Cyber attacks on California businesses are accelerating, with ransomware incidents up 37% year-over-year according to the FBI’s 2024 Internet Crime Report. A single breach can cost your company hundreds of thousands in recovery, legal fees, and lost revenue.

Commercial cyber insurance in California isn’t optional anymore-it’s a business necessity. We at Tower Insurance Associates, Inc. help California business owners understand their coverage options and build protection strategies that actually work.

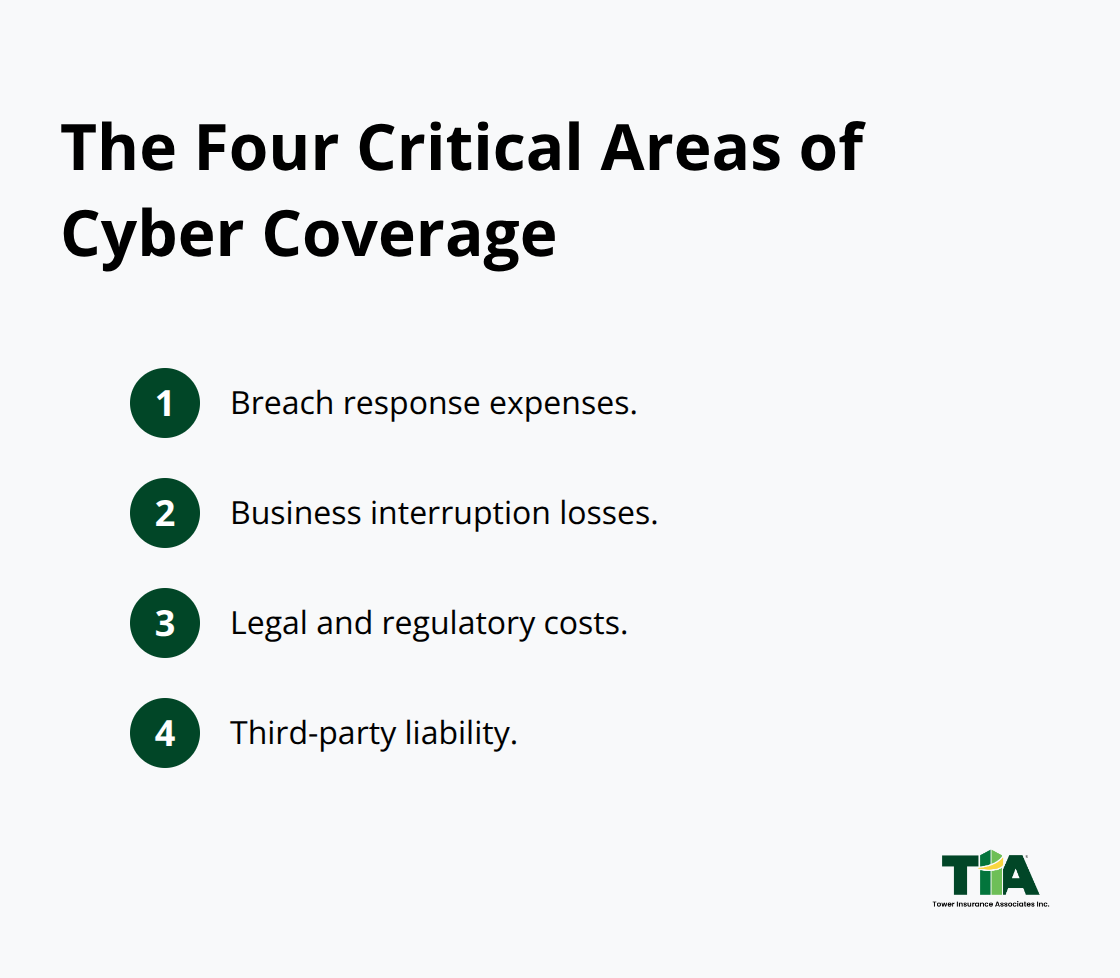

What Commercial Cyber Insurance Actually Covers

Commercial cyber insurance protects your California business from the financial fallout of data breaches, ransomware attacks, and other digital threats. The coverage spans four critical areas: breach response expenses, business interruption losses, legal and regulatory costs, and third-party liability. First-party coverage includes costs to respond to a breach, notify affected customers, recover stolen data, and restore your systems.

