Retail businesses face an unprecedented wave of cyber attacks that threaten both customer data and bottom-line profits. At Tower Insurance Associates, Inc., we’ve seen firsthand how a single breach can devastate a company’s finances and reputation.

Retail business cyber liability isn’t just an IT concern-it’s a business survival issue. This guide walks you through the real threats your store faces and how the right insurance protects you when the worst happens.

Why Retail Remains the Top Target for Cyber Criminals

The Scale of the Retail Attack Problem

Retail accounts for 24% of all cyberattacks according to Verizon data, making it the most hunted industry in the digital landscape. Criminals target retail because you hold what they want: customer payment data, personal information, and the financial means to pay ransoms. Online retail has intensified this problem dramatically, with a 75% rise in ransomware attacks in 2022 alone according to Sophos.

The shift toward e-commerce expanded your attack surface, and criminals have capitalized on this vulnerability.

The True Financial Cost of Breaches

The average retail data breach cost $3.28 million in 2022 according to Verizon’s Data Breach Investigations Report. Target’s 2013 breach impacted 41 million payment cards and 70 million customers, ultimately costing the company around $290 million. Home Depot’s 2014 breach affected 52 million customers with pre-tax expenses near $195 million. These weren’t small businesses-they were industry giants with sophisticated security teams, yet the costs consumed massive portions of their annual budgets. For smaller retailers, a $3.28 million breach can mean bankruptcy.

Verizon found that 98% of retail breaches were financially motivated, with attackers targeting payment and personal data in nearly half of incidents. Credentials were stolen in almost 50% of cases, giving criminals ongoing access to your systems long after the initial breach.

Customer Trust Evaporates After a Breach

Your reputation takes an equal hit to your finances. A Vercara study found that 75% of consumers would abandon a brand following a data breach, meaning customer lifetime value evaporates overnight. This reputational damage extends far beyond the immediate incident-customers remember breaches for years.

The erosion of trust becomes permanent unless you demonstrate robust recovery and prevention measures.

How Attackers Actually Get Inside

Most retail breaches happen through credential theft and phishing. Verizon data shows credential phishing leads attack methods at 30.43% for retail-targeted incidents. Your employees are the frontline, and a single compromised password or successful phishing email opens your entire network to attackers. This human element makes cyber threats nearly impossible to prevent through technology alone, which is why insurance becomes non-negotiable rather than optional.

The vulnerabilities that make retail such an attractive target extend beyond external attacks-they run through your operations, your staff, and your supply chain relationships.

Key Vulnerabilities in Retail Operations

Point-of-Sale Systems Remain Dangerously Exposed

Your point-of-sale systems sit at the frontline of customer data collection, yet they remain dangerously exposed in most retail environments. PCI DSS compliance requires firewalls, encryption, and antivirus software, but many retailers treat these as checkbox exercises rather than foundational security. The reality is brutal: your POS terminals collect credit card data dozens of times per day, and if that system isn’t isolated from your general network, a single compromised employee laptop can give attackers direct access to payment information.

Isolation matters more than most retailers realize. Your payment processing systems should sit on a completely separate network segment with its own firewall rules, antivirus protection, and monitoring. Don’t use the same computer for payment processing that employees use for general web browsing or email. That separation costs almost nothing to implement but prevents the majority of payment data theft. Additionally, ensure your POS vendor provides regular security patches and that you apply them immediately upon release. Delayed patching is how attackers exploit known vulnerabilities in thousands of retail locations simultaneously.

Employee Access and Human Error Create Your Weakest Link

Employee access and human error remain your weakest link, and no firewall fixes bad password practices. Verizon’s research shows credential phishing leads retail attacks at 30.43%, meaning your staff’s login credentials are the most valuable asset criminals target. Enforce multi-factor authentication across all systems that touch customer data, especially for remote access. A password alone is insufficient in 2026.

Limit data access to only the employees who genuinely need it for their job-a cashier shouldn’t access your customer database, and a stock person shouldn’t access payment systems. This least-privilege approach reduces damage when an account gets compromised. Train your team quarterly on recognizing phishing emails and credential theft tactics, and make it clear that clicking suspicious links or sharing passwords has real consequences for the entire business.

