California directors and officers face mounting legal exposure from shareholder disputes, employment claims, and regulatory investigations. The costs of defending against these lawsuits-even when companies win-can devastate leadership and drain company resources.

At Tower Insurance Associates, Inc., we’ve seen firsthand how California D&O insurance protects executives when litigation strikes. This guide walks you through the coverage you need and how to evaluate your current protection.

What Claims Actually Threaten California Directors and Officers

Securities Litigation and Shareholder Exposure

California directors and officers face three distinct liability threats that drain personal finances and derail careers. Securities class actions remain the most expensive. California companies faced 225 federal securities class action filings in 2024, with median settlements exceeding $13.5 million. These lawsuits allege breach of fiduciary duty, mismanagement, or disclosure failures-and they hit personal assets when the company cannot indemnify leadership.

Employment practices claims form the second major exposure. California’s pro-employee legal environment generates claims around wrongful termination, discrimination, harassment, and wage violations at rates higher than most states. A single employment lawsuit costs $100,000 to $500,000 in defense alone before settlement.

Regulatory Investigations and Personal Defense Costs

Regulatory investigations from the California Attorney General or the SEC represent the third threat. The SEC launched 47 enforcement actions targeting ESG disclosure violations in 2024, signaling aggressive board-level scrutiny. Directors and officers pay defense costs personally unless coverage applies, which can exceed $250,000 in complex investigations.

Most directors assume the company pays for their legal defense. California law rarely works that way. When a shareholder sues alleging breach of fiduciary duty, the company cannot indemnify its own leadership because the company is the defendant. Defense costs mount immediately-expert witnesses, depositions, and motion practice easily consume $50,000 to $150,000 in the first six months of litigation.

The WTW FINEX Observer reported that average securities class action settlements in 2024 reached approximately $43 million, with first-half 2024 settlements averaging around $26 million. Most directors lack personal liquidity to cover these expenses while litigation proceeds. D&O insurance advances defense costs as the case progresses, preventing cash-flow crises that force leaders to settle unfavorable claims or exhaust personal savings.

Climate Disclosure and Insolvency Risk

California’s climate-disclosure requirements under SB 219 and SB 253 create direct board-level exposure that did not exist three years ago. Companies must report Scope 1 and 2 emissions in 2025–2026, with overlapping state and federal SEC requirements. Boards that misreport or omit material emissions data face shareholder derivative actions, SEC investigations, and personal liability for individual directors who approved the filings.

Bankruptcy risk amplifies this exposure. Bankruptcies rose approximately 33 percent year-over-year in 2024, with 22,762 filings according to available data. Directors of insolvent companies face claims for unpaid wages, benefits, and tax obligations-liabilities that attach personally if governance fails.