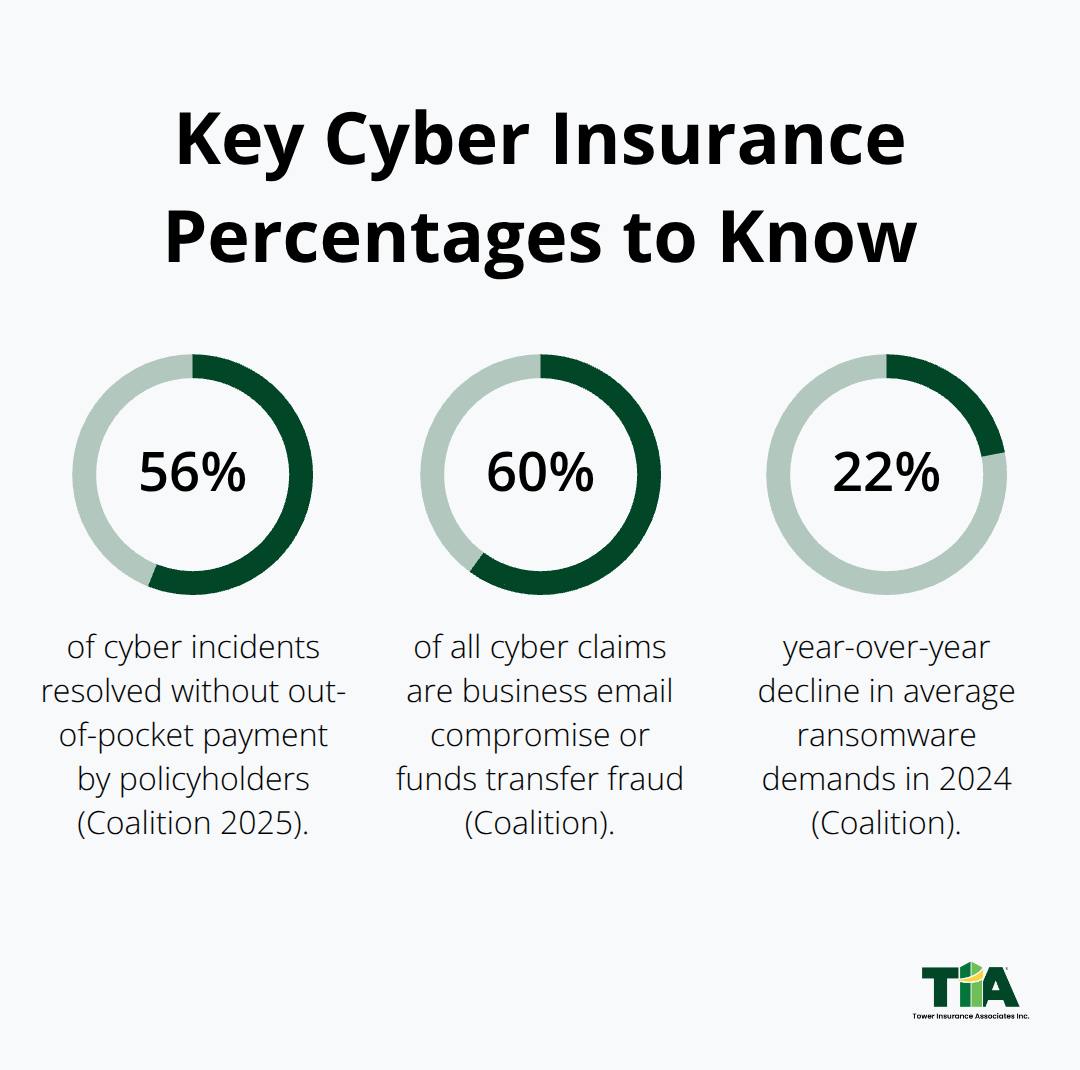

Third-party coverage handles liability claims when customer data is compromised in your care, plus legal defense costs if you face lawsuits. According to Coalition’s 2025 Cyber Claims Report, 56% of cyber incidents were resolved without any out-of-pocket payment by policyholders, meaning the right policy catches what you’d otherwise pay from operating cash.

