One mistake we see professionals make is underestimating their liability exposure. A California professional liability policy protects your practice when clients claim you caused them financial harm through negligence or errors.

At Tower Insurance Associates, Inc., we help professionals understand exactly what this coverage includes and how to choose the right limits for their business. This guide walks you through the details so you can make an informed decision.

What Professional Liability Insurance Actually Covers

Professional liability insurance in California protects you from financial devastation when a client sues over your work. This isn’t theoretical protection-it covers real claims where clients allege you made mistakes, gave bad advice, or failed to deliver what you promised. The policy pays for your legal defense costs and any settlement or judgment the court orders you to pay, up to your coverage limits.

A designer who didn’t follow the agreed blueprint, an accountant who missed tax deductions, or a consultant who gave incorrect guidance all face exposure that professional liability insurance handles. Defense costs alone can drain $50,000 to $200,000 before a case even goes to trial, which is why this protection matters regardless of your experience level.

Who Actually Needs This Coverage

California law requires professional liability insurance for lawyers who are shareholders in professional law corporations, partners in LLPs, or Registered Foreign Legal Consultants under California Corporate Code Section 16956. Solo law practitioners aren’t legally required to carry it, but over 90% of California attorneys in private practice maintain coverage anyway-and for good reason.

About 5 to 6 insured lawyers per 100 in private practice experience a malpractice claim in any given year. Outside law, many professions face client demands for proof of coverage before accepting work. Real estate professionals, architects, engineers, and consultants routinely encounter clients or contracts that require specific coverage limits. The most claim-prone practice areas are trusts and estates, business transactions, and corporate or securities work, though conflicts of interest remain the number-one driver of malpractice claims across all fields.

How Claims-Made Policies Work

Professional liability in California typically operates on a claims-made basis rather than an occurrence basis. A claims-made policy covers claims that you report during the policy period, regardless of when the work happened. This means you need continuous coverage-if your policy lapses and a client sues six months later, the gap leaves you unprotected.

Many professionals miss this detail and discover it’s too late when a claim arrives. When you switch carriers, you must ensure the new policy includes prior acts coverage so events that occurred before the switch remain covered. This protection prevents gaps that could expose you to uninsured liability.

