A D&O claims process can feel overwhelming when your organization faces a lawsuit or regulatory action targeting directors and officers. At Tower Insurance Associates, Inc., we’ve guided countless clients through this journey, and we know that understanding each step makes all the difference.

This guide walks you through what happens from the moment you notify your insurer to the final resolution, so you can navigate with confidence.

What D&O Insurance Actually Covers

D&O insurance protects your organization’s leaders from personal financial devastation when lawsuits or regulatory actions target their decisions. This coverage pays for defense costs and settlements when directors and officers face allegations of wrongful acts in their professional capacity. The protection extends to the individual executives themselves, not just the company, which matters because personal assets can be at stake. Without this coverage, a single lawsuit can drain personal savings, retirement accounts, and home equity.

Five Primary Sources of D&O Claims

D&O claims stem from five primary sources that appear across industries. Fiduciary duty breaches occur when directors prioritize personal interests over company interests, such as approving unfavorable asset sales to connected parties or failing to act during financial distress when creditors demand accountability. Misrepresentation claims arise when financial performance, human resources capabilities, or contract fulfillment are overstated to win business, then the company cannot deliver on promises. Intellectual property theft happens when departing executives take trade secrets or licenses to competitors, creating unfair competition liability for the organization’s leadership. Employment practices violations include wrongful termination based on protected characteristics like gender, age, or race, exposing directors to personal liability alongside the company. Securities and disclosure failures occur when offering documents contain inaccurate information or material facts are omitted from investor communications, triggering shareholder lawsuits and regulatory investigations.