Coverage That Stops the Bleeding

Business interruption coverage reimburses lost income while your systems remain down-critical for companies that cannot operate without their networks. Most policies also cover ransomware demands and incident response services, which matter because ransomware remains the costliest attack type. In 2024, the average ransomware demand was $1.1 million, though Coalition’s incident response team negotiated payments down by an average of 60%, showing why professional negotiators in your corner save real money.

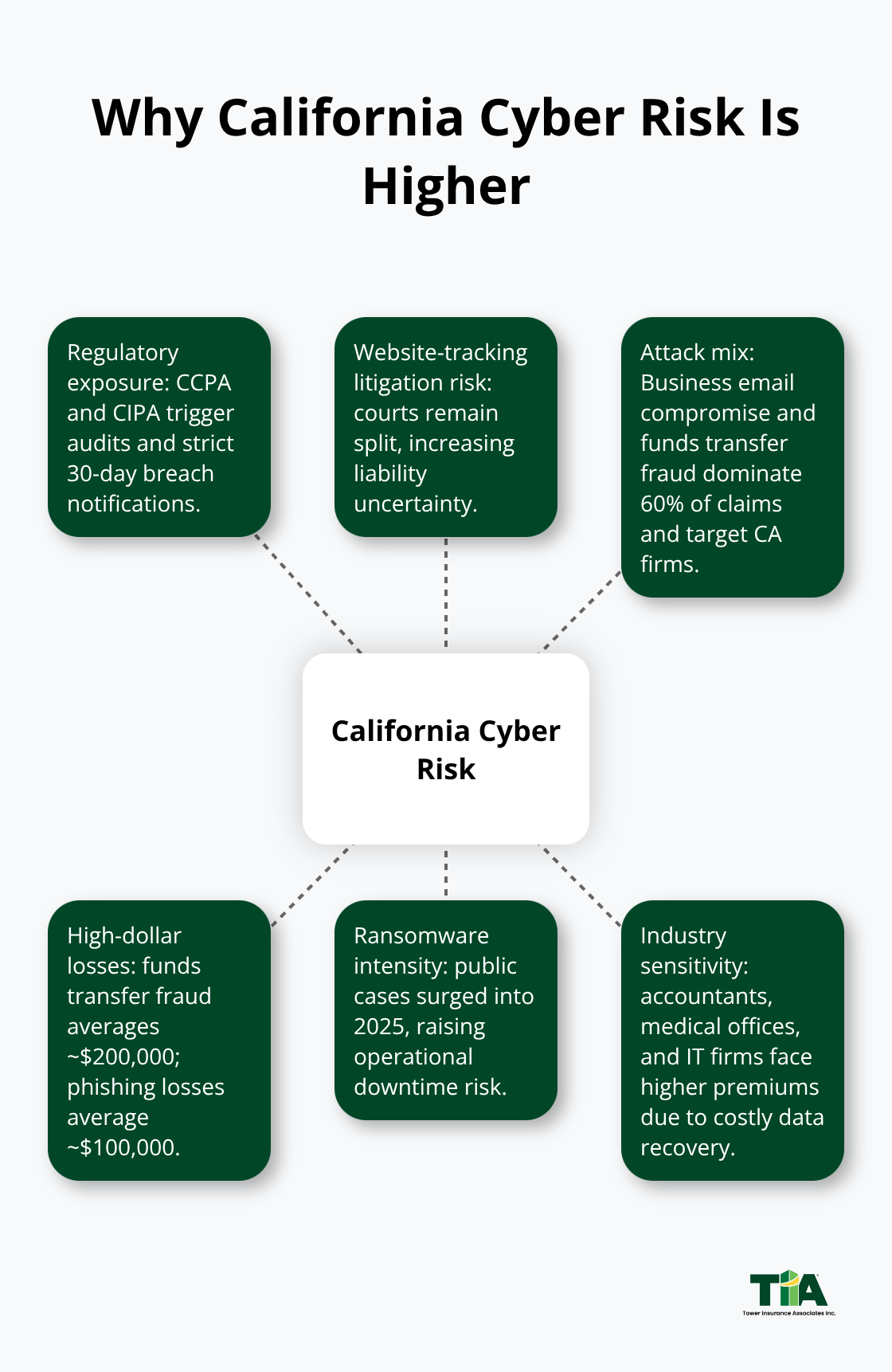

Why California Businesses Face Escalating Cyber Risk

California businesses operate in a uniquely risky environment. The state’s CCPA and CIPA privacy laws create regulatory exposure that other states do not have-breaches here trigger mandatory cybersecurity audits and 30-day breach notification requirements. Website-tracking litigation under CIPA remains high, with courts still split on liability, meaning your digital footprint carries genuine legal risk.

Business email compromise and funds transfer fraud account for 60% of all cyber claims according to Coalition, and these schemes specifically target California companies because of their size and data value. In 2024, funds transfer fraud losses averaged about $200,000 per incident, and phishing losses averaged around $100,000. Ransomware incidents have intensified into 2025, with March 2025 marking the highest volume of public ransomware cases on record. Your industry matters too-accountants, medical offices, and IT firms face higher premiums because their data recovery costs run substantially higher when breaches occur.

The Real Cost of Inaction

A data breach costs far more than most business owners expect. Average remediation expenses exceed $300,000, and when you add notification costs, legal defense, regulatory fines, and lost customer trust, a single incident can force a small business to shut down. Coalition helped claw back $31 million for policyholders in 2024, with an average recovery of $278,000 per incident, but only if policyholders had coverage in place and reported funds transfer fraud within 72 hours. Without cyber insurance, you absorb these costs yourself. With it, your carrier handles negotiation, recovery, and incident response while you focus on keeping your business operational.

The question now shifts from whether you need cyber insurance to which policy actually fits your specific business profile and risk exposure.

Key Coverage Areas in Commercial Cyber Insurance Policies