What You’ll Pay for Coverage

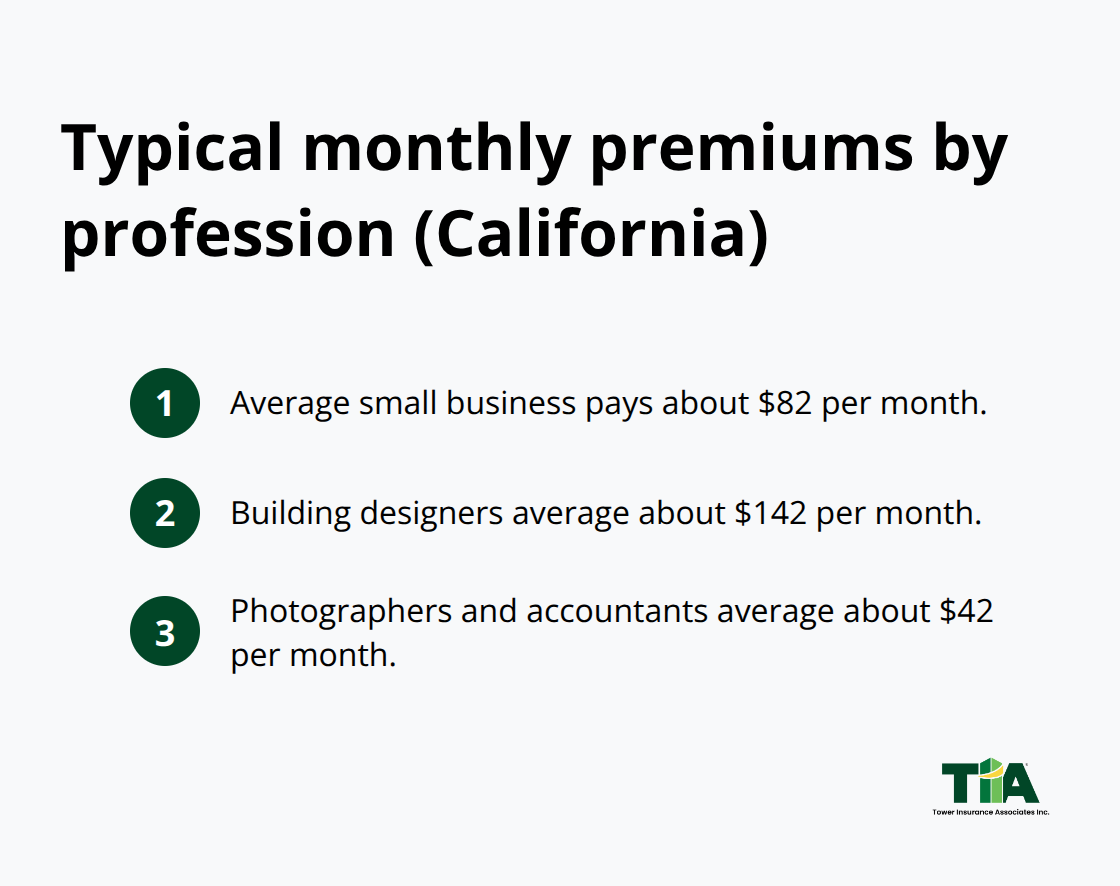

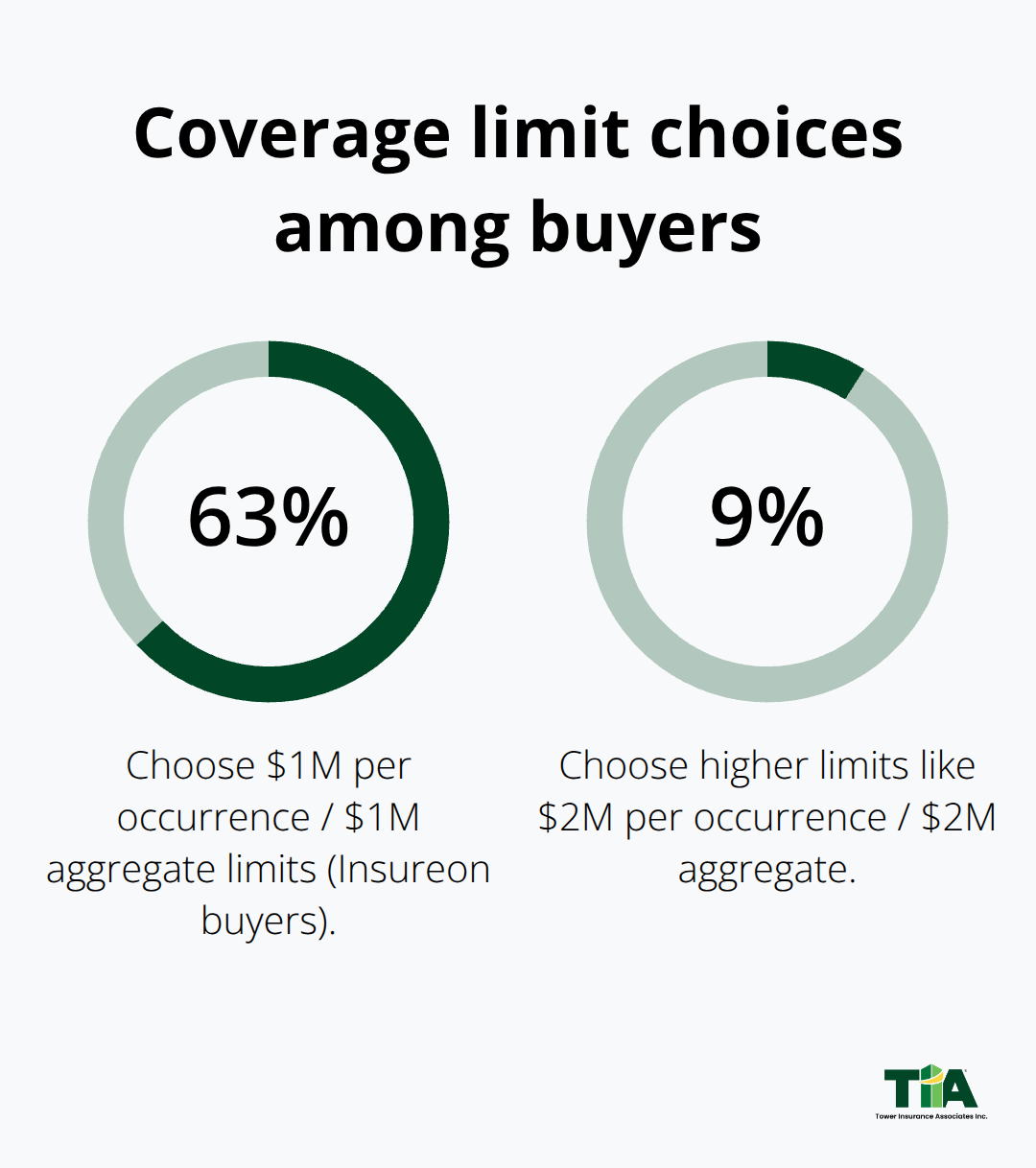

The average small business in California pays about $82 per month for professional liability insurance, according to Insureon’s data from approximately 40,000 small-business policyholders. Most customers select $1 million per occurrence and $1 million aggregate limits, which covers 63% of Insureon buyers.

Industry risk heavily influences cost-building designers average about $142 per month, while photographers and accountants average about $42 per month. Your claims history, location, revenue, number of employees, and the specific services you offer all shape your premium.

A clean claims history typically yields lower rates, so loss prevention practices directly reduce your costs over time. Understanding these cost drivers helps you identify where you can control expenses while maintaining adequate protection for your practice.

What Your Professional Liability Policy Actually Pays For

How Claims-Made Coverage Works in California

Claims-made coverage dominates California’s professional liability market, and this structure directly affects what happens when a client sues. Your policy covers claims that you report during the active policy period, not when the work occurred. A designer who completes a project in 2024 but receives a lawsuit notice in 2026 needs active coverage in 2026 to trigger protection. This distinction matters enormously because it creates a coverage gap if you let your policy lapse. Stop paying premiums, and a client sues months later-you’re uninsured. Errors & Omissions Insurance will pay for any resulting judgments against you, including court costs, up to the coverage limits on your policy.

When you switch carriers, insist that your new policy includes prior acts coverage, which extends protection backward to cover work performed before the policy started. Without this endorsement, you face exposure for years of prior work. Some carriers charge extra for prior acts coverage, but the cost is minimal compared to the uninsured risk you’d carry otherwise.

Defense Costs and Settlement Coverage

Defense costs and settlement payouts are where professional liability actually protects your finances. Your insurer pays legal fees, expert witness expenses, and court costs as your case progresses, separate from your coverage limits. Most professionals cannot absorb defense costs without the policy. The insurer also covers any judgment or settlement up to your chosen limit.

Understanding Policy Exclusions

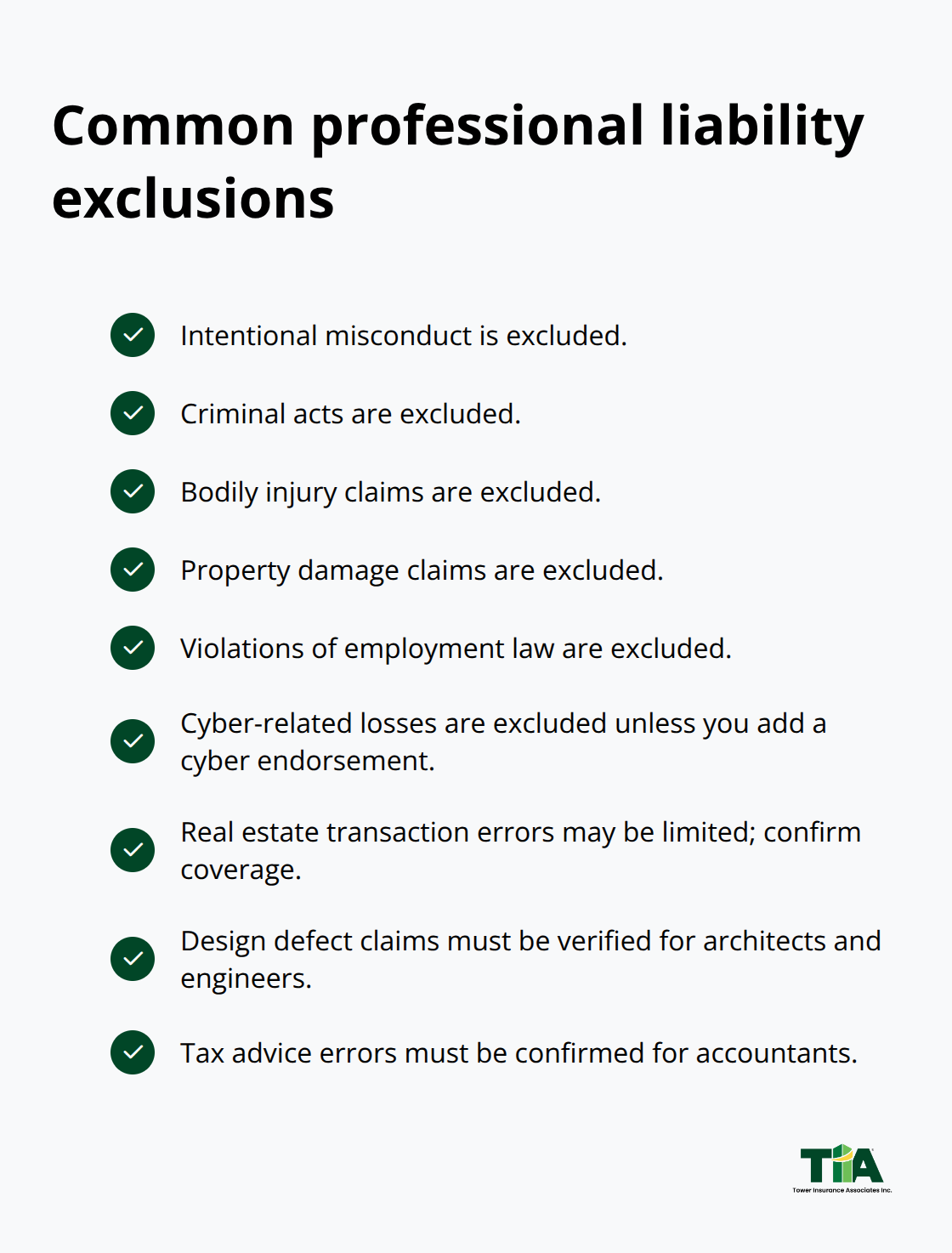

Exclusions exist that you must understand before you buy. Professional liability policies typically exclude intentional misconduct, criminal acts, bodily injury claims, property damage, and violations of employment law. Some policies exclude cyber-related losses unless you add a cyber endorsement.

Real estate professionals should confirm their policy covers errors and omissions in property transactions, as some carriers limit coverage in this area. Architects and engineers need to verify that design defect claims are covered, not excluded. Accountants must confirm that tax advice errors are included in their coverage.

These exclusions vary by carrier and policy form, so comparing actual policy language matters more than comparing price alone. Your specific practice area requires a policy that covers your actual exposures rather than leaving gaps. As an independent insurance agency representing multiple top-rated carriers, Tower Insurance Associates, Inc. matches your practice area with appropriate coverage that addresses your real risks.

