One mistake in your professional services can trigger a lawsuit that drains your savings and reputation. California professional liability insurance protects your business when clients claim you failed to deliver promised results or caused them financial harm.

At Tower Insurance Associates, Inc., we’ve seen too many California business owners operate without this coverage, only to face devastating claims they couldn’t afford. The right policy covers your legal defense costs and settlements, letting you focus on running your business instead of worrying about financial ruin.

What Professional Liability Insurance Actually Covers

The Core Protection Your Business Needs

Professional liability insurance protects your California business when clients claim you made a mistake, gave bad advice, or failed to deliver promised results. This coverage pays for your legal defense costs and any settlements or judgments up to your policy limits. In many cases, average defense costs fall between $10,000 and $20,000, although more complex disputes can exceed that range. The policy covers allegations of negligence, errors in service delivery, misrepresentation, omissions, and violations of good faith and fair dealing. If a client sues, your insurer covers attorney fees, expert witness costs, and the final settlement or judgment. Without this coverage, you personally absorb these expenses, which can devastate your finances and force you to shut down operations.

Legal Requirements in California

California law requires professional liability insurance for certain professions. Lawyers who are shareholders in professional law corporations, LLP partners, or Registered Foreign Legal Consultants must carry coverage under California Corporate Code Section 16956. Real estate professionals, architects, engineers, and many consultants face client contracts that specifically demand proof of coverage before they can work. Even if your industry doesn’t legally mandate it, operating without coverage is reckless.