Data Breach Response Costs That Hit Immediately

When a breach strikes, financial damage spreads across multiple fronts at once. Data breach response coverage handles the immediate costs that most business owners drastically underestimate. You’ll need funds for forensic investigation to determine what attackers stole, notification services to contact affected customers within California’s mandatory 30-day window, credit monitoring setup for victims, and public relations support to manage reputation damage. Without this coverage in place, you write checks from operating cash while your team scrambles to contain the breach.

Business Interruption Coverage Protects Your Revenue Stream

Business interruption coverage addresses the silent killer most California businesses overlook: lost revenue while systems stay down. If your network goes offline for two weeks due to ransomware, you still owe payroll, rent, and vendor payments even though you generate zero income. This coverage reimburses that lost profit, plus ongoing operating expenses, keeping your business afloat during recovery. The financial impact compounds quickly-a week of downtime can cost a mid-sized firm tens of thousands in lost sales alone, making this protection essential for companies that depend on continuous network access.

Liability Protection Under California’s Strict Privacy Laws

Liability protection becomes essential because California’s CCPA and CIPA regulations hold you accountable when customer data is compromised in your systems. If a breach exposes customer information, you face lawsuits from those customers plus regulatory penalties from the California Attorney General. Your policy covers legal defense costs, settlements, and judgments up to your policy limits. Medical offices, accountants, and IT firms experience the highest liability exposure because their data recovery costs run $300,000 or more when breaches occur.

Ransomware Negotiation Support Reduces What You Actually Pay

The 2024 average ransomware demand of $1.1 million illustrates why negotiation support matters. Professional negotiators in your corner directly reduce what you’ll actually pay if attackers strike. This negotiation capability transforms your policy from a passive reimbursement tool into an active defense mechanism that protects both your cash flow and your operational timeline. The difference between paying full ransom demands and negotiated amounts represents the kind of real savings that separates adequate coverage from truly protective coverage.