Why These Claims Matter Most

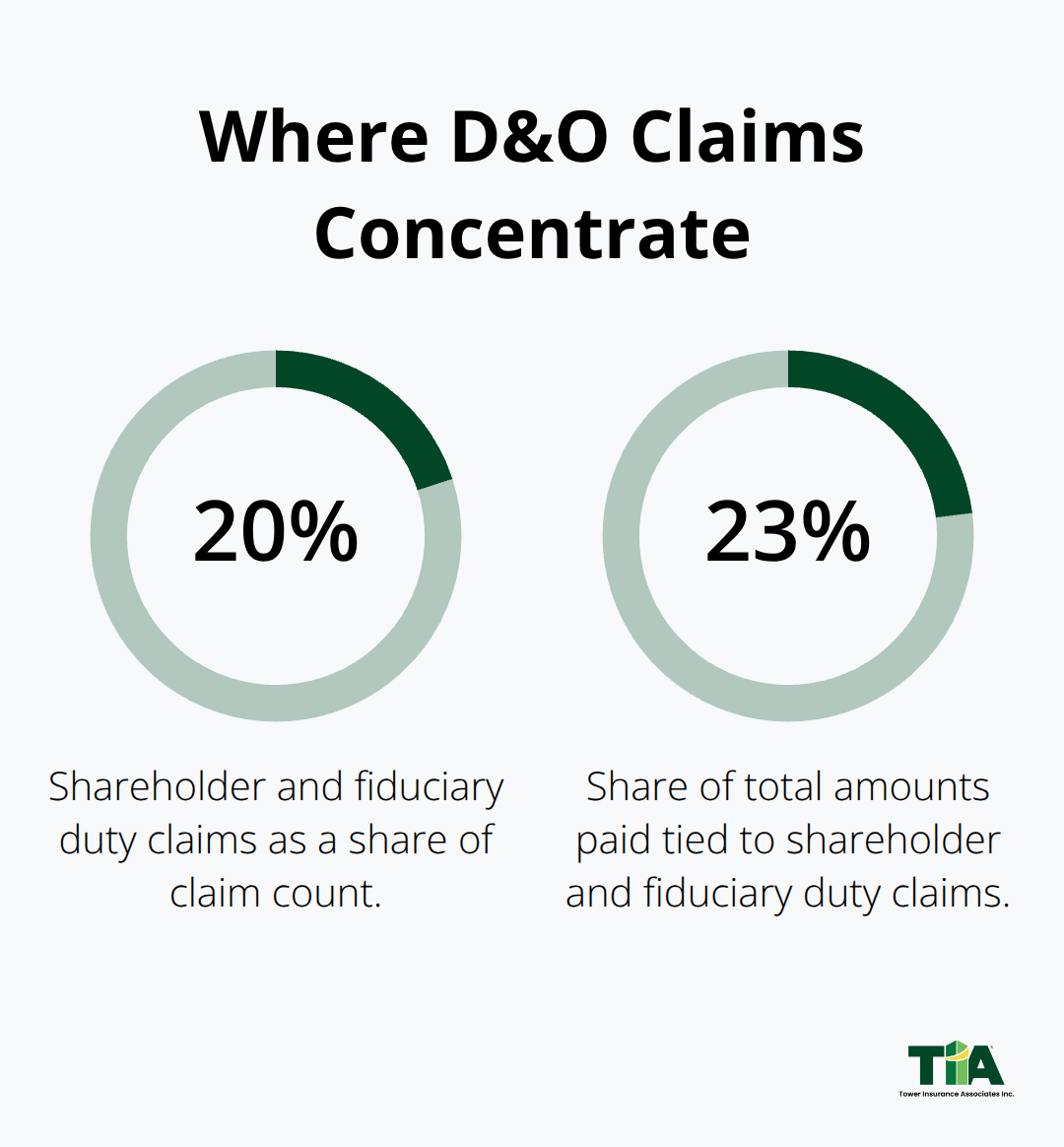

Breach of fiduciary duty and misrepresentation account for the majority of D&O claims filed, with shareholder and fiduciary duty claims representing 20% of claim count and nearly one quarter (23%) of amounts paid. Understanding your specific exposure in these areas helps determine whether your current coverage limits are adequate for your organization’s risk profile. The financial stakes demand that you examine your D&O policy carefully before a claim arises.

Coverage Gaps That Surprise Organizations

Many organizations discover too late that their D&O policies exclude certain claim types or cap coverage at inadequate levels. A policy may cover regulatory investigations but exclude securities claims, or it may protect the company entity while leaving individual directors exposed. Your policy’s specific language determines what the insurer will actually pay when a claim lands on your desk. This is why the notification process itself-which we cover in the next section-requires immediate attention to your policy terms and prompt communication with your insurer.

Getting the Notice Right From Day One

The moment a lawsuit lands or a regulatory investigation begins, contact your D&O insurer immediately. This is not optional, and delays cost money. Most D&O policies require timely notice within 30 to 60 days, and missing that deadline gives insurers legal grounds to deny your entire claim. A written notice alleging a wrongful act triggers coverage, and even emails or counterclaims count as formal notice under most policies. Contact your insurance broker or outside counsel if you’re uncertain whether a particular situation qualifies as a claim, because when in doubt, you notify. The insurer will assign a claims adjuster and begin their initial assessment immediately upon notification. Failure to provide timely notice may result in the insurer disclaiming coverage not just for the claim itself but for related claims that follow, multiplying your financial exposure. Your policy likely specifies the exact method and contact person for notice, so follow those instructions precisely rather than assuming any communication will suffice.

Organize Your Documentation Before You Call

Gather your original policy documents, all endorsements, and any amendments before making that notification call. Have the incident report, legal filings, and internal communications about the disputed conduct ready to reference. The insurer will ask specific questions about dates, parties involved, and the nature of the allegations, so having this information organized prevents delays and demonstrates your organization takes the matter seriously. After notification, the insurer will request substantially more documentation including financial records, regulatory notices, witness statements, and internal incident logs. Organize these materials by category and timeline rather than dumping everything at once, because insurers process claims faster when documentation is logical and complete. If your organization has separate legal counsel already engaged, coordinate with them on what documentation to preserve and what to withhold under attorney-client privilege, because sharing privileged materials with the insurer can waive that protection.

The Insurer’s Initial Response Happens Quickly

Expect the insurer to acknowledge receipt and assign an adjuster within 48 to 72 hours. That initial response is quick because the insurer wants to preserve evidence and understand the claim’s basic facts. The detailed investigation phase takes considerably longer, typically running four to eight weeks depending on claim complexity. During this phase, the insurer interviews relevant parties, gathers additional evidence, and conducts legal and financial analysis to determine claim validity and scope. Cooperate completely by providing requested documents promptly and facilitating meetings, because resistance or delays signal problems to the insurer and can create coverage disputes later. Keep your insurer updated on significant developments without waiting for them to ask, because surprises discovered during their investigation damage credibility and settlement negotiations.

What Happens During the Investigation Phase

The investigation moves through distinct stages that require your active participation. The insurer’s team examines your policy language to identify covered versus non-covered matters, which affects how defense costs get allocated and reimbursed. They review the facts surrounding the alleged wrongful act and assess potential liability exposure based on similar cases and legal precedent. Financial analysis follows, where the insurer estimates damages, defense costs, and settlement ranges to understand the claim’s scope. Settlement discussions rarely begin until the insurer completes their investigation and forms an opinion on liability exposure, so patience during this phase is necessary even though it feels like nothing is happening. Your cooperation throughout this stage-providing documents on time, answering questions directly, and maintaining transparency-accelerates the process and positions your organization favorably when negotiations begin.

Defense Counsel and Insurer Investigation Work in Parallel

How Defense Counsel and Insurer Teams Coordinate

Defense counsel and your insurer’s investigation team operate simultaneously, and this matters because how they coordinate directly affects your costs and settlement timeline. Once you notify the insurer and provide initial documentation, the insurer will typically require you to engage defense counsel from either their approved panel or independent counsel depending on your policy language and state law requirements. Many D&O policies mandate that the insurer preapprove your choice of defense counsel before you incur costs, so contact your insurer immediately before hiring your own attorney. Independent defense counsel has a duty to you even when the insurer pays the bills, which means they represent your interests separately from the insurer’s interests when those diverge.

The Insurer’s Parallel Investigation Process

The insurer’s investigation team simultaneously evaluates claim validity by analyzing your policy coverage, reviewing the factual allegations, and estimating potential damages and defense costs. This dual process typically runs four to eight weeks for straightforward claims and considerably longer for complex securities or fiduciary duty allegations. Defense counsel focuses on building your legal position and challenging the plaintiff’s case, while the insurer’s team assesses financial exposure and settlement value. Neither team operates in isolation-your defense counsel must update the insurer on case developments regularly and obtain written consent before settlement discussions begin, because settlement proposals without insurer approval can give the insurer grounds to disclaim coverage entirely.

Billing Guidelines and Cost Management

The insurer will require defense counsel to follow specific billing guidelines and reporting protocols, and noncompliance reduces reimbursement or creates disputes over what costs the insurer will actually pay. Defense costs alone in D&O claims frequently reach six figures, with complex cases exceeding $750,000 or more before any settlement payment occurs. Submit defense counsel invoices regularly to maintain reimbursement momentum after any deductible or retention. Clear delineation of time entries for covered versus non-covered matters on invoices streamlines the insurer’s review and accelerates payment processing.

Settlement Negotiations and Authority

Settlement negotiations succeed when both sides understand the actual financial exposure and litigation costs. Settlements in fiduciary duty and misrepresentation cases range from mid-six figures to multiple millions, and shareholder derivative actions commonly settle in the $750,000 range or higher. Your insurer uses the investigation findings to establish a settlement authority-the maximum amount they will approve for settlement-and this number drives negotiation strategy. Experienced D&O defense counsel will propose settlement discussions only when the insurer completes their investigation and determines the claim has real exposure, because settling too early leaves money on the table while settling too late means mounting defense costs that could have purchased resolution.

Accelerating Resolution Through Alternative Dispute Resolution

Mediation or arbitration often accelerates settlement when direct negotiation stalls, and many D&O policies provide coverage for mediator fees and arbitration costs. Maintaining transparency between you, your defense counsel, and the insurer throughout negotiations prevents coverage disputes that outlast the underlying claim itself. Hidden communications or settlement discussions conducted without insurer knowledge create problems that extend well beyond the original claim resolution.

Final Thoughts

The D&O claims process from notice to resolution demands preparation, transparency, and experienced guidance at every stage. Organizations that notify their insurers promptly, organize documentation systematically, and cooperate fully with investigators experience faster resolutions and better outcomes. Defense costs in fiduciary duty and misrepresentation cases frequently exceed $750,000, and settlements often reach six or seven figures, which underscores why adequate coverage matters before a claim arrives.

Your best protection against D&O exposure starts with strong governance practices. Accurate financial reporting, transparent disclosures in offering documents, proper intellectual property controls, and clear conflict-of-interest policies reduce the likelihood that claims arise in the first place. Regular board training on fiduciary duties and employment law compliance prevents the costly mistakes that trigger shareholder lawsuits and regulatory investigations.

Selecting the right D&O coverage requires honest assessment of your specific risks. A manufacturing company faces different exposures than a software firm, and a private company has different shareholder dynamics than a public corporation. Your policy should cover regulatory investigations, securities claims, and employment practices violations without gaps that leave individual directors exposed, and coverage limits must reflect your organization’s size, industry, and transaction activity. Contact us at Tower Insurance Associates, Inc. to find D&O coverage that matches your actual risk profile rather than settling for generic policies.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.