Directors and officers in California face unique insurance challenges that most standard business policies simply don’t address. A California D&O policy protects your leadership team from personal liability claims, legal defense costs, and employment-related lawsuits that could otherwise drain company resources.

At Tower Insurance Associates, Inc., we’ve seen too many California firms operate with coverage gaps that leave them exposed to significant financial risk. This guide walks you through what your D&O policy should cover, where California’s regulatory environment creates special considerations, and which protection gaps could hurt your business.

What Your D&O Policy Actually Covers

Directors and officers in California need to understand exactly what their D&O policy pays for when a claim lands. The policy covers three distinct areas: personal liability protection for individual directors and officers when the company cannot indemnify them, legal defense costs in securities litigation, and employment-related claims that stem from governance decisions. These three components work together to shield both personal assets and company finances.

A basic D&O policy typically covers $5–$10 million in limits, though extended coverage can push limits to $10–$25 million with fewer exclusions. The cost generally ranges from 0.5% to 3% of revenue depending on company size, industry, and claims history. In California, where 428 federal securities class action filings occurred in 2024 with median settlements above $13.5 million according to Emergen Research, adequate limits become non-negotiable. The insurer typically defends the claim and pays legal defense costs upfront, though most policies require consent before settlement becomes binding. A hammer clause may penalize you if you refuse a reasonable settlement offer, so understanding this mechanism before a claim arrives prevents costly surprises.

Defense Costs in Regulatory Investigations

California regulators intensified enforcement in 2024 with 47 SEC enforcement actions targeting sustainability disclosures, and your D&O policy should explicitly cover defense costs in these investigations. Many directors assume their policy covers regulatory defense, but gaps appear when the language remains vague about what constitutes a covered wrongful act. Courts in California have held that advancement of defense costs applies to potentially covered claims, not just conclusively covered ones, as demonstrated in the AmTrust v. 180 Life Sciences case. This means the insurer must advance your legal fees even when the ultimate coverage question remains unclear.

Subpoenas from government agencies frequently trigger disputes over coverage, particularly in merger contexts where a change-of-control exclusion might apply. The burden falls on the insurer to prove with conclusive evidence that wrongful acts occurred after a triggering event; document requests alone do not satisfy this standard. You should audit your policy language to confirm that defense cost advancement applies broadly and that change-of-control exclusions are narrowly written. Regulatory defense costs can spiral quickly, and a $1 million deductible becomes painful when you defend against an SEC investigation into ESG disclosures or data security practices.

Employment and Governance Claims

Employment practices claims frequently overlap with D&O coverage in California, where the state’s labor code creates heightened exposure. Claims arising from wrongful termination, discrimination, harassment, or retaliation decisions made by the board or officers fall within D&O coverage alongside dedicated Employment Practices Liability Insurance. California courts recognize that governance decisions often trigger employment claims, so your D&O policy should not carve out employment-related wrongful acts.

The policy should cover claims from current and former employees alleging that board decisions harmed them, whether through compensation disputes, promotion decisions, or workplace policy enforcement. Many California firms carry both D&O and EPLI as complementary coverages, with D&O addressing governance-level employment decisions and EPLI covering day-to-day HR operations. A practical step involves mapping which employment claims your board might face and confirming that your D&O policy covers those specific scenarios. Startup boards face particular risk here because early employment decisions often lack formal documentation, making defense costs higher when disputes arise.

Coverage Limits and Policy Structure

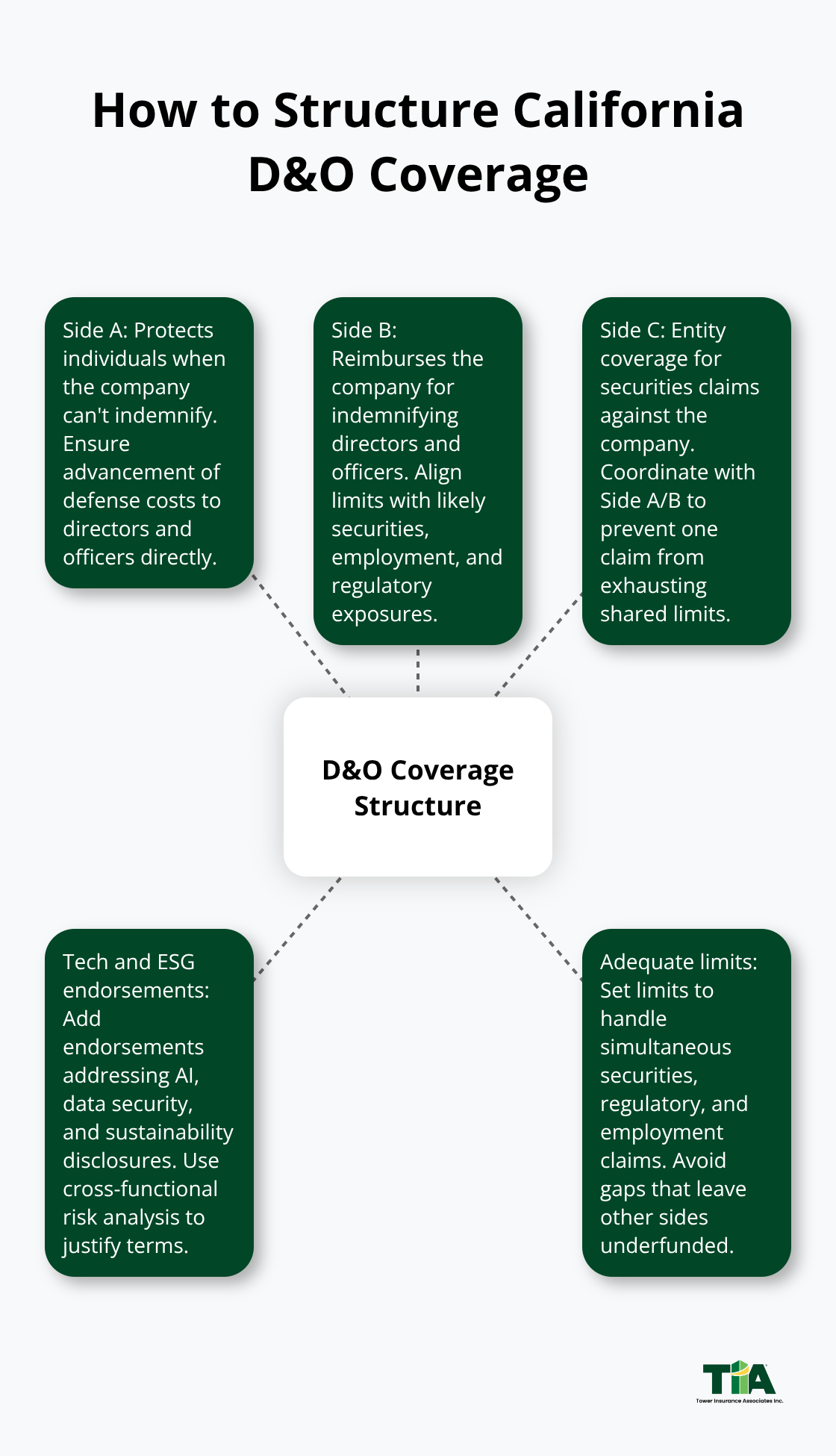

Your choice of coverage limits directly affects how well your policy responds when multiple claims hit simultaneously. Extended D&O policies (offering $10–$25 million in limits) typically include fewer exclusions and broader coverage for technology and ESG-related claims than basic policies. The three-part structure of D&O insurance-Side A (personal coverage when indemnification is unavailable), Side B (company reimbursement for indemnifying directors and officers), and Side C (entity coverage)-means you must align each component with your governance model and risk profile to avoid gaps.

California’s regulatory landscape and litigation environment make this alignment critical. A company facing potential securities claims, regulatory investigations, and employment disputes simultaneously needs sufficient limits across all three sides to prevent one claim from exhausting coverage available for others. Your policy should explicitly address technology and AI exposure, with risk analysis from your technology and legal teams used to justify tech-related endorsements on the D&O policy.

This foundation prepares you to address the specific coverage gaps that plague many California businesses.

California’s Regulatory Pressure Changes What Your D&O Policy Must Do

California’s regulatory environment has shifted dramatically, and your D&O policy structure must reflect this reality. The SEC launched enforcement actions targeting sustainability disclosures in 2024, and California’s Department of Insurance oversees a market where firms spent more than $3.1 billion on insurance in 2021, indicating how seriously the state takes governance and compliance. Your D&O policy should explicitly address regulatory defense costs because ESG enforcement actions now trigger substantial legal bills before any settlement appears. Many California firms still carry policies with vague language around what constitutes a covered wrongful act during regulatory investigations, leaving them vulnerable when the SEC or state regulators issue subpoenas. The burden to prove that a wrongful act falls outside coverage rests with the insurer, not you, but only if your policy language is precise enough to support that argument.

Extended D&O coverage that runs $10–$25 million in limits typically includes explicit regulatory defense provisions, whereas basic $5–$10 million policies often leave gaps when sustainability claims or data security investigations begin. California Labor Code sections 2800–2806 impose fiduciary duties on officers that go beyond federal securities law, meaning employment-related wrongful acts carry distinct legal exposure. Your policy must cover claims arising from board decisions around compensation, promotion, or workplace policies under California’s strict employment standards, not just federal Title VII or ADA claims. A practical step involves having your legal counsel review your current policy language against the specific Labor Code provisions that apply to your industry and governance structure.

Side A Coverage Protects Individual Directors When the Company Cannot Indemnify

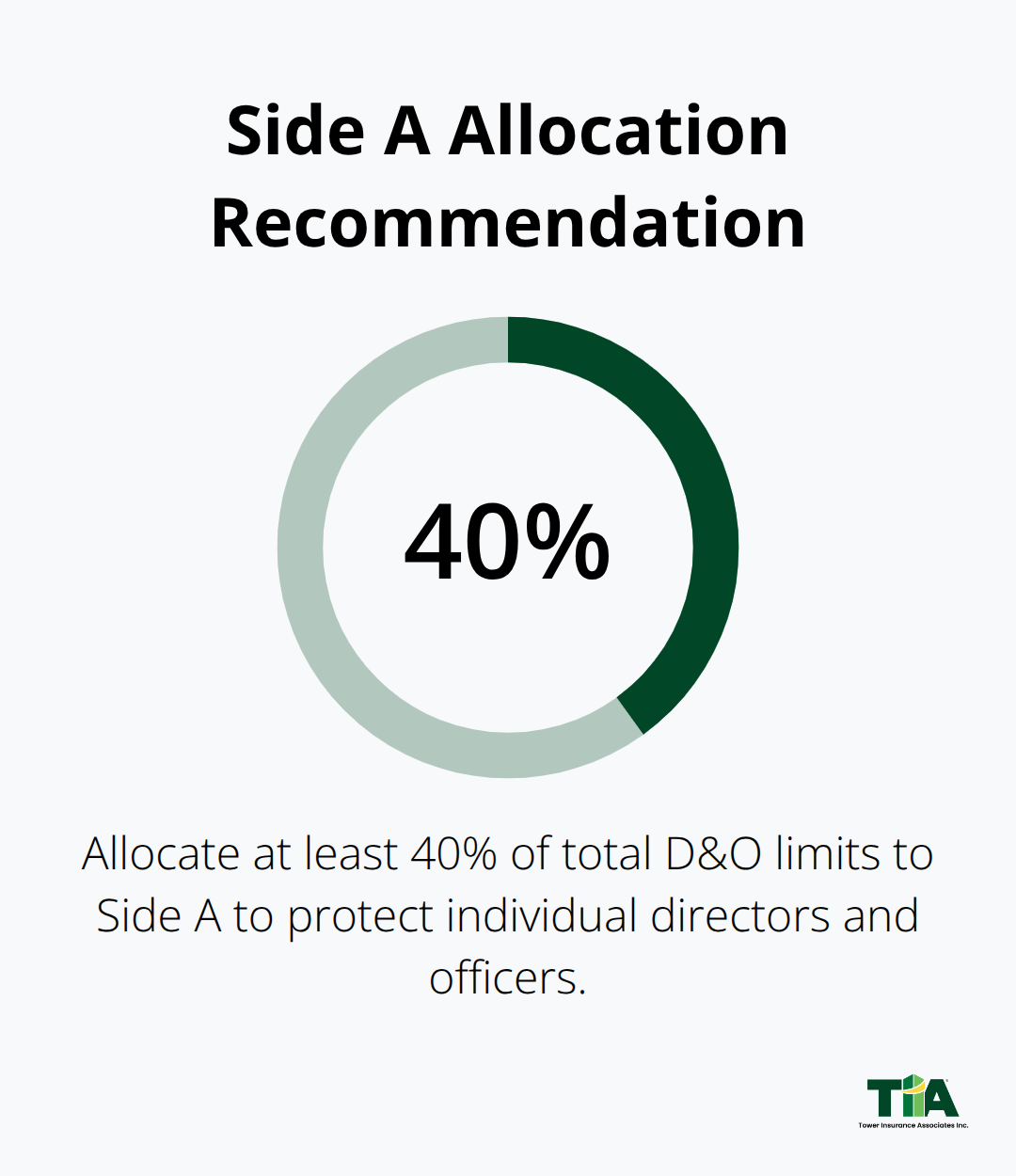

Side A coverage protects individual directors and officers when the company lacks funds to indemnify them or chooses not to, and this protection becomes essential in California’s litigious environment. The 2024 federal securities market recorded 428 class action filings with median settlements exceeding $13.5 million according to Emergen Research, meaning a single claim can exhaust company resources and leave directors personally exposed. Side A coverage advances defense costs directly to the individual director or officer, bypassing the company entirely, which matters when the company faces insolvency or when indemnification would violate state law.

California courts have held that advancement of defense costs applies to potentially covered claims rather than only conclusively covered ones, as shown in the AmTrust v. 180 Life Sciences case in federal court in San Francisco. This means your insurer must pay for your defense even when coverage ultimately remains uncertain, provided the policy language supports advancement. Many California companies allocate insufficient limits to Side A relative to their exposure, creating a situation where multiple directors face claims simultaneously and coverage exhausts quickly. Allocating at least 40 percent of your total D&O limits to Side A when your board faces technology, employment, or securities exposure protects individual leaders from personal financial devastation. Defense costs in regulatory investigations can reach $1 million or more before any settlement, so adequate Side A limits prevent individual directors from facing personal bankruptcy while defending their governance decisions.

Change-of-Control Exclusions Require Careful Scrutiny During Transactions

Change-of-control exclusions in D&O policies frequently create coverage gaps during mergers, and California courts impose a high evidentiary burden on insurers to invoke these exclusions. When your company undergoes a merger or acquisition, the insurer cannot simply deny coverage for post-closing claims based on a change-of-control exclusion without proving with conclusive evidence that wrongful acts occurred after the transaction closed. The AmTrust case established that document requests and subpoenas from government agencies do not constitute conclusive evidence of post-closing wrongful acts, so an insurer seeking to deny coverage must produce substantive proof of timing.

Your insurance broker should conduct a detailed policy review before any transaction closes, specifically examining how change-of-control language interacts with regulatory investigations that may begin months or years after closing. Extended D&O policies often include carve-outs that permit coverage for pre-closing conduct even if a change-of-control exclusion applies, whereas basic policies frequently lack this flexibility. If your company anticipates a transaction, work with coverage counsel to map potential regulatory or litigation exposure and ensure your policy language supports advancement of defense costs regardless of when an investigation commences. Post-closing investigations into pre-closing conduct represent a significant exposure for California firms, and inadequate policy language can force the company to fund director and officer defense costs out of pocket while disputes with the insurer continue.

Regulatory Defense Costs Demand Explicit Policy Language

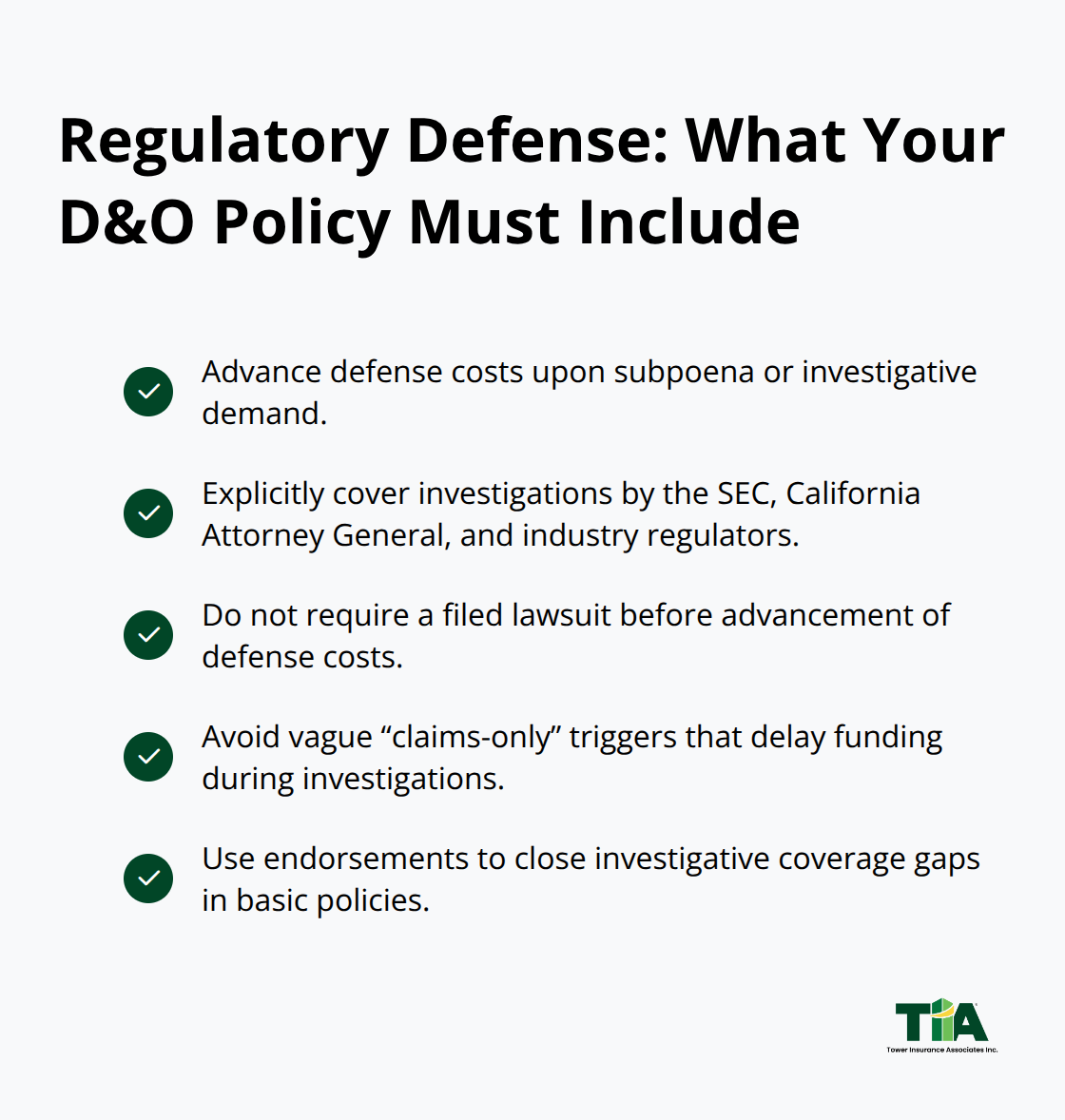

Regulatory investigations consume substantial resources before any settlement or judgment materializes, and your policy must explicitly cover these defense costs from the outset. The SEC’s enforcement actions in 2024 targeting sustainability disclosures demonstrate that regulators now scrutinize board-level decisions with intensity that rivals securities litigation. Your D&O policy should specify that defense costs advance immediately upon receipt of a regulatory subpoena or investigative demand, not after a formal complaint is filed. Vague policy language that ties advancement to “claims” rather than “investigations” creates delays that force your company or individual directors to fund defense costs upfront while coverage disputes continue. California firms facing technology-related regulatory exposure (such as AI governance or data security practices) should confirm that their policy covers defense costs in investigations by the California Attorney General, the FTC, or industry-specific regulators. This explicit coverage becomes the foundation for managing the next layer of D&O risk that California firms must address.

Where D&O Policies Fall Short for California Companies

Most California firms discover their D&O gaps only after a claim arrives, and by then the damage is done. We at Tower Insurance Associates, Inc. regularly audit policies for companies facing regulatory investigations or securities exposure, and the pattern is consistent: coverage limits lag behind actual litigation costs, exclusions eliminate protection for the exact scenarios that triggered the claim, and regulatory defense provisions remain vague enough to spark coverage disputes when the company needs certainty most. The 428 federal securities class action filings recorded in 2024 with median settlements exceeding $13.5 million according to Emergen Research mean that a basic $5–$10 million policy exhausts within weeks of a substantial claim. California firms operating with inadequate limits face a brutal choice between depleting company resources to defend against claims or forcing individual directors to fund their own defense while disputes with the insurer drag on. Growing companies compound this problem by scaling revenue and headcount without scaling D&O limits proportionally, creating a widening gap between actual exposure and policy coverage.

Coverage limits rarely keep pace with company growth

A California company generating $50 million in annual revenue typically allocates 0.5–1.5 percent of revenue to D&O premiums, translating to $250,000–$750,000 annually depending on industry and claims history. This budget constraint forces a choice between adequate limits and acceptable premiums, and most companies choose premiums. Extended D&O policies offering $10–$25 million in limits cost roughly 15–25 percent more than basic $5–$10 million policies, but the additional premium shrinks as a percentage of total cost once you move beyond entry-level coverage. A tech company with substantial data-handling exposure or a healthcare firm managing patient privacy should carry minimum limits of $15–$20 million because a single data breach claim can produce $2–$5 million in defense costs alone before settlement. The problem intensifies when a company pursues venture funding or acquisition because investors and acquirers now require proof of adequate D&O coverage, and inadequate limits create deal friction or force emergency policy upgrades at inflated premiums. Scenario planning helps here: map your industry-specific litigation exposure (securities claims for public companies, employment claims for aggressive growth-stage startups, regulatory defense for healthcare or financial services firms) and calculate the combined defense and settlement costs across multiple simultaneous claims, then allocate D&O limits accordingly. A growing company should review D&O limits annually and increase them whenever revenue crosses a meaningful threshold or when business model changes introduce new risk categories.

Prior Acts and Known Claims Exclusions Create Real Blind Spots

Prior acts exclusions eliminate coverage for any wrongful act committed before the policy inception date, and this creates a dangerous gap for companies with legacy governance issues or unresolved regulatory matters. A California firm that receives a regulatory subpoena for conduct occurring two years prior will discover that the current D&O policy excludes coverage if the exclusion language references any prior investigation or known circumstance. Extended D&O policies typically include a known circumstances waiver that carves out coverage for specific issues identified before policy inception, whereas basic policies frequently lack this flexibility. The practical implication is severe: a company with a pending SEC inquiry or shareholder derivative lawsuit must disclose this known circumstance to the insurer before policy renewal, and the insurer can then exclude coverage for that specific matter. This forces California firms to either accept a policy with broad known-circumstance exclusions or pay substantial additional premiums for coverage of disclosed matters. The solution involves working with an insurance broker experienced in California D&O to negotiate known-circumstances language before claims materialize. If your company faces any pending regulatory matter, shareholder complaint, or employment dispute, disclose it during underwriting and negotiate explicit coverage for that matter as part of the policy terms. Hiding known issues to avoid disclosure penalties almost always backfires when a claim is filed because the insurer discovers the non-disclosure and denies coverage entirely, leaving the company with no protection for the very exposure it tried to hide.

Regulatory Defense Gaps Leave Directors Paying Out of Pocket

California regulators intensified enforcement in 2024 with 47 SEC enforcement actions targeting sustainability disclosures according to the SEC Division of Enforcement, and most D&O policies carry inadequate language around regulatory defense costs. Many policies tie defense cost advancement to formal complaints or lawsuits, leaving a dangerous gap when the SEC or California Attorney General issues a subpoena during the investigative phase. A regulatory investigation can consume $500,000–$1.5 million in defense costs before any complaint is filed, and if your policy language requires a formal claim before advancement begins, the company or individual directors must fund defense costs upfront. Extended D&O policies explicitly cover defense costs in regulatory investigations, whereas basic policies frequently carve out investigative costs or require the company to prove that an investigation will likely result in a covered claim. This distinction matters enormously because regulatory investigations into technology practices, data security, or ESG disclosures now represent a primary D&O exposure for California firms.

Your policy should specify that defense costs advance immediately upon receipt of a subpoena, investigative demand, or regulatory inquiry, not after a formal complaint is filed. Many California firms carry policies with language stating that the insurer covers defense costs for claims, but claims typically means lawsuits, not investigations. Review your current policy to confirm that regulatory defense costs are covered from the moment an investigation begins, and if your policy contains gaps, negotiate an explicit regulatory defense endorsement that covers investigations by the SEC, California Attorney General, or industry-specific regulators.

Final Thoughts

California D&O policy selection requires a clear-eyed assessment of your actual litigation and regulatory exposure, not a generic approach that works for every business. The 428 federal securities class action filings in 2024 with median settlements exceeding $13.5 million demonstrate that inadequate coverage limits force California firms to choose between depleting company resources or leaving individual directors personally exposed. Your policy must explicitly cover regulatory defense costs from the moment an investigation begins, address technology and AI-related exposures through specific endorsements, and allocate sufficient Side A limits to protect individual leaders when the company cannot indemnify them.

An insurance adviser who understands California’s specific regulatory landscape and litigation patterns transforms your D&O program from a checkbox compliance item into genuine protection. Your broker should conduct scenario planning that maps your industry-specific risks and calculates combined defense and settlement costs across multiple simultaneous claims, then recommend limits and endorsements that align with actual exposure rather than budget constraints alone. An adviser experienced in California D&O can identify gaps in your current policy, negotiate known-circumstances language before claims materialize, and ensure that change-of-control exclusions do not eliminate coverage during transactions.

Start by requesting a detailed policy review from Tower Insurance Associates, Inc., an independent insurance agency in Culver City with over 60 years of experience providing personalized service and claims advocacy across commercial coverages. Compare your current limits, exclusions, and regulatory defense provisions against the specific scenarios outlined in this guide, and contact us if your policy lacks explicit regulatory defense coverage, carries broad prior-acts exclusions, or allocates insufficient limits to Side A. California’s regulatory environment and litigation exposure will not soften, so the time to strengthen your California D&O policy is now, before the next claim arrives.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.