Why Coverage Limits and Deductibles Shape Your Real Protection

The coverage limits you select determine your maximum protection, while your deductible determines how much you absorb before insurance kicks in. A $3 million policy costs substantially more than a $25,000 policy, so aligning your limits to your actual data exposure and recovery costs matters. Higher deductibles lower your premiums but increase your out-of-pocket risk when incidents occur. Your industry, data volume, and prior claim history all influence both the cost and the availability of coverage you can obtain. Understanding these trade-offs helps you build a policy that actually matches your business profile rather than one that leaves gaps when you need protection most.

Finding the Right Policy for Your California Business

Match Your Coverage to Your Industry’s Data Exposure

Your industry determines your cyber risk profile more than almost any other factor. Accountants, medical offices, and IT service providers face substantially higher premiums because their data recovery costs exceed $300,000 when breaches occur. A law firm storing client files faces different exposure than a retail business with minimal customer data on hand. Start by cataloging exactly what sensitive information your business stores, processes, and transmits. If you handle payment card data, medical records, or financial documents, your cyber insurance costs will reflect that exposure. If you store mostly general business communications and basic customer contact information, your premiums drop considerably. The gap between these two scenarios can be $1,000 to $3,000 annually, making this assessment genuinely worth your time.

Strengthen Your Security Posture to Lower Premiums

Next, examine your current security posture. Do you require employees to use strong passwords and multi-factor authentication? Is your antivirus software current across all devices? How often do you back up critical systems? Insurers directly reduce premiums for businesses that demonstrate concrete security measures because these practices lower claim frequency. A company with firewalls, regular security updates, and documented access controls pays less than one with minimal protections-sometimes 15 to 25 percent less according to carrier underwriting standards. These investments in security infrastructure translate directly into lower insurance costs while simultaneously reducing your actual breach risk.

Select Policy Limits That Match Your Financial Reality

Policy limits and deductibles require honest conversation about your financial capacity to absorb loss. A $3 million policy with a $10,000 deductible costs substantially more than a $500,000 policy with a $25,000 deductible, but the lower-limit option leaves you exposed if a major incident occurs. Your decision should match your revenue and cash reserves. A company with $2 million in annual revenue cannot responsibly choose a $500,000 limit because a single breach could exceed that protection entirely. Conversely, a startup with minimal data exposure choosing a $5 million limit wastes premium dollars on unnecessary coverage.

Average ransomware demands in 2024 reached $1.1 million, declining 22 percent year-over-year. This trend matters because it suggests your limits need to cover both ransom potential and incident response costs, typically totaling $250,000 to $500,000 for most mid-sized California businesses.

Balance Your Deductible Against Your Cash Reserves

Higher deductibles reduce your premium but increase your out-of-pocket exposure when claims happen. A $50,000 deductible versus a $10,000 deductible might save you $800 annually, but it shifts significant risk onto your business if an incident strikes. Try setting a deductible that matches 30 days of operating cash reserves so you can absorb the out-of-pocket portion without operational strain. This approach aligns your insurance structure with your actual financial capacity and prevents premium savings from creating dangerous coverage gaps.

Final Thoughts

Commercial cyber insurance in California protects your business from threats that accelerate every year. Ransomware demands averaged $1.1 million in 2024, business email compromise accounts for 60% of all cyber claims, and funds transfer fraud losses hit $200,000 per incident on average. Without coverage, a single breach forces you to absorb these costs from operating cash while managing recovery, legal defense, and regulatory compliance simultaneously.

Protecting your California business starts with honest assessment of your data exposure and security posture. Catalog what sensitive information you store and process, then strengthen your defenses through multi-factor authentication, current antivirus software, regular backups, and documented access controls. These investments lower your breach risk while simultaneously reducing your insurance premiums by 15 to 25 percent, and selecting policy limits and deductibles that match your financial reality rather than your worst-case fears ensures you obtain adequate protection without overpaying.

We at Tower Insurance Associates, Inc. understand California’s unique regulatory environment and help you build commercial cyber insurance policies that actually protect your business. CCPA and CIPA requirements, mandatory breach notification timelines, and website-tracking litigation create compliance obligations that generic national policies often miss. Contact us to assess your specific risk profile and compare coverage options across top-rated carriers.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.