Third-Party Vendors Present Hidden Vulnerabilities

Third-party vendors and supply chain partners present an equally serious vulnerability that most retailers ignore until after a breach. Before engaging any IT service provider, payment processor, or inventory management vendor, demand proof of their cyber liability insurance and ask about their specific security controls. Don’t assume your vendor is secure just because they’re established. JD Sports suffered a 2023 breach affecting 10 million customers through vendor access, demonstrating that your security is only as strong as your weakest partner.

Put specific security requirements and breach notification obligations in your vendor contracts. Require vendors to notify you of any incidents within 24 hours, not weeks later. Regularly audit vendor access to your systems and revoke credentials for vendors you no longer use. These vulnerabilities across your POS systems, staff, and vendor relationships create multiple entry points for attackers-which is precisely why cyber liability insurance becomes your essential safety net when prevention fails.

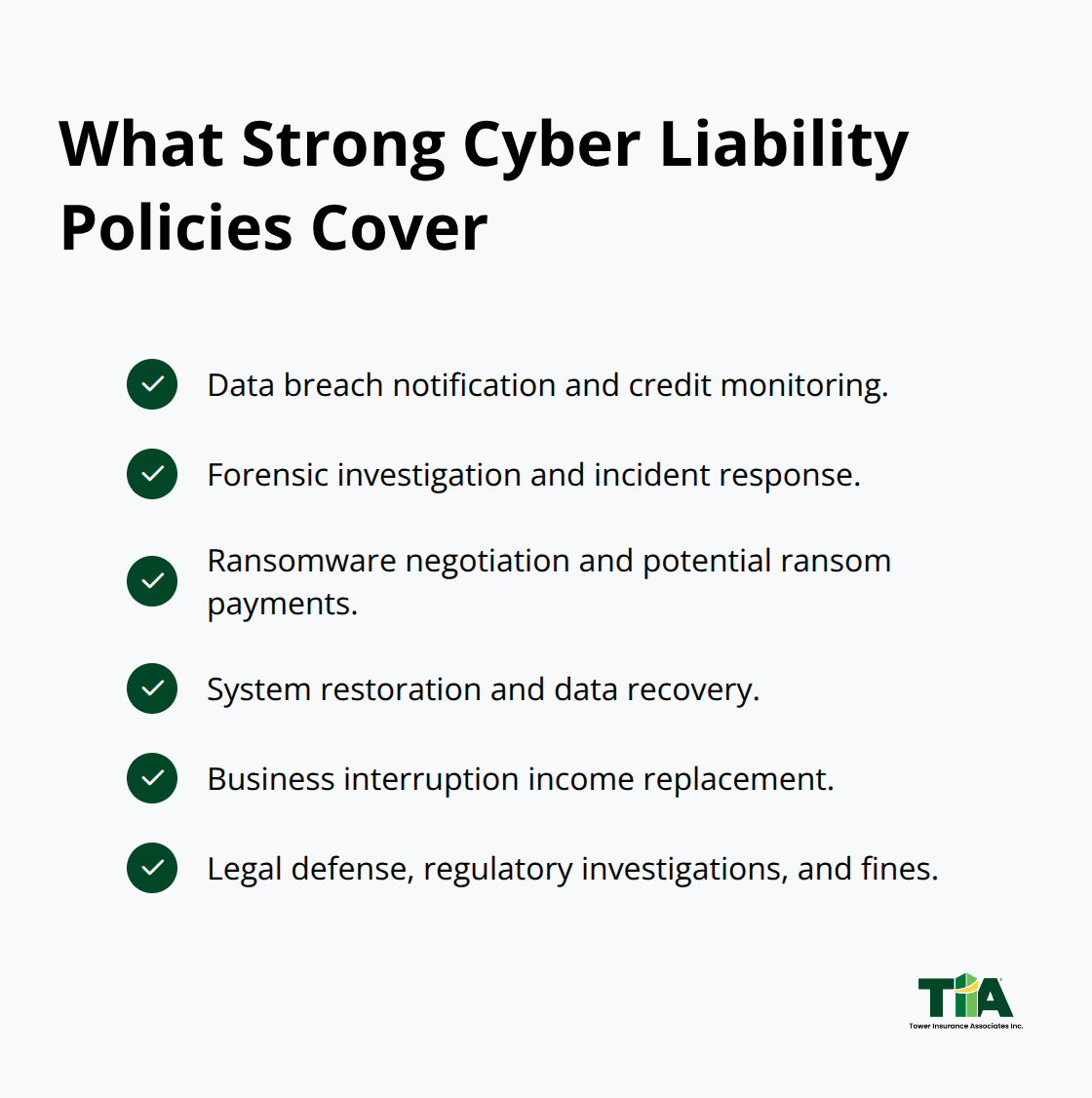

What Cyber Liability Insurance Actually Covers

Cyber liability insurance stops being theoretical the moment your systems get hit. This coverage addresses the specific costs that follow a breach, not the breach itself. When attackers steal customer data or lock your systems with ransomware, cyber liability pays for the immediate response and the long tail of expenses that cripple unprepared retailers.

The average retail breach costs $4.88 million, but most retailers have no idea where that money actually goes.

Data Breach Response and Notification Costs

Your policy covers notification costs when you must contact affected customers, credit monitoring services you’re legally required to provide, and forensic investigation to determine what happened. This isn’t optional spending-it’s mandatory under state breach notification laws and federal regulations like GLBA and FCRA. A retailer in California must notify customers within specific timeframes, and that notification process alone costs tens of thousands of dollars when you’re handling millions of records. Credit monitoring services that you must offer for typically two to three years add another significant expense. Without insurance, these costs come directly from your operating budget and can bankrupt smaller operations.

Ransomware and Extortion Coverage

Ransomware attacks represent 13.04% of retail-targeted attacks according to Verizon data and lock your entire operation-no point-of-sale, no inventory access, no customer transactions. Your cyber policy includes access to negotiation services with threat actors and can cover ransom payments if you decide that route. More importantly, it covers the restoration costs to rebuild your systems, recover your data, and get back online.

Business Interruption Protection

Business interruption coverage reimburses lost revenue while you’re offline, which matters enormously for retailers operating on thin margins. A mid-sized retailer losing $50,000 daily in sales during a week-long shutdown faces $350,000 in direct losses before recovery costs. Your cyber policy absorbs these losses so you survive the incident without depleting cash reserves or taking on emergency debt.

Legal Defense and Regulatory Fines

Legal and regulatory costs extend beyond customer lawsuits to include regulatory investigations and potential fines from state attorneys general, the FTC, or payment card networks. Target and Home Depot both faced multimillion-dollar settlements with regulators years after their initial breaches, demonstrating that regulatory consequences extend far beyond the incident itself. Cyber liability insurance covers these defense costs and settlement amounts, protecting your company from catastrophic financial exposure that would otherwise consume years of profits.

Final Thoughts

Retail business cyber liability isn’t a future problem-it’s happening right now to retailers of every size. The data proves it: breaches cost millions, destroy customer trust, and create regulatory nightmares that extend years beyond the initial incident. Prevention matters, but it remains incomplete without financial protection when attackers succeed.

The retailers winning this battle combine two strategies. First, they implement security fundamentals: isolating payment systems, enforcing multi-factor authentication, training employees on phishing, and vetting vendor security before engagement. These measures reduce breach risk significantly, yet they cannot eliminate it entirely. Second, they pair these controls with cyber liability insurance that covers the costs prevention cannot eliminate-forensic investigation, customer notification, credit monitoring, ransomware negotiation, business interruption losses, and regulatory defense (expenses that would otherwise bankrupt most retailers).

At Tower Insurance Associates, Inc., we understand retail operations and the specific cyber risks you face. Contact Tower Insurance Associates, Inc. to discuss retail business cyber liability options that fit your budget and protect your profits.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.