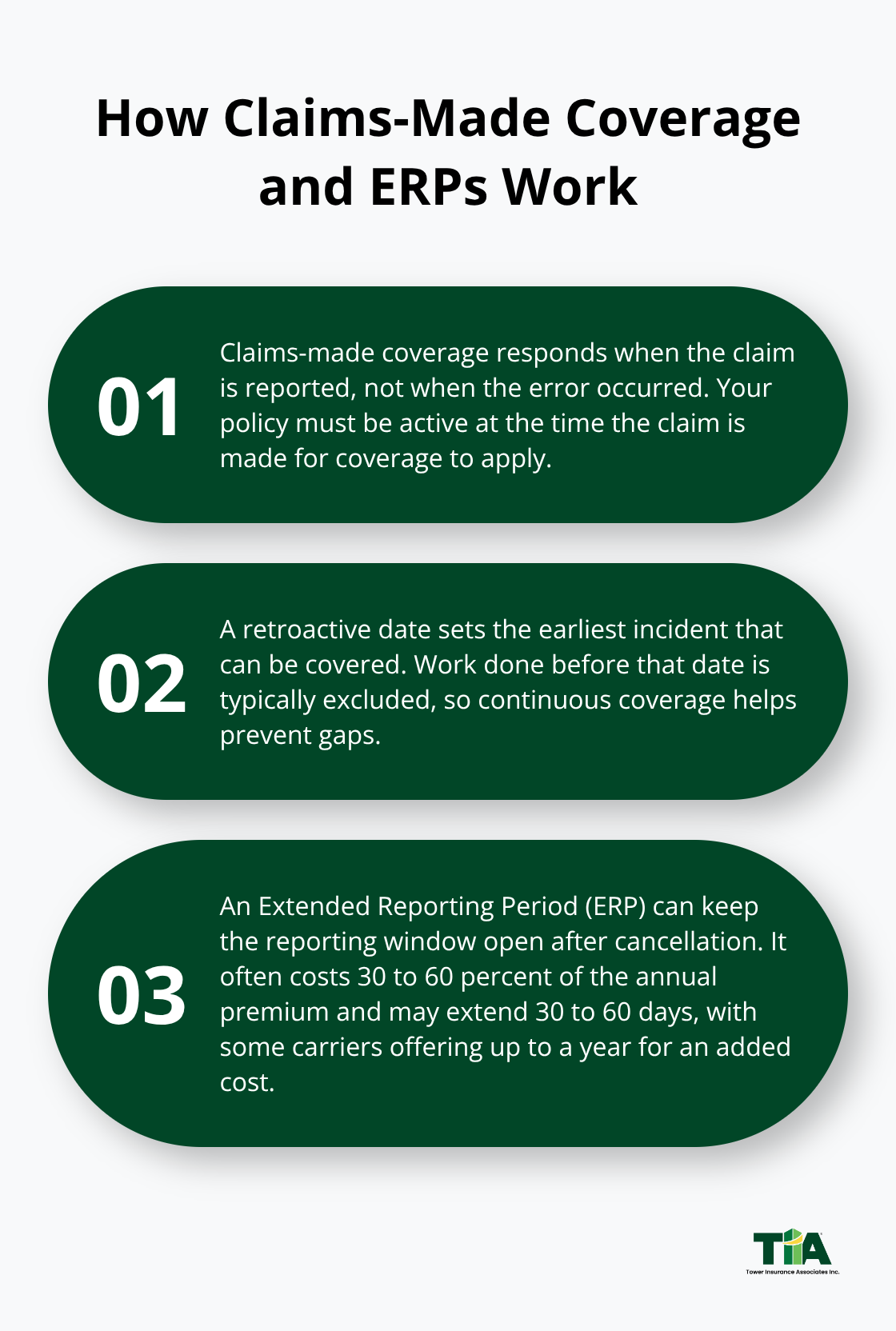

Claims-Made Policies Create Hidden Timing Traps

Most professional liability policies operate on a claims-made basis, not occurrence-based. The policy must remain active when the claim is reported, not when the error actually happened. Your policy includes a retroactive date that defines the earliest incident covered-any work performed before that date typically has no coverage. This creates a serious problem when you cancel a policy: claims arising from past work may never qualify for coverage unless you purchase extended reporting period (ERP) coverage, which typically costs 30 to 60 percent of your annual premium and extends the reporting window 30 to 60 days after cancellation.

Some carriers offer longer ERP periods up to a year for additional cost.

Long-Tail Risks Surface Years Later

The Humana Tower case involving Michael Graves & Associates demonstrates this risk-a design defect claim surfaced years after the project completed, highlighting how professional liability claims can emerge long after you finish the work. Maintaining continuous coverage protects you against this exposure. Discussing retroactive dates and ERP options with your agent prevents costly gaps when you change policies or retire. Understanding these timing mechanics now positions you to make informed decisions about coverage limits and policy structure, which directly affects how much protection you actually receive when a claim arrives.

