California businesses face a rising tide of cyberattacks, with the state’s strict data privacy laws making compliance failures costly. A single breach can drain your finances and damage your reputation in ways that traditional insurance won’t cover.

That’s where California cyber liability insurance comes in. We at Tower Insurance Associates, Inc. help businesses like yours understand what protection you actually need and how to get it.

Why Cyber Threats Cost California Businesses Real Money Right Now

California Leads the Nation in Cybercrime Complaints

California ranked number one among all U.S. states for cybercrime complaints in 2024, according to the FBI’s Internet Crime Complaint Center. The state’s businesses filed thousands of complaints involving cryptocurrency fraud, extortion, and phishing attacks. These aren’t theoretical risks-they’re happening to your competitors and peers today.

State Privacy Laws Multiply Your Financial Exposure

What makes California different is that cyberattacks here trigger expensive compliance obligations that don’t exist in other states. Under the California Consumer Privacy Act and California Privacy Rights Act, a data breach involving customer information can result in regulatory fines up to $7,500 per violation. A mid-sized breach affecting hundreds of customers can quickly balloon into hundreds of thousands of dollars in penalties alone, before you address notification costs, credit monitoring, or legal defense.

California’s 2026 amendments now require defined threshold businesses to conduct annual cybersecurity audits performed by qualified independent professionals. These audits must document security gaps, weaknesses, remediation steps, and timelines-creating a paper trail that regulators and plaintiffs’ attorneys will scrutinize if a breach occurs. This mandatory audit requirement means your cyber risk profile is now permanently documented and subject to regulatory review, making breach response costs even more substantial.

Direct Financial Losses Extend Beyond Regulatory Penalties

Data breach notification costs-including mailings, call centers, and credit monitoring services-represent a major claim component, especially in a state as large as California. Business interruption from a ransomware attack or system downtime can halt operations for days or weeks, eliminating revenue while your IT team works on recovery. A spear-phishing attack that tricks an employee into authorizing a wire transfer can result in direct financial loss that traditional business insurance won’t cover.

Third-party liability claims follow when your breach exposes customer data or when a compromised vendor in your supply chain causes downstream damage. The Federal Trade Commission estimates the average time to resolve an identity theft incident is about 400 hours of management attention-time your leadership should spend running the business, not managing a crisis.

Standard Insurance Leaves You Exposed

California’s strict privacy environment means your cyber liability policy must explicitly cover regulatory fines under CCPA and CPRA, breach notification expenses, forensic investigations, and business interruption losses. Standard general liability policies don’t include cyber coverage, so without a dedicated cyber liability policy, your business operates completely exposed to these mounting financial and operational threats. Understanding what your current coverage actually protects is the first step toward closing this gap.

What Your California Cyber Liability Policy Actually Covers

A California cyber liability policy protects you against the specific costs that follow a data breach or cyberattack. Unlike general liability insurance, cyber policies address the financial fallout from incidents that compromise data, disrupt operations, or expose your business to regulatory action. The coverage works across four critical areas: breach response expenses, business interruption losses, legal and regulatory costs, and third-party liability claims. Understanding what each area covers helps you identify whether your current policy limits match your actual exposure.

Breach Response and Notification Expenses

When a breach occurs, notification costs accumulate quickly. You must contact affected individuals through mailings or call centers, often within 30 to 45 days depending on California law. Credit monitoring services for affected customers add substantial expense, especially for breaches affecting hundreds or thousands of people. Forensic investigations to determine how the breach happened and what data was compromised typically cost tens of thousands of dollars. A cyber liability policy covers these direct response costs outside your policy limit in many cases, meaning notification and investigation expenses don’t reduce your available coverage for other claim components. This separation matters because a mid-sized breach can easily generate $50,000 to $150,000 in notification and forensic costs alone. Your policy should explicitly state that breach response expenses are covered under first-party coverage, protecting your cash flow during the critical weeks following an incident.

Business Interruption and Lost Revenue Recovery

Ransomware attacks and system failures don’t just damage your data-they halt operations. A manufacturing company loses production for a week, a healthcare provider cannot access patient records, or a retail business sees their point-of-sale system go offline, and all face immediate revenue loss. Cyber liability policies cover business interruption losses, compensating you for revenue you would have earned during the downtime plus extra expenses incurred to restore operations. This coverage requires detailed documentation of lost revenue and additional costs, so maintain accurate financial records to strengthen your claim. The policy typically covers losses from ransomware attacks, malware infections, and system failures caused by cyberattacks. However, coverage often includes a waiting period-commonly 24 to 72 hours-before business interruption payments begin, so understand your policy’s specific terms.