Cyber Breaches and Accelerated Litigation

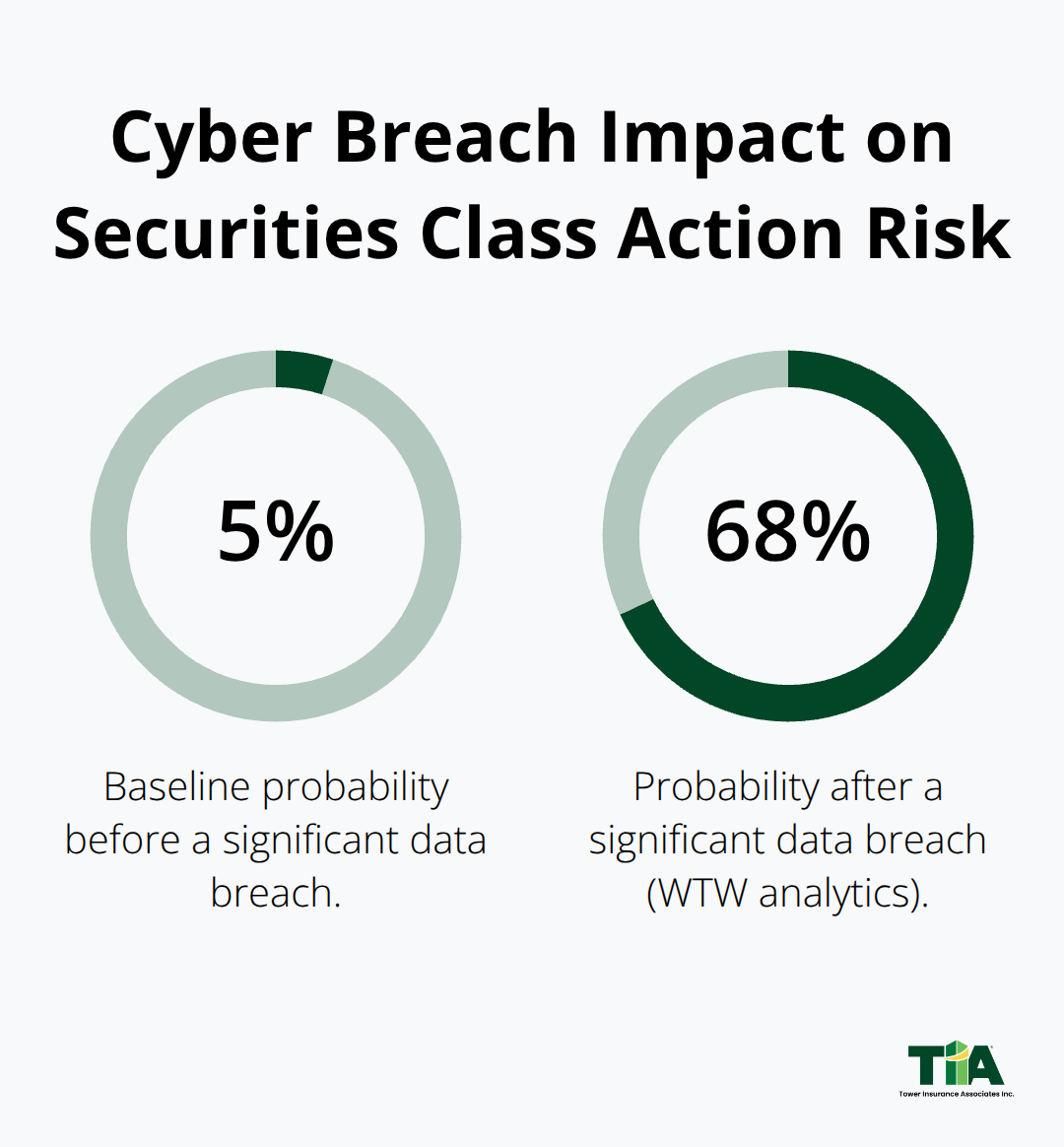

A cyber breach further accelerates litigation risk. After a significant data breach, the probability of a securities class action jumps from 5 percent to 68 percent according to WTW analytics. This means a board-level cybersecurity failure today becomes shareholder litigation tomorrow.

Side A coverage specifically protects personal assets when indemnification is unavailable-this is non-negotiable for California leadership. Without it, a director faces personal bankruptcy even if ultimately vindicated.

D&O coverage that excludes cyber-related claims or defense costs leaves leadership catastrophically exposed. The next section examines which coverage areas matter most when evaluating a D&O policy for your organization.

What Each Coverage Layer Actually Protects

Understanding Side A and Side B Protection

D&O policies contain multiple coverage layers, and most directors misunderstand which layer covers which exposure. Side A coverage protects personal assets when the company cannot or will not indemnify leadership-this is the non-negotiable piece. Side B reimburses the company when it indemnifies directors and officers for defense costs and settlements. Entity coverage protects the organization itself from management liability claims.

The problem runs deep: many California directors purchase policies with inadequate Side A limits while overfunding Side B, leaving personal assets exposed when litigation hits hardest. The 2024 data reveals the danger. Median securities class action settlements reached $14 million in 2024, and average settlements reached $43 million. A director with $5 million in Side A coverage faces $9 million in uninsured exposure on a median case.

Side A should never sit subordinated to Side B. If Side B funds exhaust, your personal protection vanishes. This distinction matters more in California than anywhere else because shareholder derivative actions increasingly target individual directors rather than the company.

Sizing Limits Based on Company Profile

When sizing limits, start with your company’s litigation history and asset base. Public companies and venture-backed firms need $10–$25 million minimum. Private companies with $50–$500 million in revenue typically require $5–$10 million. Startups seeking Series A or B funding should carry at least $3–$5 million to reassure investors.

The calculation is straightforward: your Side A limit should cover expected defense costs plus potential settlements. Defense costs alone in securities litigation run $250,000 to $500,000 before trial. Add settlement exposure and the math becomes clear-underfunding Side A creates catastrophic personal risk.