What Gaps in Coverage Cost You

The cost of inadequate coverage extends far beyond the premium you save. A policy with the wrong exclusions leaves you personally liable for claims that fall outside your coverage. You pay defense costs from your own pocket, and any judgment comes directly from your business assets or personal finances. This exposure is why comparing policies side-by-side-not just prices-determines whether you’re truly protected.

Your next step involves assessing your industry’s specific risks and determining the coverage limits that actually match your exposure level.

Matching Coverage to Your Real Practice

How Your Industry Shapes Cost and Coverage Needs

Your industry determines what professional liability actually costs and which exclusions matter most. Building designers pay roughly $142 monthly according to Insureon data from 40,000 small-business policyholders, while photographers and accountants average $42 monthly. This gap reflects real risk differences. Architects need coverage that explicitly includes design defect claims. Real estate professionals require transaction error protection. Accountants must confirm tax advice errors are covered. Technology consultants benefit from cyber liability add-ons because data breach lawsuits increasingly target professional services. The wrong policy for your field leaves dangerous gaps.

When you shop for quotes, start by identifying which practice area your carrier places you in, then verify the policy covers your actual work. A consultant who gives cybersecurity advice but purchases a general professional liability policy without cyber coverage discovers too late that the exclusion applies when a data breach claim arrives.

How Your Claims History Affects Your Premiums

Your claims history shapes premiums significantly. Insureon’s data shows that professionals with clean claim records pay substantially less than those with prior incidents. This means loss prevention directly reduces your costs over time. You should document client agreements thoroughly, maintain communication records, and follow industry standards religiously because these practices both lower claims frequency and demonstrate to insurers that you manage risk responsibly.

Selecting the Right Coverage Limits

Coverage limits must match your actual exposure, not your budget constraints. Standard coverage requirements are $1 million per occurrence and $3 million aggregate. Roughly 9% of Insureon customers choose higher limits like $2 million per occurrence and $2 million aggregate, which increases premiums but provides stronger protection. Your decision depends on contract requirements, client sophistication, and project complexity.

Real estate transactions often require proof of coverage at specific limits before clients will work with you. Corporate and securities work typically demands higher limits than general consulting. You should review your largest contracts to see what coverage limits clients require, then select limits that exceed those requirements. The average deductible sits around $2,500, and raising your deductible reduces monthly premiums noticeably. A solo practitioner with five years in business, clean claims history, and $1 million limits might pay $600 to $1,200 annually depending on industry and location.

Finding Competitive Rates and Avoiding Coverage Gaps

Shopping the market yourself takes time, but working with an independent agent accelerates the process. Tower Insurance Associates, Inc., an independent insurance agency representing multiple top-rated carriers, obtains quotes from different insurers to find competitive rates specific to your practice area and risk profile. When you switch carriers, confirm that prior acts coverage extends back to protect your entire practice history, and avoid policy lapses that create uninsured periods. Continuous coverage matters because claims-made policies only protect you when you’re actively insured during the year the claim is reported.

Final Thoughts

Professional liability insurance protects your practice from financial devastation when clients claim you made mistakes or failed to deliver promised results. A California professional liability policy covers your legal defense costs and settlements up to your chosen limits, which means the difference between staying in business and losing everything when a claim arrives. About 5 to 6 insured lawyers per 100 in private practice experience a malpractice claim annually, and claim severity has spiked due to court delays and case complexity.

Protecting your professional practice starts with honest assessment of your real exposure. Review your largest client contracts to identify required coverage limits, then select limits that exceed those requirements. Confirm your policy includes prior acts coverage when you switch carriers to avoid gaps in protection, and document client agreements thoroughly because these practices reduce claims frequency and demonstrate responsible risk management to insurers.

The most critical step is avoiding policy lapses, since claims-made coverage only protects you when you’re actively insured during the year a claim is reported. We at Tower Insurance Associates, Inc. represent multiple top-rated carriers and obtain quotes tailored to your specific practice area and risk profile. Contact Tower Insurance Associates to discuss your professional liability needs and get personalized guidance for your practice.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.