Professional liability claims can devastate a firm’s finances and reputation. A single lawsuit can cost tens of thousands in legal fees, settlements, or judgments-money that directly impacts your bottom line.

At Tower Insurance Associates, Inc., we’ve seen firsthand how professional liability risk management separates thriving firms from those struggling to recover. This guide walks you through concrete strategies to protect your business before claims happen.

What Professional Liability Coverage Actually Pays For

Professional liability insurance covers the costs that destroy unprepared firms: legal defense, expert witnesses, court costs, settlements, and judgments when a client alleges your work caused them financial loss. This coverage activates when a claim is made, not when the error occurred, which is why response timing matters enormously. The moment a client threatens legal action, your policy’s claims-made structure means you must notify your insurer immediately to preserve coverage and control the defense strategy. Without this coverage, you write checks from operating capital to pay attorneys while your firm bleeds cash flow during disputes that can drag on for years.

When Claims Actually Strike

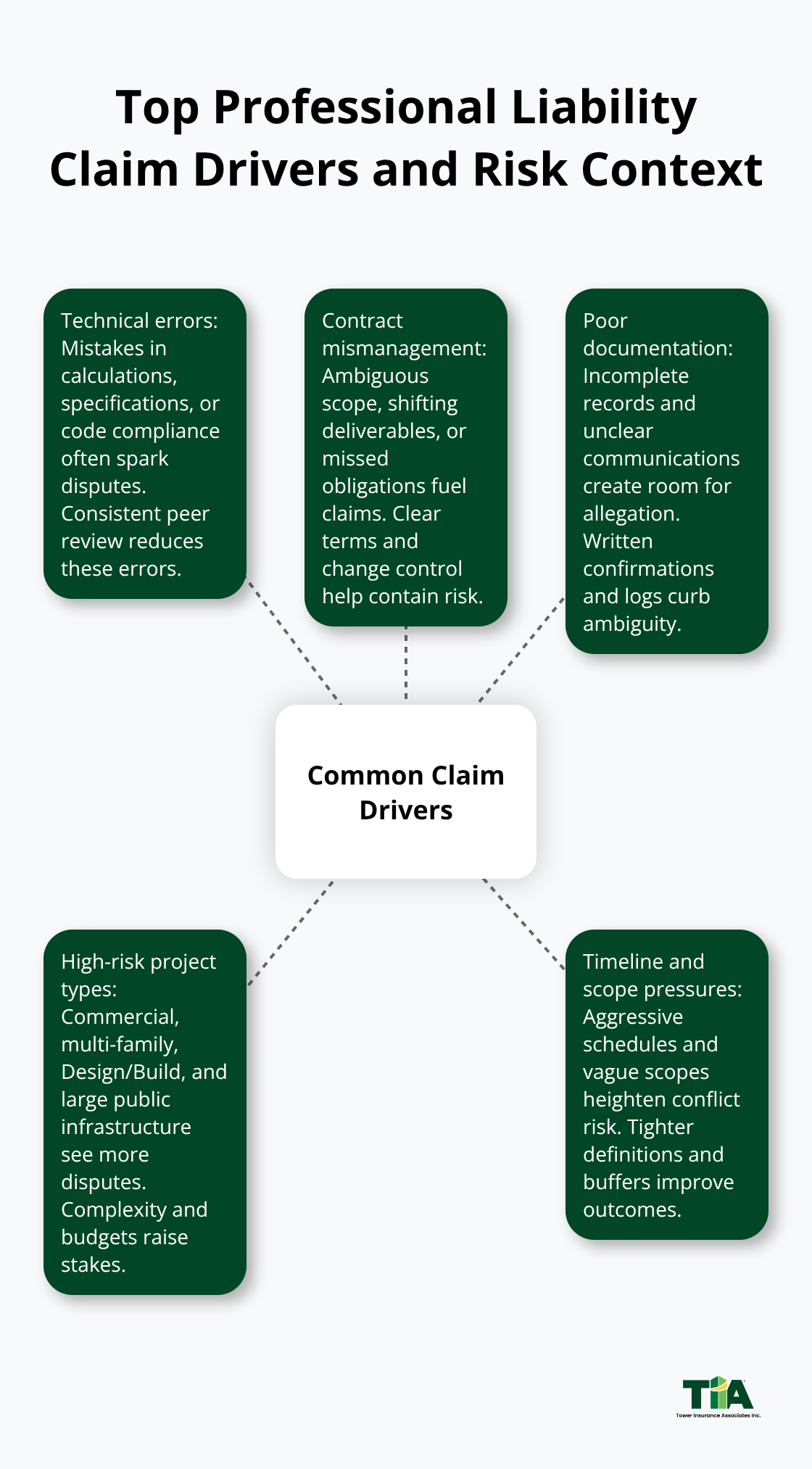

The 2025 Professional Liability Trends report from the AIA, ACEC, and NSPE shows that commercial and multi-family residential projects generate the most claims, followed by single-family residential and transportation work. Technical errors, contract mismanagement, and poor documentation rank as the top three claim drivers-not rare catastrophes, but preventable breakdowns in everyday project execution. Design/Build contracts and large public infrastructure projects carry elevated risk because aggressive timelines, shared responsibilities, and vague scopes create fertile ground for disputes.

A missed deadline that delays financing triggers late fees; a design gap that requires change orders costs the client money; inadequate communication that leaves scope ambiguous invites claims. These scenarios represent the bread and butter of professional liability claims that cost firms between tens of thousands and millions depending on the damage alleged.

Coverage Limits Must Match Your Exposure

Policy limits need to scale with your project size and financial exposure. As average project budgets grow, a $1 million coverage limit becomes dangerously thin if a single commercial project generates a $2 million claim. Nuclear verdicts-jury awards exceeding $100 million-are rising and increasingly affecting underwriting and pricing, particularly in litigation-heavy states (New Jersey, Texas, California, Pennsylvania, New York, Georgia, and Florida). Even if your firm operates in lower-risk states, inflation drives up claim costs across the board, making historical limits obsolete. Coverage exclusions matter too: standard cyber policies exclude claims arising from professional services, so if a data breach exposes client information, your professional liability policy won’t cover the fallout. You need dedicated cyber coverage separate from your E&O policy.

