Your vintage car is more than just transportation-it’s a piece of history that deserves specialized protection. Standard auto insurance policies simply don’t account for the unique value and care requirements of classic vehicles in California.

At Tower Insurance Associates, Inc., we understand that a vintage car policy in California needs to reflect what your vehicle actually means to you. This guide walks you through the coverage options, requirements, and steps to properly protect your timeless investment.

What California Actually Requires for Vintage Car Coverage

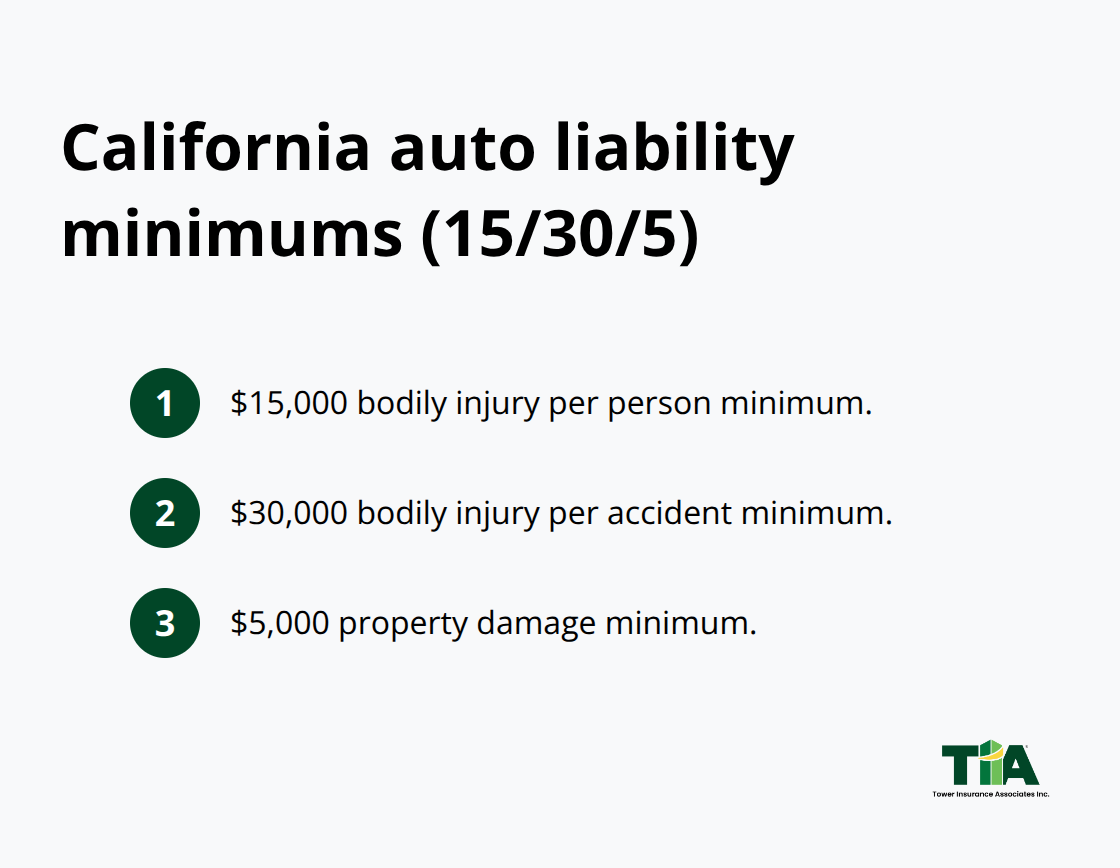

California’s Liability Baseline

California’s Department of Motor Vehicles mandates that all registered vehicles carry liability insurance, and vintage cars are no exception. You need a minimum of 15/30/5 coverage, meaning $15,000 bodily injury per person, $30,000 per accident, and $5,000 property damage.

However, this baseline covers only damage you cause to others-not your own vehicle. For a vintage car worth tens of thousands or more, standard liability alone leaves your investment dangerously exposed.

Why Actual Cash Value Fails Vintage Cars

Standard auto policies use Actual Cash Value, which depreciates your classic car based on age and market tables, often undervaluing the thousands you’ve invested in period-correct restoration work or rare components. If your 1967 Mustang suffered a total loss, an ACV policy might pay out $18,000 when you’ve spent $35,000 rebuilding the engine and interior to original specifications. This mismatch between what you’ve invested and what you receive creates a financial disaster that standard policies don’t prevent.

Agreed Value: Protection That Matches Reality

Agreed Value coverage changes this equation entirely. You and your insurer establish the vehicle’s worth upfront, and the insurance company will guarantee that they will pay this agreed-upon value in the event of a covered total loss-no depreciation, no surprises, no negotiation after a loss. This approach recognizes that vintage cars aren’t depreciating assets like daily drivers; they’re preserved investments that gain value through meticulous maintenance and authentic restoration.