Employment Practices and Fiduciary Coverage

Employment practices liability coverage handles wrongful termination, discrimination, harassment, and wage-and-hour claims-California’s largest source of D&O exposure after securities litigation. This coverage advances defense costs immediately, which matters because a single employment lawsuit costs $100,000 to $500,000 in legal fees before any settlement.

Fiduciary liability and breach-of-duty coverage extends protection to pension plans, health and welfare funds, and 401(k) administration. California directors face mounting claims for failure to monitor investment performance, inadequate disclosures to plan participants, and mismanagement of plan assets. Defense costs in fiduciary claims run $150,000 to $400,000, and settlements average $500,000 to $2 million for mid-sized plans.

Evaluating Policies and Underwriting Standards

Obtain sample policies from at least three carriers before purchase, and have counsel review coverage definitions. Confirm that defense costs are advanced rather than reimbursed-this distinction prevents cash-flow crises during litigation. Underwriters scrutinize governance controls, cyber-risk assessments, board records, and ESG performance before quoting.

A board that documents regular risk reviews, conducts annual cyber audits, and maintains detailed meeting minutes receives better pricing and faster underwriting decisions than one that treats governance as administrative overhead. This governance readiness signals to carriers that leadership understands exposure and manages risk actively. Consider an extra layer of protection through umbrella insurance policies to safeguard your assets beyond standard D&O coverage.

The next section examines how to evaluate your current coverage against California’s specific regulatory landscape and litigation trends.

Why California Businesses Cannot Afford Weak D&O Coverage

The True Cost of Underinsured Leadership

California’s litigation landscape has fundamentally shifted. Defense costs that seemed catastrophic five years ago now represent the opening salvo in disputes that routinely exceed $43 million in settlements. The WTW FINEX Observer documented that average securities class action settlements in 2024 reached $43 million. These figures represent the cost of miscalculating D&O protection. A director with $5 million in Side A coverage faces $8 million to $38 million in uninsured personal exposure on a median or average case. That gap translates to personal bankruptcy, asset seizure, and career destruction even when litigation ultimately vindicates leadership’s decisions.

Employment Practices Claims Compound Personal Exposure

Employment practices claims compound this exposure because California’s pro-employee legal environment generates wrongful termination, discrimination, and wage-violation lawsuits at rates that dwarf other states. A single employment lawsuit consumes $100,000 to $500,000 in defense costs before settlement negotiations begin. Many directors discover their D&O policies exclude employment practices entirely or cap coverage at inadequate limits. This gap leaves leadership personally liable for defense costs that mount immediately once a claim arrives.

Cyber Breaches Accelerate Shareholder Litigation

Cyber breaches accelerate the timeline further. WTW analytics show that the probability of securities class action litigation jumps from 5 percent to 68 percent following a significant data breach. A board-level cybersecurity failure today becomes shareholder litigation tomorrow. Policies that exclude cyber-related claims or fail to cover defense costs in breach scenarios leave leadership catastrophically exposed. The connection between data loss and shareholder litigation has become direct and measurable.

The Mathematics of Modern Litigation Demand Action

The mathematics of modern litigation demand that California directors stop treating D&O insurance as optional risk management and start treating it as foundational to personal financial survival. Strong D&O protection with adequate Side A limits, employment practices coverage, and explicit cyber defense-cost provisions separates leadership that survives litigation from leadership that faces personal ruin. Weak coverage creates the illusion of protection while leaving personal assets undefended when settlements and defense costs mount fastest.

Final Thoughts

California D&O insurance protects your leadership team against the litigation realities that define the state’s business environment. Median securities settlements exceed $13.5 million, employment practices claims consume $100,000 to $500,000 in defense costs alone, and cyber breaches trigger shareholder litigation 68 percent of the time. Directors without adequate Side A coverage, employment practices protection, and explicit cyber defense-cost provisions face personal financial ruin even when courts ultimately vindicate their decisions.

Start your coverage review by examining your policy’s Side A limit against your company’s litigation exposure and asset base. Confirm that defense costs advance rather than reimburse, preventing cash-flow crises during active litigation. Verify that employment practices liability and cyber-related claims receive coverage without subordination to other layers, and request sample policies from multiple carriers for counsel review before renewal.

We at Tower Insurance Associates, Inc. tailor California D&O insurance to match your organization’s specific risk profile and regulatory environment. Contact us today to conduct a comprehensive coverage review and strengthen your leadership’s financial security against California’s dynamic litigation landscape.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.