Legal Defense and Regulatory Fines Under California Law

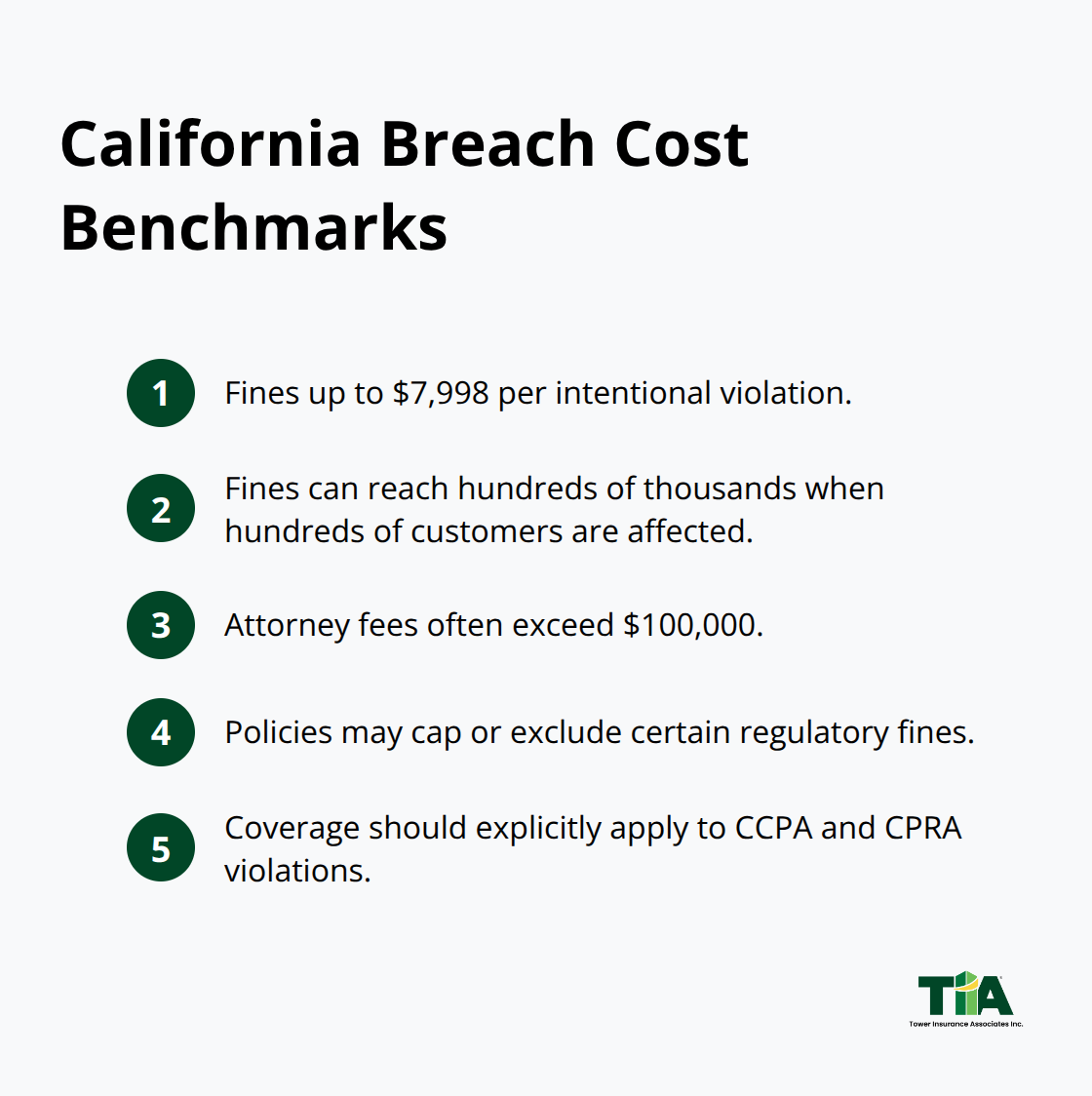

California’s regulatory environment creates substantial legal exposure. Under CCPA and CPRA, regulatory fines can reach up to $7,998 per intentional violation, with a single breach affecting hundreds of customers potentially triggering fines in the hundreds of thousands of dollars. Cyber policies cover legal fees for defending against regulatory investigations and lawsuits from affected individuals. The policy should explicitly cover regulatory fines and penalties under California privacy laws, though coverage varies by insurer. Some policies cap regulatory fine coverage or exclude certain violation types, so verify that your coverage applies to CCPA and CPRA violations specifically.