Exclusions Create Hidden Gaps

Most professional liability policies contain specific exclusions that leave firms exposed in critical areas. Cyber liability ranks high on this list-data breaches, ransomware attacks, and system failures fall outside standard E&O coverage, yet clients increasingly demand proof of cyber protection. Environmental exposures (PFAS and broader contamination risks) are on insurers’ radar, so you must understand what your policy excludes before a claim surfaces. Bodily injury claims present another exposure; while some professional liability policies cover bodily injury, others limit or exclude it entirely, yet rising litigation costs make this distinction vital. Your policy documents govern what’s covered and what’s not, so reviewing your actual terms-not just the marketing materials-prevents costly surprises when you file a claim.

The Claims-Made Trigger Changes Everything

Claims-made coverage means your insurer pays only if the claim arrives while your policy is active, not when the underlying error happened. This structure creates urgency: a client who discovers a problem years after project completion can still file a claim, but only if you maintain continuous coverage through that discovery date. Tail coverage (extended reporting period insurance) protects you after you leave a firm or retire, extending claims-made protection beyond your active policy period. Without tail coverage, a claim filed after you stop paying premiums receives no protection, leaving you personally liable for defense costs and damages. Understanding this timing distinction separates firms that recover quickly from claims versus those that face uninsured exposure.

The specific risks your firm faces depend on your project types, contract practices, and staffing stability. Identifying which claims hit your industry hardest-and which coverage gaps expose you most-shapes the protection strategy that actually works for your business.

How to Stop Claims Before They Start

Technical Errors, Contract Gaps, and Poor Documentation Drive Most Claims

The 2025 Professional Liability Trends report from the AIA, ACEC, and NSPE identifies three preventable claim drivers that account for the majority of losses: technical errors, contract mismanagement, and inadequate communication or documentation. These aren’t exotic failures-they’re routine breakdowns in project execution that firms can eliminate through structured controls. The firms that stay claim-free don’t rely on luck; they build systems that catch problems before clients discover them.