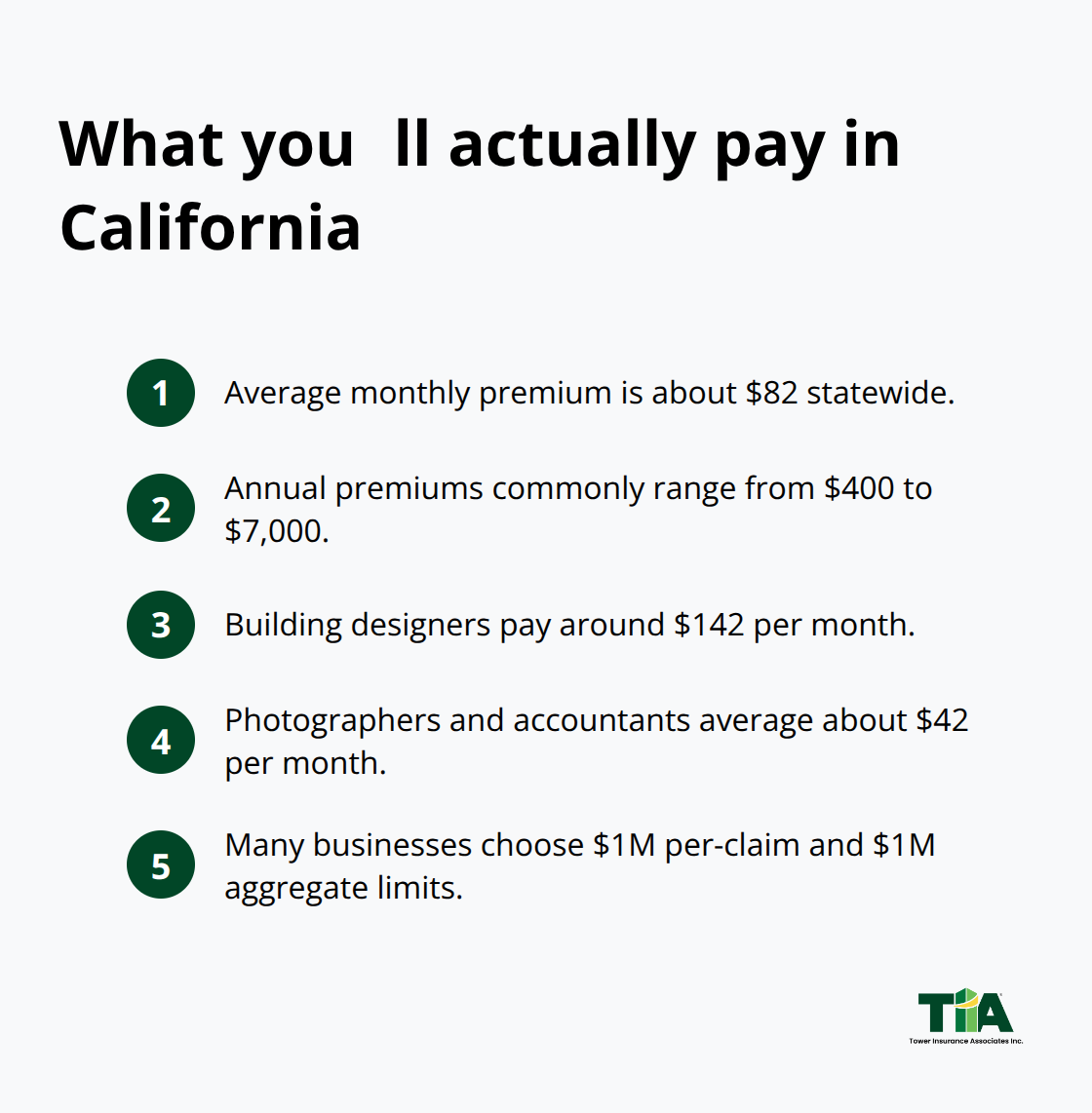

What You’ll Actually Pay

According to Insureon data, professional liability in California averages about $82 per month, with annual premiums typically ranging from $400 to $7,000 depending on your industry and business size. Building designers pay around $142 monthly, while photographers and accountants average about $42 monthly. Most California businesses choose $1 million per-claim and $1 million aggregate limits, which costs far less than a single lawsuit.

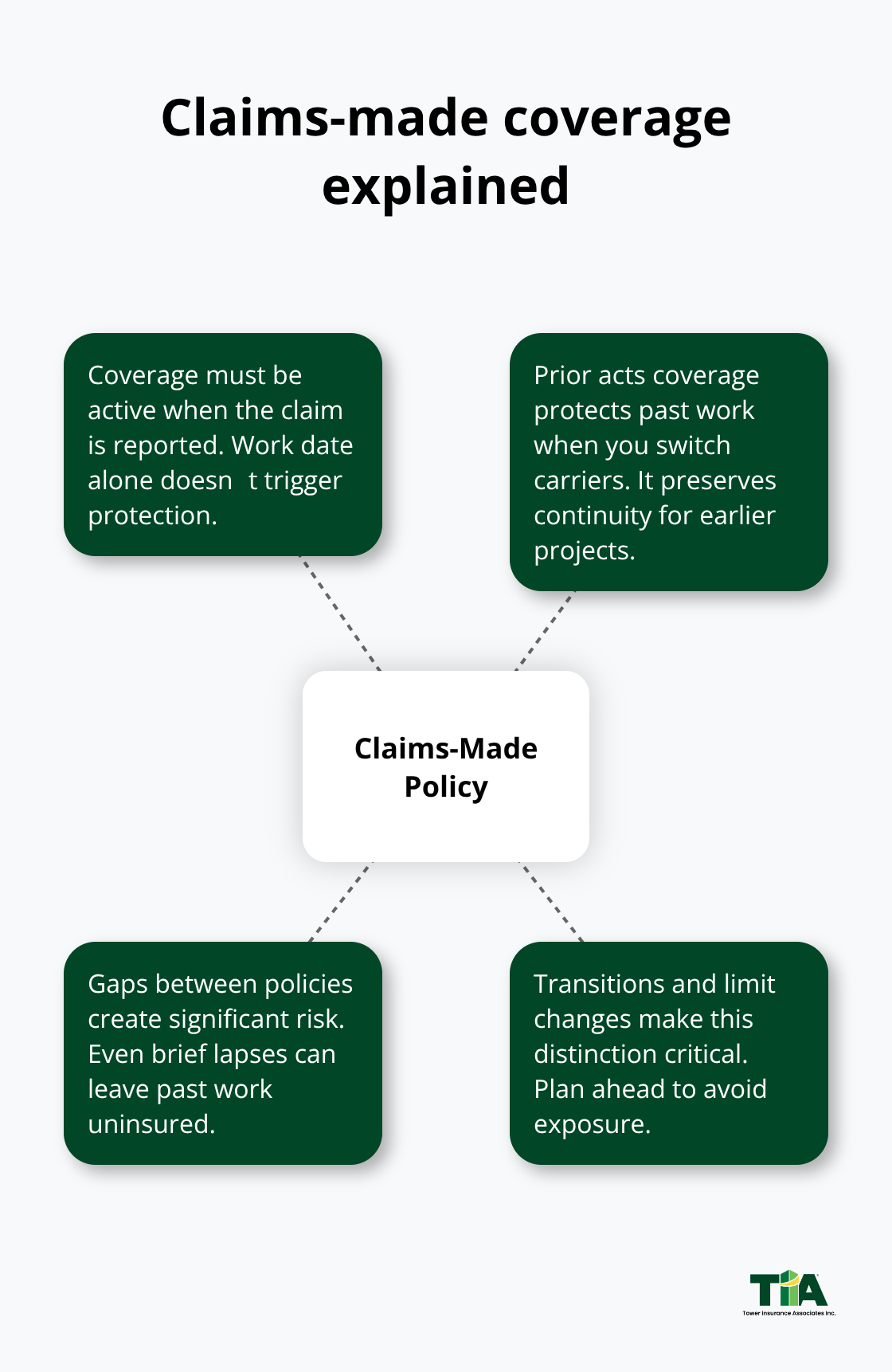

Claims-Made Coverage and Policy Transitions

The coverage operates on a claims-made basis, meaning the policy must be active when a claim is reported to trigger protection. When you switch carriers, your new policy should include prior acts coverage to protect work performed before the transition and avoid gaps that could leave past projects uninsured. This distinction matters significantly when you change insurance providers or update your coverage limits.

What Happens When Claims Actually Hit Your Business

How Real Claims Unfold in California Service Industries

The moment a client claims you made a mistake, your professional liability policy either protects you or leaves you exposed. Real claims in California arrive constantly across service industries, and they follow predictable patterns that matter to your coverage decisions. A designer who failed to follow a client’s specifications faces a lawsuit for the cost of rework plus lost business opportunity. An IT consultant who gave faulty cybersecurity advice ends up liable when the client gets breached and loses customer data. A real estate agent who omitted key property details during a transaction gets sued for the difference in market value. These aren’t hypothetical scenarios-they happen regularly, and defense costs alone can reach $50,000 to $200,000 before trial. Your policy pays these defense expenses and any settlement or judgment up to your chosen limits, which means the difference between staying solvent and facing personal bankruptcy.

The True Cost of Defense and Settlements

The financial reality of claims extends beyond what most business owners anticipate. A single negligence claim can allege that you violated your duty to the client, failed to exercise reasonable care, or breached an implied contract to deliver results. Your insurer covers the legal team that fights these allegations, the expert witnesses who testify on your behalf, and the eventual settlement if the case resolves. Without coverage, you hire and pay those lawyers yourself-immediately and out of pocket.

Architects and engineers in California face particularly high exposure because their errors directly affect building safety and cost thousands to remedy. Accountants face claims when tax advice causes client losses, and consultants get sued when their recommendations fail to produce promised outcomes. The financial burden hits hardest when you operate without coverage, forcing you to liquidate business assets or personal savings to pay legal fees.

Why Claims-Made Coverage Creates Hidden Risks

The claims-made structure of your policy means coverage must be active when the claim arrives, not when the work happened, which is why gaps between carriers expose you to significant risk. When you transition to a new insurer, prior acts coverage becomes essential because old projects can generate claims years later. Most California professionals who’ve faced claims report that the stress of litigation and the uncertainty of outcomes damage their business reputation faster than the financial hit itself.

This reality makes continuous coverage non-negotiable for anyone serving clients in high-stakes industries. A lapse in coverage-even a brief one during a carrier transition-can leave past work completely unprotected. Your next policy should explicitly include prior acts coverage to close this gap and maintain protection across your entire project history. Understanding these coverage mechanics now prevents catastrophic exposure later, and selecting the right policy limits and deductible requires a clear assessment of your actual business risks and client contract requirements.

Matching Coverage Limits to What Your Business Actually Faces

Determine Your Industry’s Real Exposure

Your industry determines how much coverage you genuinely need, and selecting the wrong limits costs you money either way. If you choose limits too low, a single claim exhausts your policy and leaves you personally liable for the remainder. If you choose limits too high, you overpay for protection you’ll never use. Most California businesses select $1 million per-claim and $1 million aggregate limits, according to Insureon data, which works for many service providers but not all.

Building designers face higher exposure from design defects and costly rework, so they should consider $2 million per-claim limits because a single project error can easily exceed $1 million in remediation costs. Real estate agents handling commercial transactions should match their limits to the typical transaction values they work with-a $5 million commercial deal demands higher limits than a $500,000 residential sale. Accountants and tax consultants face lower individual claim severity but higher frequency of smaller errors, making $1 million limits often adequate. Technology consultants who handle data security should pair their professional liability with cyber coverage because a data breach claim can spike costs dramatically beyond typical service errors.

Balance Your Deductible Against Your Cash Flow

The deductible you choose shapes your premium directly. Raising your deductible from $1,000 to $2,500 typically reduces your monthly cost, but only if you can actually absorb that $2,500 out of pocket when a claim arrives. Insureon data shows the average California professional liability deductible sits at $2,500, which suggests most businesses can manage that threshold. Your cash flow situation and risk tolerance should drive this decision-a higher deductible saves money upfront but requires financial reserves to cover it when claims hit.

Account for Claims History and Business Size

Your claims history and business size directly influence what you’ll pay, which means shopping multiple carriers makes a real difference in your final cost. A designer with zero claims history pays dramatically less than one with prior claims on record, and a five-person firm pays less than a fifty-person firm offering identical services. Location matters too-California coastal areas and major metro regions see higher premiums than inland or rural areas due to higher litigation costs and jury awards.

Secure Prior Acts Coverage During Transitions

When you transition between carriers, insist on prior acts coverage in your new policy because a gap in protection leaves your entire project history exposed to claims. This coverage protects work you performed before switching insurers, which matters significantly when old projects generate claims years later. Your new policy should explicitly include prior acts language to maintain continuous protection across your entire business history.

Shop Multiple Carriers for Competitive Pricing

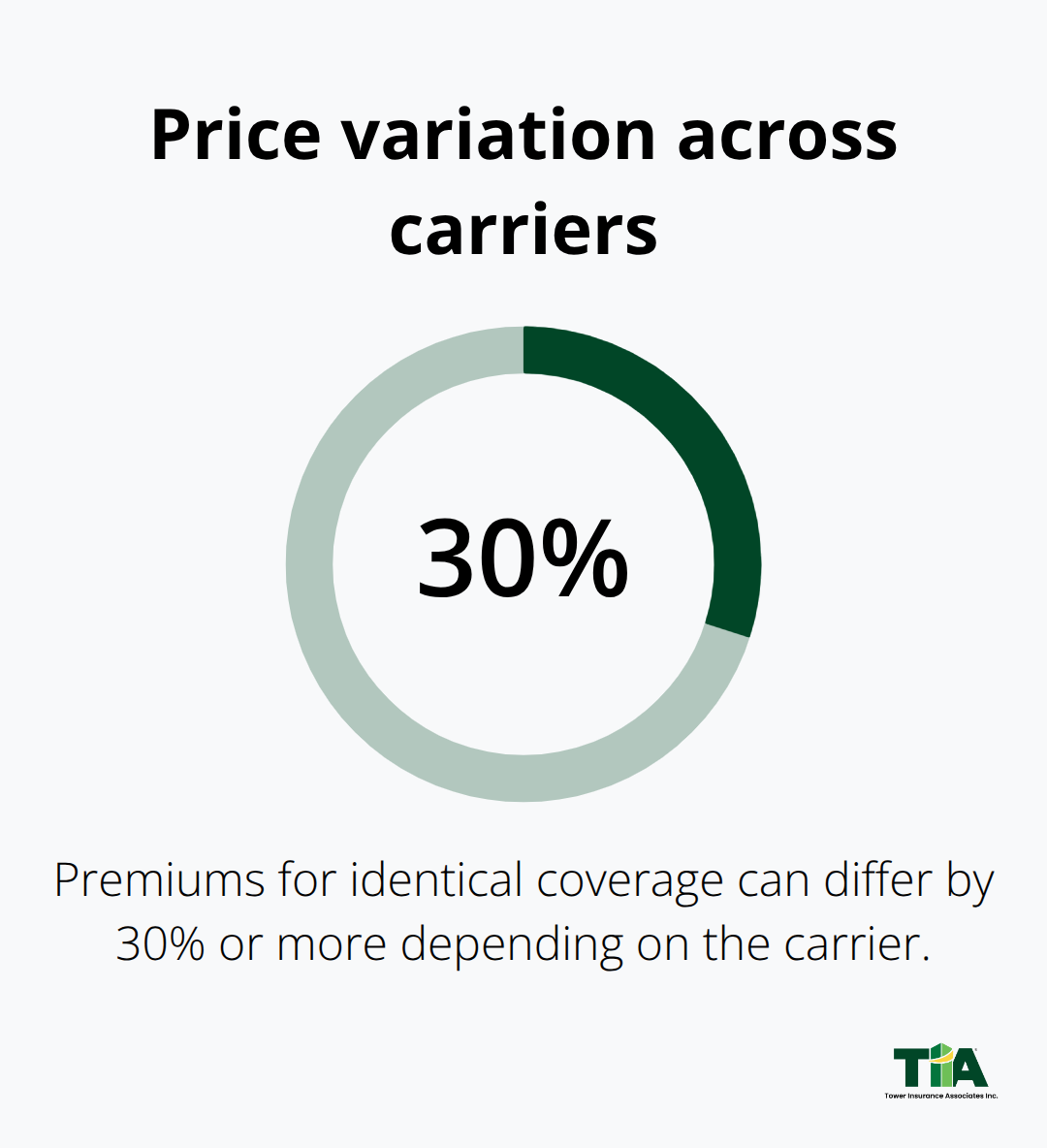

Comparing quotes from at least two or three carriers reveals how much variation exists in the market-premiums for matching coverage limits to what your business actually faces can differ by 30 percent or more depending on how each insurer assesses your risk profile. An independent agent who represents multiple carriers can access pricing you won’t find shopping online alone, and they understand California’s specific regulatory landscape and which insurers actually pay claims promptly when disputes arise. We at Tower Insurance Associates, Inc., an independent agency in Culver City representing multiple top-rated carriers, work to find competitive quotes tailored to your specific industry, claims history, and coverage needs.

Final Thoughts

Professional liability insurance protects your California business when clients allege you made mistakes, gave bad advice, or failed to deliver results. Defense costs alone can reach $50,000 to $200,000 before trial, and without coverage, you absorb these expenses personally. California professional liability insurance costs far less than a single lawsuit, with most businesses paying between $400 and $7,000 annually depending on industry and coverage limits.

Start by reviewing your largest client contracts to identify required coverage limits and specific policy language they demand. Document your service agreements clearly and assess your actual risk exposure based on the work you perform and the clients you serve. If you handle sensitive data or provide technology services, add cyber coverage to your professional liability policy because data breach claims can spike costs dramatically. When you switch carriers, insist on prior acts coverage in your new policy to protect work performed before the transition, and gaps in coverage leave your entire project history exposed to claims.

Shopping multiple carriers reveals significant price variation-premiums for identical coverage can differ by 30 percent or more depending on how each insurer assesses your risk. Contact Tower Insurance Associates, Inc. today to discuss your coverage needs and secure the protection your California business requires.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.