Attorney fees for managing breach notification, responding to regulatory inquiries, and defending class action lawsuits often exceed $100,000, making this coverage component essential for California businesses.

Third-Party Liability and Supply Chain Exposure

When your breach exposes customer data, affected individuals can sue you for damages. Third-party liability coverage in your cyber policy protects you against these lawsuits. Equally important, if a vendor or service provider in your supply chain suffers a breach that affects your customers or operations, your cyber policy should cover your liability exposure. The July 2024 CrowdStrike incident illustrated how third-party failures cascade through entire industries-a single vendor’s system update crashed millions of customer computers worldwide. Your policy must cover both direct liability from your own breach and liability arising from third-party vendors’ failures. Confirm that your coverage extends to service providers and that the policy limits are sufficient for your customer base size. A business with 50,000 customers needs substantially higher third-party limits than a business with 5,000 customers.

Knowing what your policy covers is only half the battle. The real challenge lies in selecting limits, deductibles, and endorsements that actually match your business operations and risk profile-a decision that requires comparing multiple carriers and understanding how coverage gaps protect your specific vulnerabilities.

Selecting Coverage Limits That Match Your Actual Exposure

Calculate Your Breach Costs Based on Business Size

Choosing the right cyber liability policy for your California business requires three concrete decisions: determining how much coverage you actually need, comparing what different carriers will charge you for that protection, and verifying that the insurer’s incident response team can handle a breach when it happens. Most California business owners select policy limits based on price alone, then discover during a claim that their coverage falls $200,000 short of actual costs. Start with your customer data volume and revenue figures to calculate realistic exposure. A healthcare provider storing 10,000 patient records faces substantially different breach costs than a software company with 50,000 users.

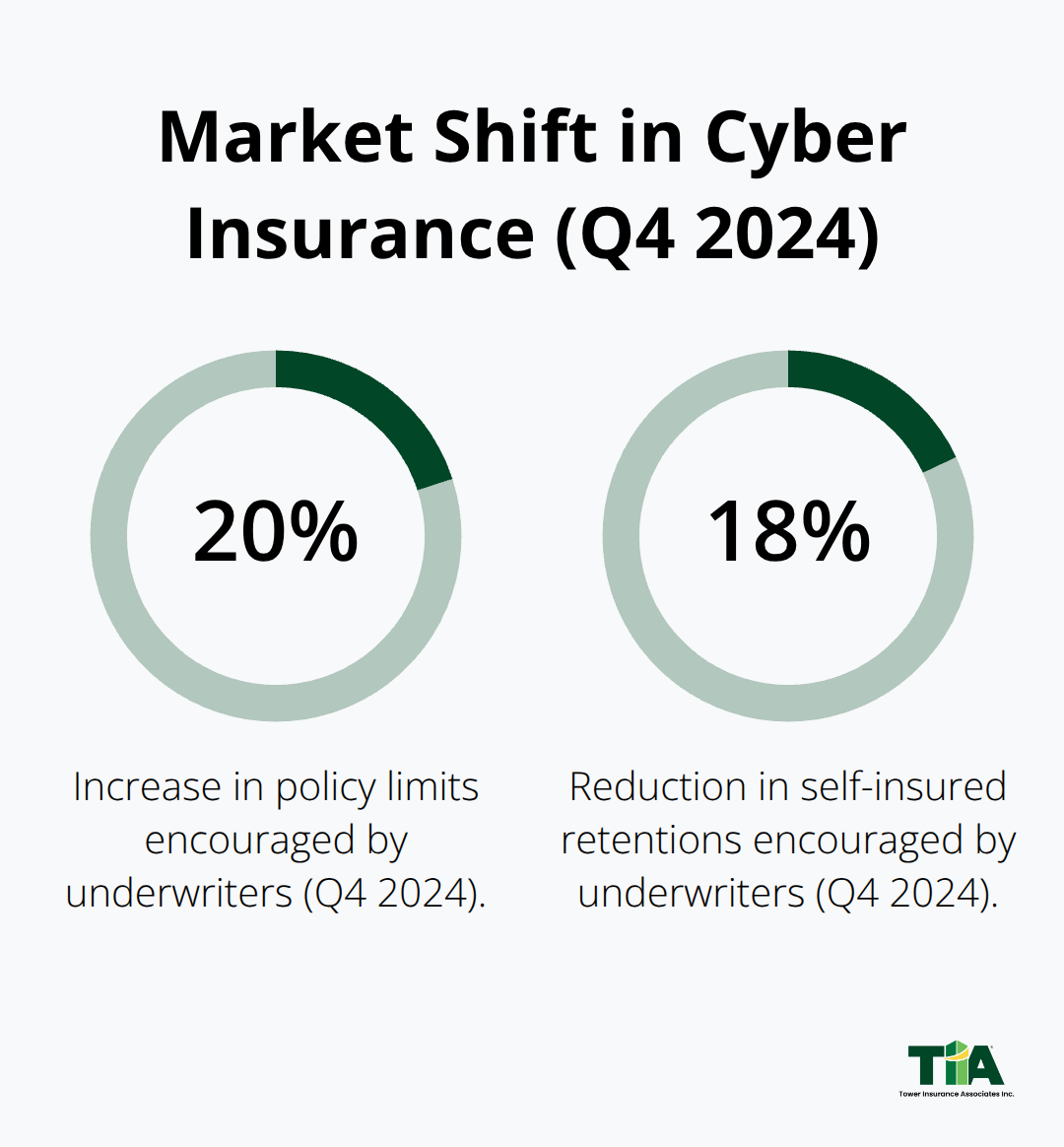

Under California privacy law, notification costs alone for a breach affecting 5,000 people typically run $75,000 to $150,000 when you factor in mailings, call centers, and credit monitoring services. Add forensic investigation costs of $40,000 to $80,000, potential regulatory fines under CCPA of $7,500 per violation, and legal defense fees exceeding $100,000, and a mid-sized breach easily reaches $400,000 to $600,000 in total losses. This calculation matters because Marsh data from Q4 2024 shows underwriters actively encourage higher policy limits-approximately 20 percent increase in limits compared to prior years-while simultaneously reducing self-insured retentions by about 18 percent.

This market shift reflects the reality that breach costs have grown substantially and carriers want policyholders carrying adequate limits to avoid coverage disputes during claims.

Compare Three Measurable Policy Factors

When comparing specific policies, focus on three measurable factors that directly impact your protection. First, verify whether breach response expenses like notification and forensic investigation costs are covered outside your policy limit or count against it-this distinction can mean the difference between recovering $1 million in breach costs or absorbing $200,000 yourself. Second, confirm that regulatory fines under California privacy laws are explicitly covered; some carriers exclude fines entirely while others cap them at $50,000 or $100,000, leaving you exposed to the full penalty amount.

Third, examine the deductible structure carefully because deductibles ranging from $1,000 to $25,000 dramatically affect your out-of-pocket costs during a claim. A $10,000 deductible on a $500,000 breach claim means you absorb that $10,000 yourself, so select a deductible level aligned with your cash flow capacity.

Verify Third-Party and Business Interruption Coverage

Equally critical is verifying that your policy covers third-party service provider breaches-the July 2024 CrowdStrike incident demonstrated how vendor failures cascade into customer liability for downstream companies. Your policy should explicitly state coverage for vendor breaches that affect your operations or customer data. Finally, confirm that business interruption coverage includes the specific attack types your industry faces; ransomware coverage is standard, but some policies exclude coverage for attacks beyond targeted incidents or include time-delay exclusions that deny claims for long-tail threats.

Conclusion

California cyber liability insurance protects your business against the specific financial and operational threats that standard policies ignore. The state’s strict privacy laws, combined with rising attack frequency and escalating breach costs, make dedicated cyber coverage non-negotiable for any California business handling customer data or operating critical systems. Your protection strategy requires three concrete actions: calculate your actual breach exposure by estimating notification costs, forensic investigation expenses, and potential regulatory fines based on your customer data volume and revenue; compare policies on measurable factors like whether breach response costs are covered outside your policy limit and whether regulatory fines under CCPA and CPRA are explicitly included; and verify that your coverage extends to third-party vendor breaches and includes business interruption protection for the specific attack types your industry faces.

The current insurance market favors California businesses seeking comprehensive protection. Marsh data from Q4 2024 shows underwriters actively encourage higher limits and lower deductibles, reflecting a healthier market with increased capacity and competition. This favorable environment means you can secure robust coverage at competitive rates if you act now.

We at Tower Insurance Associates, Inc. help California businesses identify the cyber liability insurance that actually matches their operations and risk profile. As an independent insurance agency in Culver City representing multiple top-rated carriers, we provide personalized service and competitive pricing while acting as your trusted local adviser. Contact us at insurewithtower.com to discuss your specific cyber liability needs and secure the protection your California business requires.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.