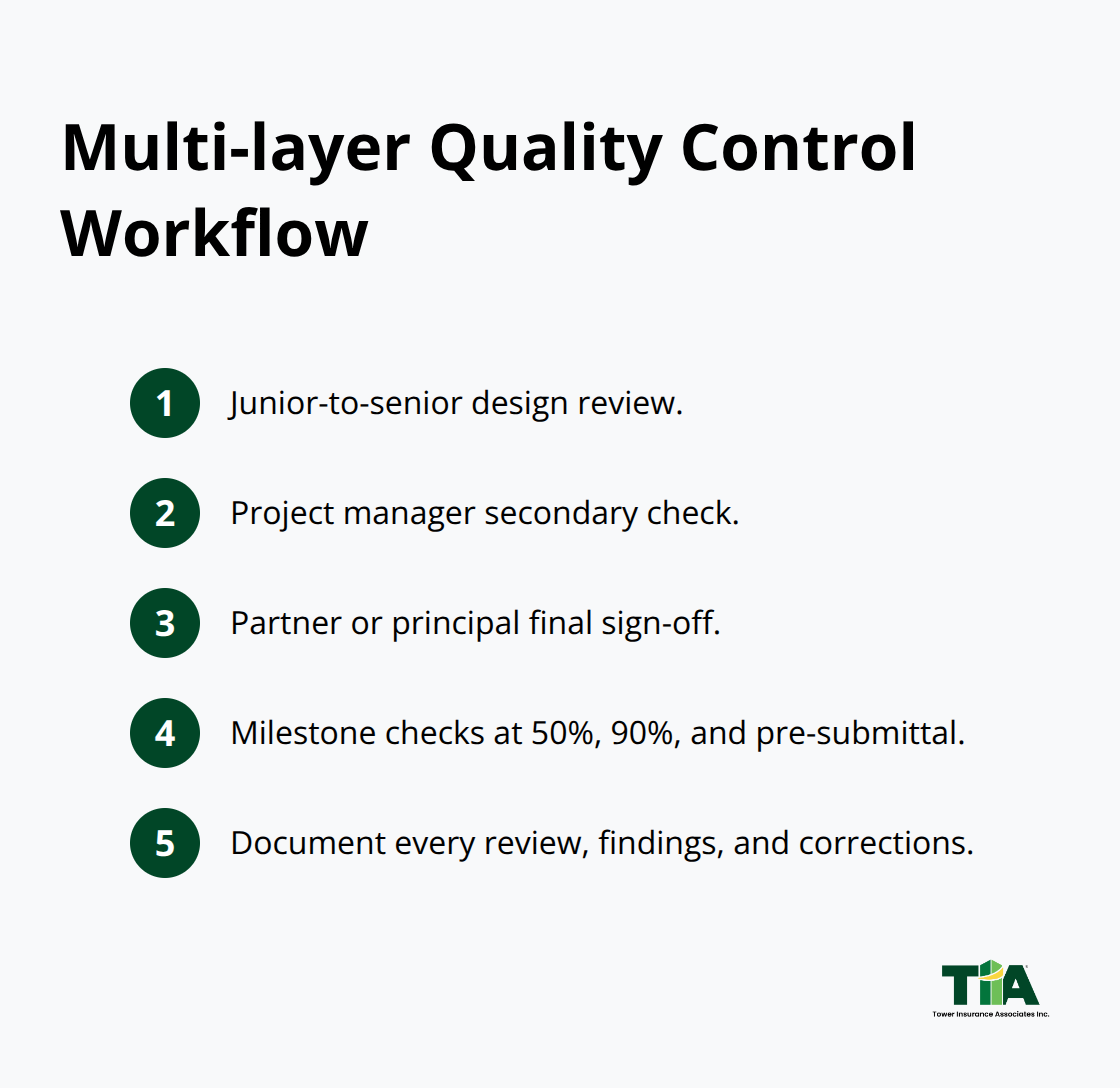

Implement Multi-Layer Quality Control Before Deliverables Leave Your Office

Quality control starts with written procedures that force multiple reviewers to examine work before delivery. A commercial architecture firm should require junior designer work to pass review by a senior architect, then a second check by a project manager, then final sign-off by a partner before the deliverable leaves your office. This multi-layer approach catches calculation errors, missed code requirements, and scope gaps that a single reviewer might overlook.

For engineering or consulting firms, establish explicit checkpoints tied to project milestones-at 50% design completion, at 90%, and again before final submission. Document every review step, who performed it, what they checked, and any corrections made. That paper trail becomes invaluable if a client later claims your firm missed something; your documentation proves you followed a rigorous process.

Documentation discipline matters more than most firms realize because it directly shapes how courts and insurers view your work if a claim surfaces. Maintain a project chronology that records key decisions, client communications, scope changes, and approvals. When a client emails requesting a change in deliverables, respond in writing confirming what you understood, what the change costs, and what timeline applies. Email creates the written record that prevents he-said-she-said disputes years later.

Train Staff on Contracts, Standards, and Evolving Compliance Requirements

Staff training on contract language and compliance standards prevents technical errors that spawn claims. Many design and engineering firms lose claims because junior staff didn’t understand contractual obligations or industry standards that applied to their work. Require annual training on your firm’s standard contract terms, your scope limitations, and the industry standards governing your work-whether that’s building codes, engineering standards, or professional best practices. Track completion and test understanding through brief assessments. Environmental and climate considerations now shape standard-of-care expectations in ways that older staff may not fully appreciate, so annual updates on evolving regulatory requirements keep your team current. When you hire or promote staff, verify that they hold required licenses, certifications, and experience before assigning them to projects; gaps in credentials create liability exposure that insurance won’t cover if a claim arises from unlicensed or unqualified work.