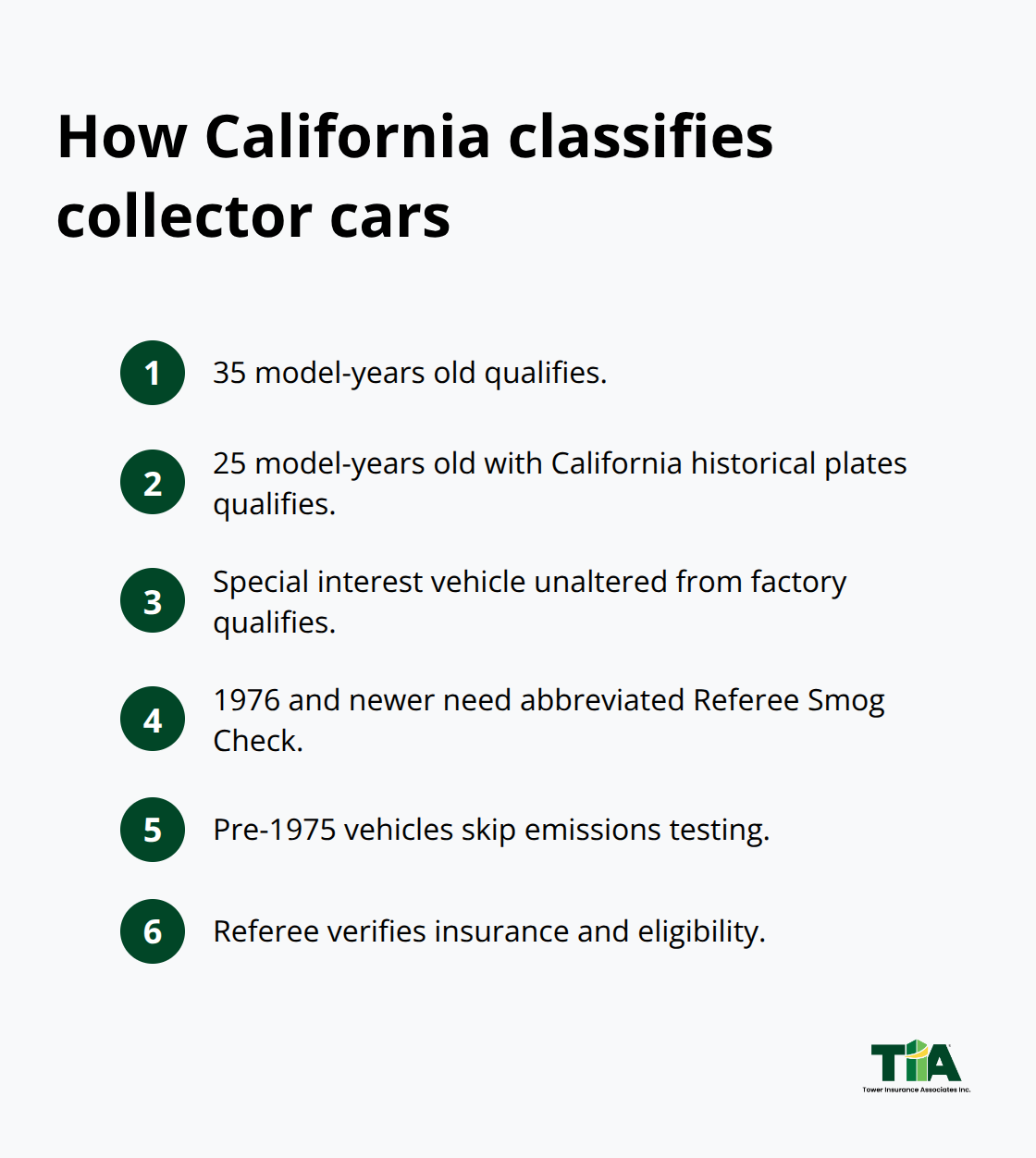

Collector Car Classification in California

Collector cars in California qualify through age or historical significance. A vehicle must be at least 35 model-years old, or 25 model-years old with California historical vehicle license plates, or qualify as a special interest vehicle that remains unaltered from factory specifications. Model-year 1976 and newer collector cars require an abbreviated Smog Check through a state Referee, while pre-1975 vehicles skip emissions testing entirely. The Referee inspection verifies your collector car insurance is in place and confirms the vehicle meets eligibility criteria.

Specialized Coverage Aligned With Your Driving

This classification provides access to specialized coverage that acknowledges your driving habits-shows, parades, weekend cruises-not daily commuting. Your coverage can grow alongside your vehicle’s value as you complete restoration milestones, and policies often account for the car community lifestyle (meets, rallies) as part of your driving profile. An independent agency approach helps you compare multiple carriers to find one that truly understands classic cars and can match your vintage car’s actual usage and restoration status to appropriate protection.

Coverage That Actually Protects Your Investment

Agreed Value: The Right Foundation for Vintage Cars

Agreed Value coverage eliminates the depreciation trap that standard Actual Cash Value policies create. With ACV, your 1972 Chevrolet Chevelle loses value every year according to market tables, regardless of the $28,000 you spent on a frame-off restoration. When a total loss occurs, you receive far less than your actual investment. Agreed Value works differently-you and your insurer establish the vehicle’s value upfront based on a professional appraisal, and that’s exactly what you receive if the car is totaled. No negotiation, no depreciation formulas, no heartbreak.

This approach makes sense because vintage cars aren’t depreciating daily drivers; they’re preserved assets that hold or gain value through authentic restoration and meticulous care. Standard policies fail to recognize this fundamental difference. Agreed Value policies acknowledge that your 1965 Ford Thunderbird represents a carefully maintained investment, not a vehicle losing value with each passing year.

Comprehensive and Collision Coverage for Your Specific Needs

Comprehensive coverage protects against theft, vandalism, weather, and animal damage-critical for cars stored in garages or displayed at shows. Collision coverage handles damage from accidents regardless of fault. For vintage cars, these coverages should align with how you actually drive and store the vehicle. If your Thunderbird stays garaged except for weekend cruises and car meets, your collision deductible can be higher (say $1,000 instead of $250) to lower premiums, since you’re not commuting in traffic.

Specialized flatbed roadside assistance matters significantly-a standard tow truck can damage original paint or suspension on a lowered classic, so policies that include flatbed recovery for backroad breakdowns protect both the car and your peace of mind. Many carriers also cover rare spare parts and components stored off the vehicle, something standard policies skip entirely.

Adjusting Coverage as Your Restoration Progresses

Your restoration milestones should trigger coverage adjustments. As you complete work on your vintage car, your coverage value can increase to match the car’s improved condition, ensuring protection grows with your investment rather than staying frozen at purchase. This dynamic approach recognizes that a frame-off restoration transforms both the vehicle’s condition and its actual value over time.

An independent agency approach helps you compare multiple carriers to find one that truly understands classic cars and can match your vintage car’s actual usage and restoration status to appropriate protection. This matters because carriers differ significantly in how they value restoration work and account for specialized storage and driving patterns.

Securing Your Vintage Car’s True Value

Start With a Professional Appraisal

A professional appraisal documents your vehicle’s actual condition and the restoration work you’ve completed before you contact an insurance company. An independent appraiser who specializes in classic cars examines everything from originality to mechanical restoration, producing a detailed report that becomes the foundation for your Agreed Value quote. Once you have that appraisal in hand, you possess the hard numbers needed to shop for accurate quotes.

Compare Carriers That Understand Collector Vehicles

Not all insurance carriers value classic cars equally. Many standard insurers treat vintage vehicles like any other used car, applying depreciation tables that ignore your authentic restoration work. An independent agency approach allows you to compare how different companies actually price your specific car. Some carriers offer better rates for pre-1975 vehicles that skip the Smog Check requirement entirely, while others provide superior coverage for restoration-in-progress situations where your car’s value is still increasing. The difference between carriers can easily amount to $200 to $400 annually on premiums, making comparison shopping genuinely worthwhile rather than settling for the first quote.

Update Your Coverage as Your Car Evolves

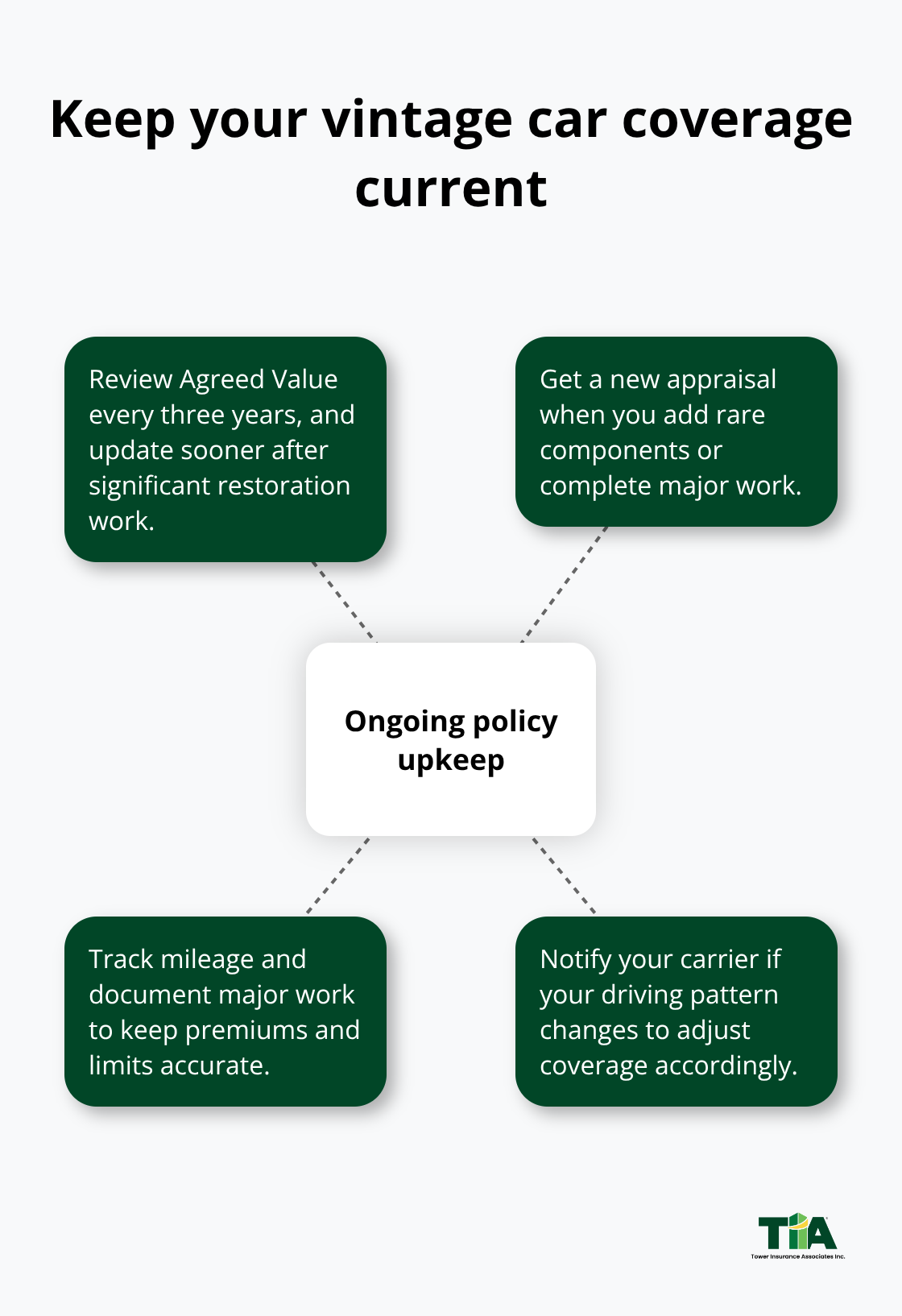

Your policy isn’t static after you sign the paperwork. California’s collector car classification requires you to keep proof of insurance current, and as your restoration progresses or your car appreciates, your coverage needs to evolve with it. Most carriers recommend reviewing your Agreed Value every three years, but if you’ve completed significant restoration work or added rare components, you should update your appraisal sooner. An outdated appraisal means you’re potentially underinsured by thousands of dollars.

Track your mileage honestly and document any major work you complete, since these details directly affect your premium and coverage limits. If you haven’t valued your car in three years and you’ve invested in authentic parts or mechanical restoration, a new appraisal might reveal your vehicle is worth significantly more than your current coverage limit.

Communicate Changes in How You Drive Your Car

Transparency about how you actually drive your vintage car matters significantly. If you’ve shifted from occasional weekend cruises to showing your car at regional events or participating in car club rallies, that changes your risk profile and may qualify you for lower rates since you’re driving even less on public roads. Conversely, if circumstances change and you start using your vintage car more frequently, you need to notify your carrier immediately to adjust your coverage accordingly.

Final Thoughts

Protecting a vintage car in California requires more than standard auto insurance because your classic vehicle represents years of restoration work and genuine investment that depreciation tables simply ignore. Agreed Value coverage, proper classification as a collector car, and specialized protection for your specific driving habits form the foundation of a vintage car policy California owners actually need. Your appraisal documents this reality, Agreed Value coverage guarantees it, and regular reviews keep your protection aligned with your car’s actual worth.

Carriers differ significantly in how they value restoration work, account for specialized storage, and price collector vehicles, which means an independent agency can compare multiple carriers on your behalf to find the one that truly understands classic cars. This comparison often reveals $200 to $400 in annual savings while securing superior coverage that matches how you drive and care for the vehicle. