Your classic car is more than just transportation-it’s an investment and a passion project. Classic car insurance in California requires a different approach than standard auto policies, and getting it right protects what matters most.

At Tower Insurance Associates, Inc., we’ve helped countless vintage vehicle owners find coverage that actually fits their needs. This guide walks you through everything from qualification requirements to selecting the right policy for your prized possession.

What Makes a Car Qualify as Classic in California

California’s definition of a classic car is stricter than most people think, and it directly affects your insurance options. The state recognizes three distinct pathways to collector car status, each with specific requirements that determine what coverage you can access and what inspections you’ll face. Understanding which category your vehicle falls into is the first step toward proper insurance.

Age Requirements Set the Foundation

A vehicle must be at least 35 model-years old to automatically qualify as a collector car in California. If your car is between 25 and 34 model-years old, it can still qualify if it carries historical license plates and was manufactured after 1922. This means a 1995 vehicle cannot qualify as a classic car under California law, regardless of condition or rarity. The DMV enforces these age thresholds strictly, and your insurer will verify your vehicle’s status against state records.

Special interest vehicles, which collectors preserve as hobbyists, must remain completely unaltered from the manufacturer’s original specifications to maintain their classification. Modified vehicles, kit cars, and grey market imports cannot qualify as collector cars because they fail to meet California’s safety and emissions standards. When you apply for classic car insurance, your insurer will ask for your vehicle’s VIN and title to confirm it meets these age and authenticity requirements.

Documentation Proves Your Vehicle’s Status

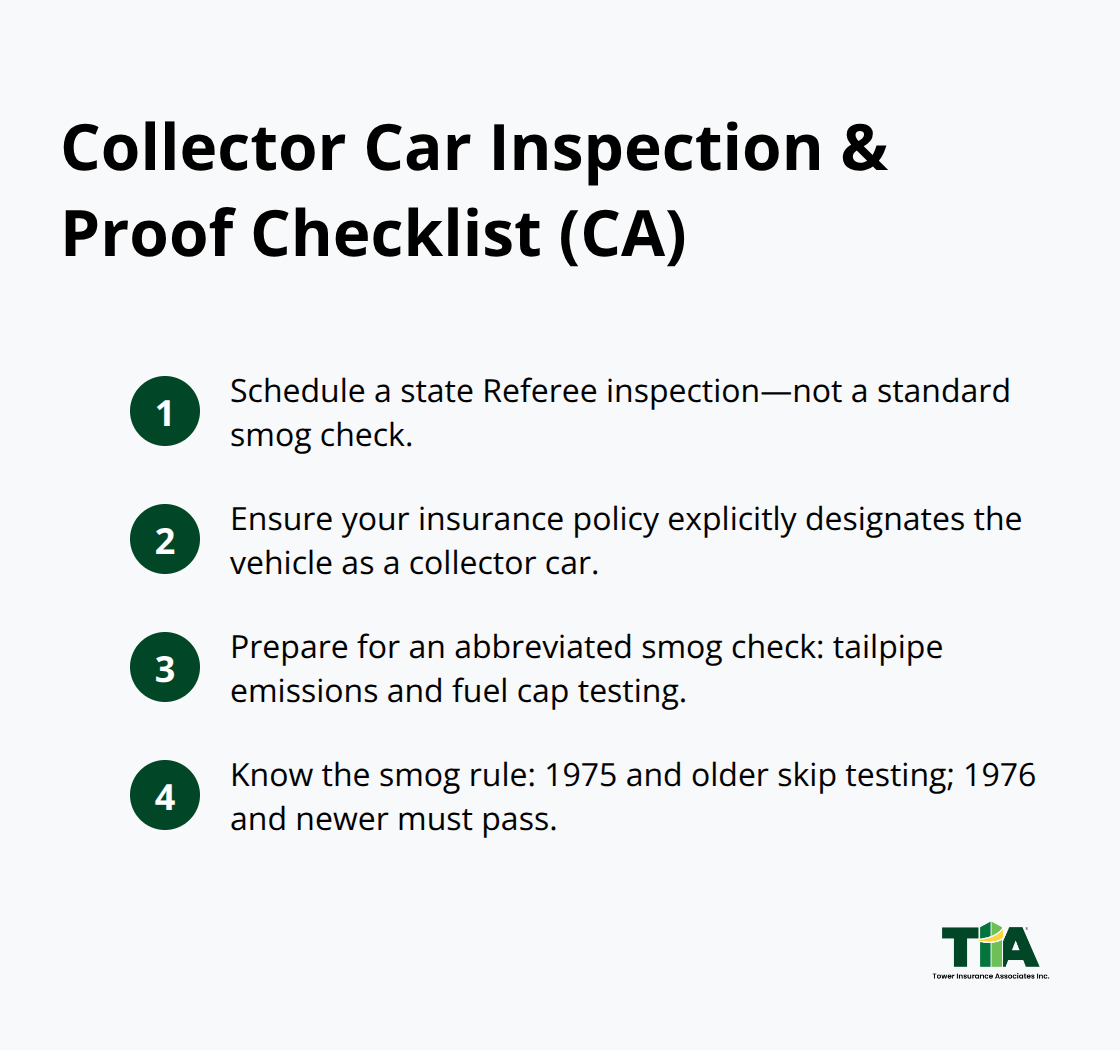

Once you establish your vehicle qualifies, you’ll need to complete a Referee inspection conducted by a state-certified inspector, not a standard smog check station. This inspection verifies your collector car status, confirms your insurance policy designates the vehicle as a collector car, and performs an abbreviated smog check that includes tailpipe emissions and fuel cap testing. Vehicles model-year 1975 and older skip the smog check entirely, but anything 1976 and newer must pass.

After passing inspection, you receive a certificate of compliance that the Referee sends electronically to the DMV, which officially registers your vehicle as a collector car in the state system. Proof of insurance as a collector car is an explicit requirement during this inspection, so you cannot schedule the Referee visit until your policy is in place and names the vehicle correctly.

Insurance Documentation Must Be Precise

Many owners underestimate how specific this documentation must be. Your insurance policy must explicitly state that the vehicle is insured as a collector car, not just be a standard auto policy covering an older vehicle. The insurer will verify this designation matches your Referee inspection paperwork.

Keep your appraisal documentation, title, and any receipts showing restoration work or maintenance (these support both your agreed value claim and your collector car status if the DMV ever questions your eligibility). Your insurer will likely request these documents when you apply, and they become critical if you file a claim. With your vehicle’s qualification status confirmed and documentation in order, you’re ready to explore the specific coverage options that protect your investment.

What Coverage Actually Protects Your Classic Car

Agreed Value Coverage Forms Your Foundation

Agreed value coverage stands as the foundation of any serious classic car policy, and it’s non-negotiable if you want protection that matches reality. Unlike standard auto policies that pay actual cash value, agreed value policies eliminate depreciation and lock in a specific amount that gets paid in full if your car is stolen or totaled. This approach eliminates the gap between what your car is worth and what an insurer decides it’s worth after a loss.

You’ll work with your insurer to establish this value through a professional appraisal or documented history. The Hagerty Price Guide and NADA Classic Car Guide provide reliable benchmarks for setting these values. Classic car values have trended upward in recent years due to collector demand and scarcity, making annual reappraisals essential as market conditions shift. Beware of stated value policies, which may pay the lesser of stated value or actual cash value-this creates serious underinsurance risk that defeats the purpose of specialty coverage.

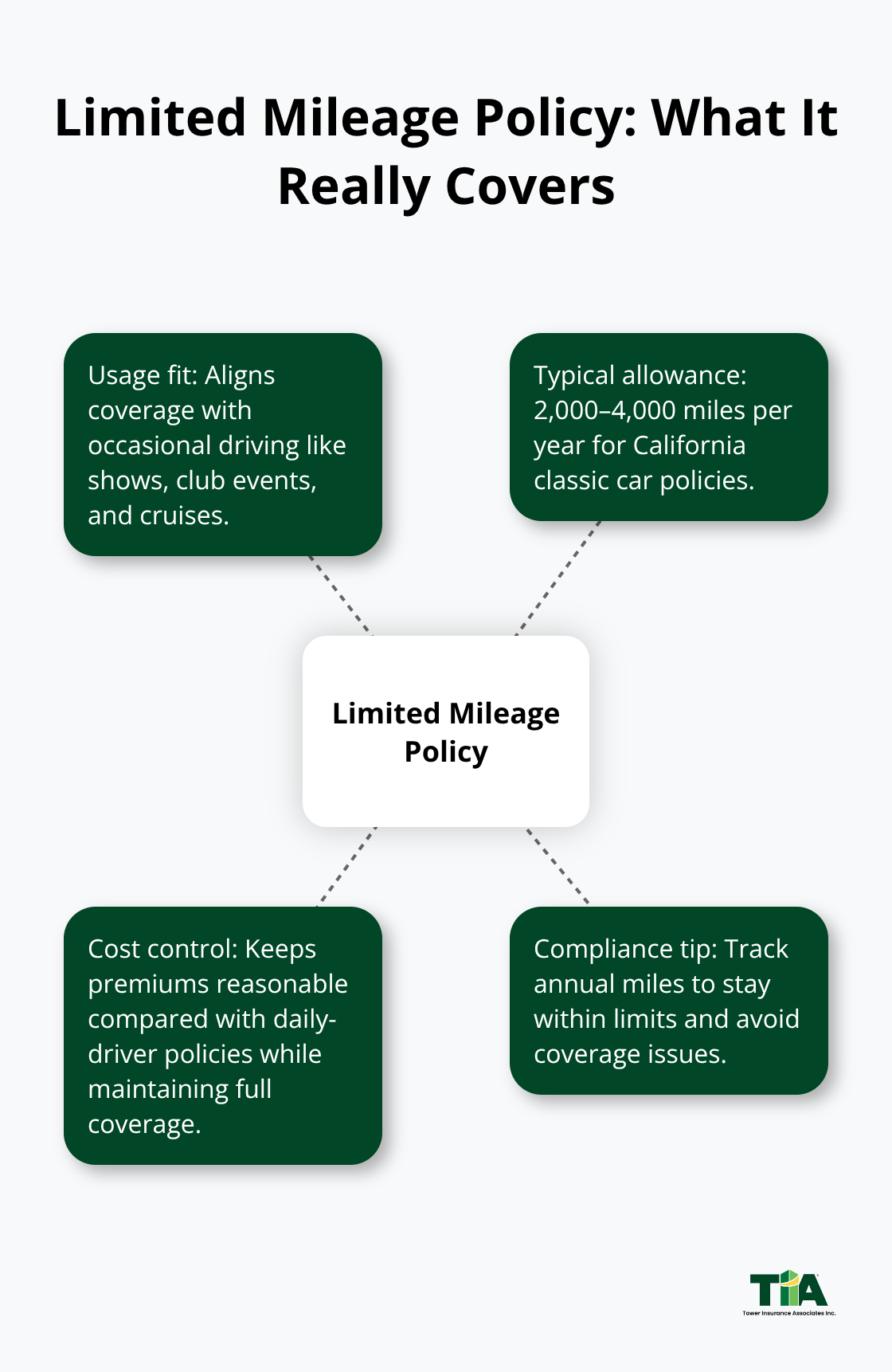

Limited Mileage Policies Match Your Actual Usage

Limited mileage policies directly address how you actually use your classic car. Most California insurers allow 2,000 to 4,000 miles annually, which covers occasional trips to shows, club events, and scenic drives without the cost of a daily-driver policy. Staying within your mileage allowance keeps premiums reasonable while maintaining full coverage when you need it.

Specialized Protection for Theft, Damage, and Transport

Specialized liability and collision protection requires both comprehensive and collision coverages that safeguard against theft, fire, weather damage, and accidents. Classic cars often contain scarce OEM parts that cost significantly more to replace than modern equivalents. Spare parts coverage reimburses costs for hard-to-find components kept specifically for your vehicle. Guaranteed flatbed towing protects your vehicle during transport to avoid damage that standard towing services might cause.

Storage and Deductible Decisions Lower Your Costs

Your storage location matters considerably; a locked, secure structure with anti-theft devices can lower your risk profile and premiums according to the Insurance Information Institute. Deductibles typically range from zero to one thousand dollars, giving you flexibility to balance premium costs against out-of-pocket expenses if a claim occurs. These choices directly affect what you pay each month while maintaining the protection your investment deserves.

With your coverage options mapped out, the next step involves determining your vehicle’s actual market value and finding the right insurer to back that valuation.

Getting Your Classic Car Valued and Insured

Professional Appraisals Establish Your True Value

Professional appraisals form the backbone of accurate agreed value coverage, and skipping this step creates serious problems later. The Hagerty Price Guide and NADA Classic Car Guide both provide market-based valuations that insurers recognize and accept, but these tools work best when combined with a documented appraisal specific to your vehicle’s condition. A car valued at $45,000 by one insurer might be valued at $52,000 by another based on their underwriting standards and market expertise. This difference directly impacts your annual costs and the payout you receive if a total loss occurs.

Compare Multiple Quotes Simultaneously

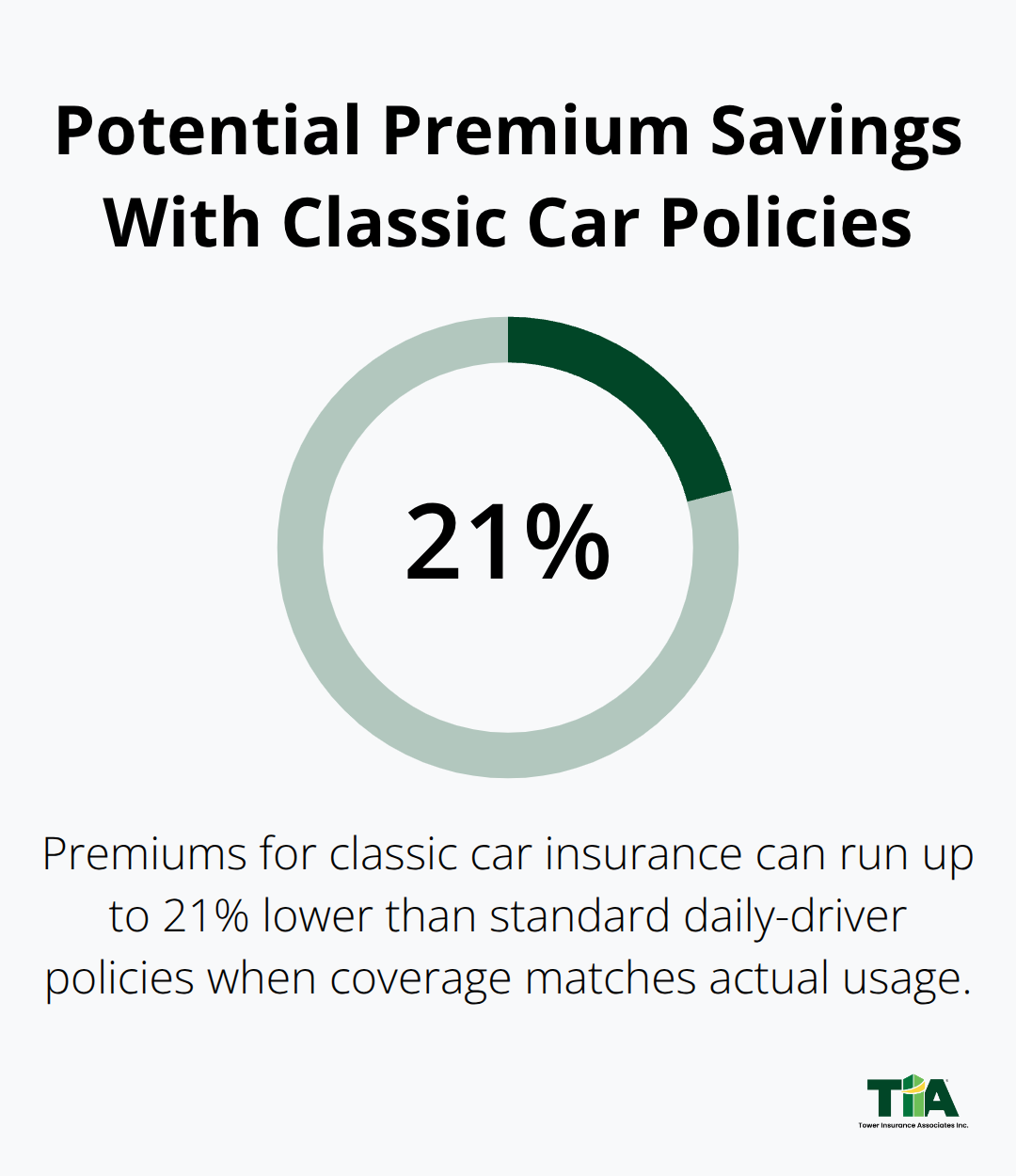

Request quotes from multiple insurers at the same time rather than sequentially-this prevents you from anchoring to the first number you hear and gives you genuine comparison data. California classic car insurers like Hagerty, Grundy, and American Collectors Insurance each approach valuation differently, so comparing their offers reveals the true range of available pricing. Hagerty reports that premiums for classic car insurance can run up to 21 percent lower than standard daily-driver policies when coverage is properly tailored to your actual usage.

When comparing quotes, isolate what changes between policies. Some carriers bundle roadside assistance and trip interruption coverage while others charge separately, making a lower base premium misleading if you need those protections. This detailed comparison takes time but protects you from selecting a policy that looks cheap until you discover missing coverage.

Verify Deductibles Match Your Financial Comfort

Deductible options typically range from zero to one thousand dollars according to the Insurance Information Institute, and your choice depends on your financial comfort with out-of-pocket expenses rather than some theoretical optimal number. A zero-dollar deductible costs more monthly but eliminates surprise expenses after a loss. A higher deductible reduces your premium but increases what you pay when a claim occurs.

Confirm Coverage Details Before You Commit

Verify that mileage allowances match your driving reality-if your policy caps you at 2,000 miles annually but you drive to shows and cruises regularly, you risk coverage denial if a loss occurs during an unapproved trip. Ask each insurer explicitly whether their policy covers show and concourse participation, as this directly affects how you can use your vehicle without triggering coverage exclusions. Request clarification on spare parts coverage limits, since hard-to-find OEM components for classic vehicles often exceed standard replacement part thresholds.

Confirm whether your insurer requires you to maintain a separate daily-driver vehicle in your name, as some California carriers impose this requirement to reduce risk. These policy details determine whether you’re actually protected when you need coverage most.

Final Thoughts

Your classic car represents years of passion and investment that standard auto policies cannot protect. Classic car insurance in California demands the specificity that ordinary coverage simply cannot provide, which is why understanding your options matters far more than hunting for the cheapest premium. Agreed value coverage eliminates depreciation risk, limited mileage policies match your actual driving habits, and specialized protections like spare parts coverage address the unique needs of vintage vehicles.

Gather your vehicle documentation and request quotes from multiple insurers to compare coverage details side by side. Ask each carrier about mileage allowances, show participation coverage, deductible options, and storage requirements, then verify that their policy explicitly designates your vehicle as a collector car. These conversations take time but protect you from selecting a policy that looks affordable until you discover missing coverage when you need it most.

At Tower Insurance Associates, Inc., we represent multiple top-rated carriers and provide the personalized service that specialty vehicles deserve. Contact us today to discuss your classic car’s specific protection needs and find tailored coverage that protects your investment while keeping your premiums competitive.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.