Write Detailed Contracts That Specify Scope, Timeline, and Liability Limits

Contracts and engagement letters set boundaries that protect both your firm and clients. Write detailed scope statements that specify exactly what you will deliver, by what date, and under what conditions. Include explicit statements about what you will not do-if you’re not responsible for environmental assessment, state so in writing. Specify liability limitations that cap your exposure and damages clauses that define what constitutes recoverable loss. Have counsel review your standard agreements regularly to ensure they reflect current law and your actual practice. A vague contract that says you’ll provide engineering services without defining scope, timeline, or deliverables invites disputes; a precise contract that specifies three rounds of revisions, completion by a fixed date, and a $50,000 cap on liability prevents misalignment that generates claims.

These control systems form the foundation of claim prevention, yet they only work if your firm enforces them consistently across every project. The next section examines how to select professional liability insurance that backs up these controls when prevention fails.

Selecting a Carrier That Matches Your Firm’s Risk Profile

Understand Your Carrier’s Industry Expertise

Choosing a professional liability insurer matters far more than most firms realize because not all carriers understand your specific work. The 2025 Professional Liability Trends report from the AIA, ACEC, and NSPE confirms that even with some carriers exiting the market, capacity remains robust due to new entrants, which means you have options-but those options vary dramatically in how well they understand design/build contracts, public infrastructure projects, or specialized consulting work. A carrier that excels at insuring residential architects may lack expertise in transportation engineering or healthcare design, and that gap shows up when you file a claim and discover your insurer doesn’t grasp why your scope decisions made sense under your contract.