Why Your Business Needs Professional Liability Coverage Now

The True Cost of Defending a Lawsuit

A single lawsuit costs more than you’ve made in profit over several years. Attorney fees run $150 to $300 per hour, expert witness costs exceed $5,000, and court filing fees accumulate throughout litigation. Even if you win the case, these defense costs still come out of your pocket without professional liability insurance. Small businesses spend an average of $13,300 annually on legal expenses, a figure that reflects routine matters before major litigation strikes. These numbers reflect what legal costs actually look like in 2026. Professional liability insurance covers these expenses immediately, preventing you from depleting cash reserves or taking on debt to defend yourself.

Industry-Specific Risks That Hit Your Bottom Line

Your industry determines how exposed you really are. Technology consultants face claims about failed implementations and missed deadlines that cost clients significant revenue. Accountants and bookkeepers deal with tax-related errors that trigger IRS penalties on top of client losses. Interior designers face claims when projects exceed budgets or don’t meet specifications. Healthcare professionals confront patient safety claims. Real estate agents handle transaction disputes. Each profession carries distinct risk profiles, which is why insurance costs vary significantly by industry. Your specific work-whether you advise clients, handle their money, design systems, or provide services that directly impact their operations-determines both your exposure and your insurance cost. If your clients depend on your expertise to make financial decisions or complete critical projects, you operate in a higher-risk category than you probably realize.

Client Contracts Now Demand Coverage

Clients increasingly demand proof of coverage before signing contracts. Many corporate clients require vendors to carry professional liability insurance and name them as additional insureds on the policy. Contracts for government work almost always mandate this coverage. Real estate transactions frequently require it. If you lose a contract because you lack coverage, you’ve already lost money. If you obtain coverage after signing a contract that demands it, you’ve failed to meet your obligation and face potential breach claims. Contracts specify minimum coverage limits, and underbidding those requirements leaves you personally liable for claims exceeding your policy limits. Starting coverage before you need it positions you to win contracts, meet client demands, and protect yourself against the specific exposures your industry creates-which means your next step involves understanding exactly how much coverage your business actually needs.

Sizing Coverage to Match What You Actually Risk

Choosing professional liability coverage without knowing your actual exposure is like buying auto insurance without considering how often you drive. Start by calculating what a worst-case claim would cost your business. If you’re an accountant and miss a tax deadline that triggers IRS penalties plus client losses, that claim could easily exceed $500,000. If you’re a web developer and a code error causes a client to lose a major contract, damages might reach $250,000 to $1,000,000 depending on the client’s revenue. If you’re an interior designer managing a commercial project, cost overruns and delays could create claims in the $100,000 to $500,000 range.

Match Your Limits to Real Industry Exposure

Professional liability coverage limits should reflect the realistic financial damage a single error could create in your specific industry, not a generic minimum. Technology consultants and management consultants typically need higher limits around $1,000,000 to $2,000,000 because implementation failures cost clients substantial revenue. Accountants and CPAs generally operate effectively with $250,000 to $500,000 limits unless they serve larger corporate clients. Healthcare professionals and mental health practitioners face different exposure profiles requiring careful limit selection based on patient populations served. Real estate agents, interior designers, and similar service providers often find $250,000 to $500,000 adequate unless they handle high-value transactions or projects.

Deductibles Control Your Premium Costs

After selecting your limit, evaluate deductible options carefully. Choosing a higher deductible like $10,000 or $25,000 instead of $2,500 can reduce your annual premium by 15 to 25 percent. This strategy works only if you can actually afford to pay the deductible from operating cash if a claim occurs. A lower deductible like $1,000 or $2,500 costs more in premiums but reduces financial strain when defending against a claim. The deductible applies per claim in most policies, so a $10,000 deductible on a $500,000 limit still leaves substantial coverage while meaningfully lowering your premium.

Pricing Reflects Your Risk Profile

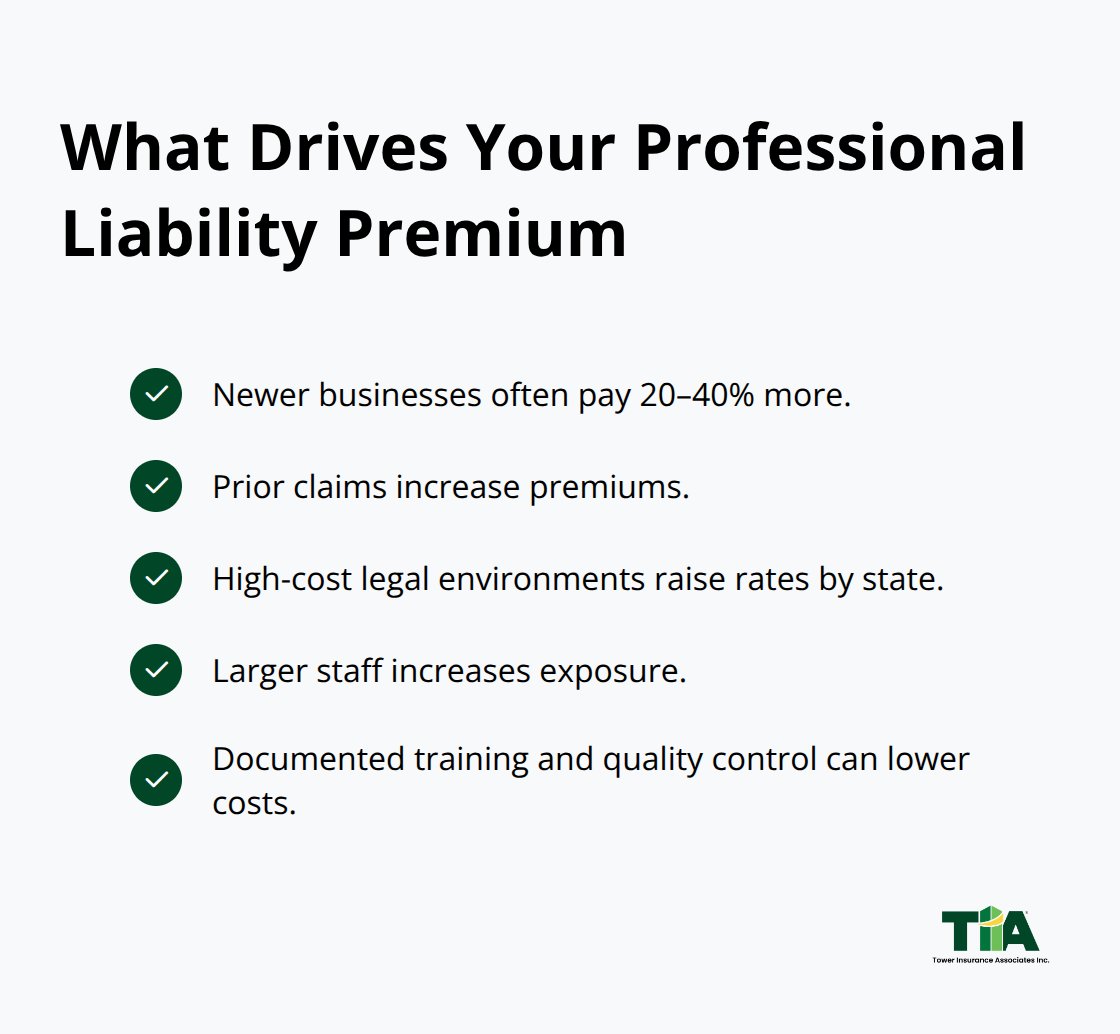

Cost varies significantly based on your specific situation, and comparing quotes from multiple carriers reveals which companies view your risk differently. A newer business typically pays 20 to 40 percent more than an established firm in the same industry because you lack a claims history demonstrating careful operations. A business with prior claims pays substantially higher premiums than one with a clean record, which means implementing documented training processes and quality control now directly reduces costs later.

Your location matters because states have different legal costs and claim frequencies. Your number of employees affects pricing because more people create more opportunities for errors.

Prepare Documentation for Accurate Quotes

Gathering specific documentation before requesting quotes helps carriers accurately assess your risk and provide competitive pricing. Collect your current contracts showing client requirements, your quality control and training documentation, your prior professional liability coverage details if you’ve carried it before, and information about any past claims or complaints. Most carriers issue quotes within 24 to 48 hours online, and coverage can start within days once you select a policy. Bundling professional liability with general liability insurance through a Business Owner’s Policy typically saves 10 to 20 percent compared to purchasing each separately, making comprehensive protection more affordable than coverage gaps that force you to pay for claims out of pocket.

Final Thoughts

Professional liability insurance isn’t optional for growing firms-it’s the foundation that lets you accept larger projects, win client contracts, and operate with confidence. Small business professional liability coverage protects your revenue, your reputation, and your ability to continue operations when claims arrive. The cost of staying uninsured far exceeds the monthly premium you’ll pay for solid protection.

Your next step is straightforward: gather your current contracts, document your quality control processes, and collect details about your prior coverage if you’ve carried it before. Contact Tower Insurance Associates, Inc. to discuss your specific industry risks and obtain competitive quotes from multiple carriers. We represent top-rated carriers and provide personalized service to find coverage that matches your actual exposure and budget.

Proper insurance planning compounds over time as a clean claims history reduces your premiums year after year, continuous coverage prevents retroactive date gaps that leave past work unprotected, and higher limits on growing projects protect you against underinsurance. The businesses that thrive invest in protection early and maintain it consistently as they scale. Your professional liability coverage becomes the safety net that lets you focus on growth instead of worrying about what happens when a client claim arrives.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.