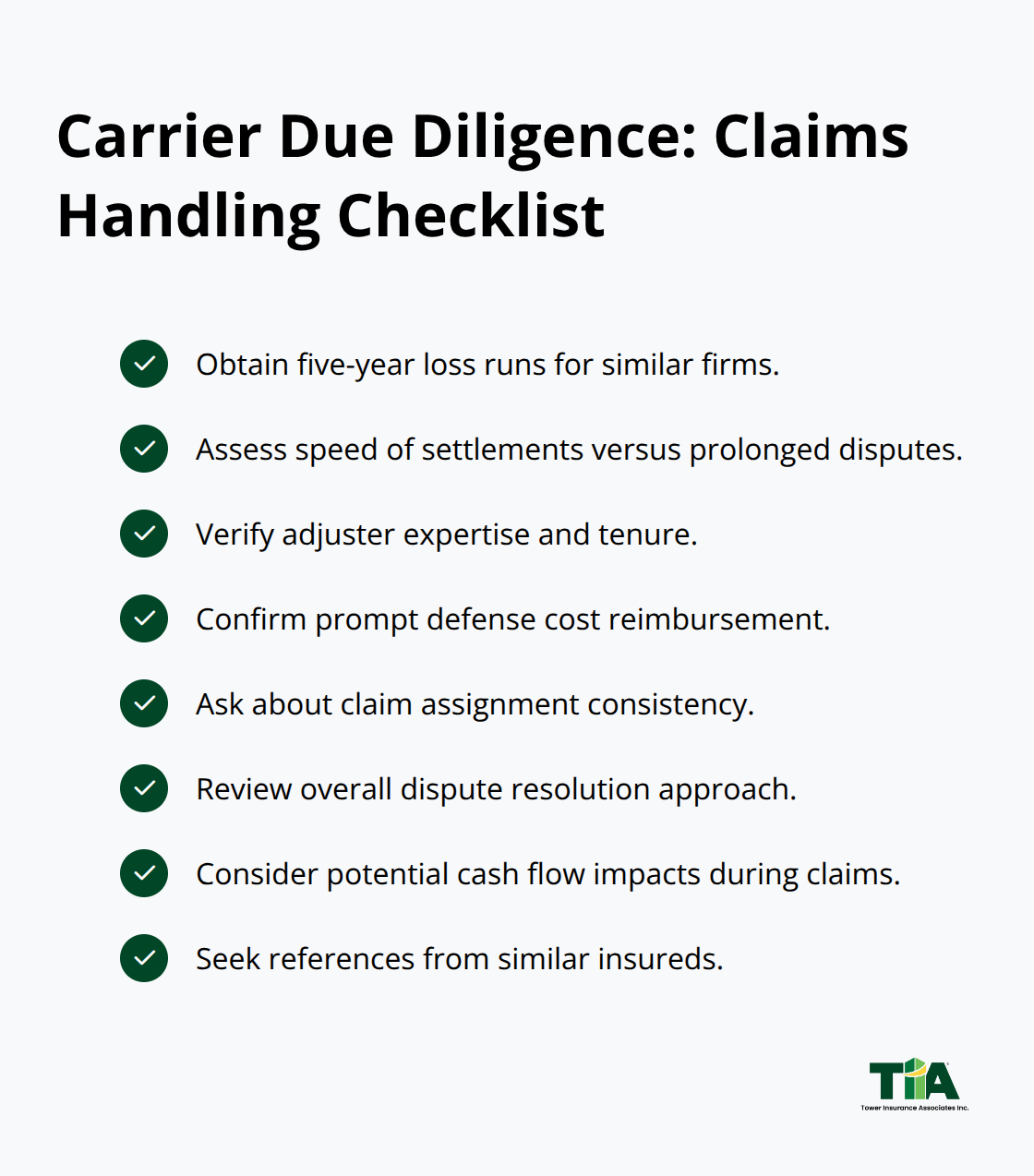

Ask potential carriers directly: Do you insure firms doing this type of work? What percentage of your book is in my sector? Can you reference three firms similar to mine that you’ve insured for five-plus years? Carriers that hesitate or give vague answers don’t understand your niche well enough to defend you effectively when disputes arise.

Evaluate Financial Strength and Claims Handling Practices

Financial strength matters, but it’s not the only factor. A carrier with an A+ rating from AM Best can still deny claims or drag out settlements if their claims team doesn’t comprehend your industry’s standards and practices. Request loss runs from any carrier you’re considering-a detailed record of claims they’ve handled for similar firms over the past five years. Look for patterns: Do they settle claims quickly or fight every allegation? Do they assign experienced claims adjusters or rotate inexperienced staff?

Do they pay defense costs promptly or create cash flow strain by delaying reimbursement?

Pricing matters, but a carrier offering lower premiums while dragging out claims for two years costs you far more in management time and operational stress than a slightly higher premium paired with responsive claims handling.

Account for Regional Litigation Risk and Coverage Gaps

Nuclear verdicts are rising in states like New Jersey, Texas, California, Pennsylvania, New York, Georgia, and Florida, which means carriers in those states face mounting losses and may tighten underwriting or raise rates aggressively. If your firm operates in multiple states, ask how your coverage responds when a claim arises in a litigation-heavy jurisdiction-some carriers apply state-specific deductibles or limit coverage in high-verdict states, creating hidden gaps.

Coverage options also vary: some carriers bundle cyber liability into professional liability policies, while others require separate cyber coverage. Given that clients increasingly demand cyber protection and that data breaches fall outside standard E&O policies, verify upfront whether your carrier offers integrated cyber coverage or requires you to purchase it separately.

Partner with an Agency That Represents Multiple Carriers

An independent agency represents multiple carriers and can match your firm’s risk profile to carriers with deep expertise in your sector, rather than forcing you into a one-size-fits-all product. Tower Insurance Associates, Inc., an independent insurance agency in Culver City, California, represents multiple top-rated carriers and provides personalized service and claims advocacy to find tailored coverage and competitive pricing while acting as a trusted local adviser.

Final Thoughts

Firms that operate without professional liability coverage or weak risk management controls face financial devastation when claims arrive. A single lawsuit drains tens of thousands in legal fees before settlement discussions even start, and if your firm loses, you pay judgments from operating capital that should fund payroll, equipment, and growth. Uninsured claims force difficult choices: deplete cash reserves, take on debt, or cut staff to survive the financial hit.

The firms that thrive build professional liability risk management into their operations before problems surface. They implement quality control systems that catch errors before deliverables leave the office, write contracts that specify scope and liability limits so clients understand exactly what they’re paying for, and train staff on compliance standards so junior team members don’t create exposure through ignorance. These controls reduce claims frequency and severity, which lowers your insurance costs and protects your reputation.

Professional liability insurance backs up these controls by paying defense costs, expert witnesses, and settlements when prevention fails. We at Tower Insurance Associates, Inc. help firms in California and beyond build comprehensive professional liability protection tailored to their specific work, match your firm’s risk profile to carriers with deep expertise in your sector, and provide claims advocacy when disputes arise. Contact us at https://insurewithtower.com to discuss your coverage needs and build a risk management plan that protects your firm’s financial future.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.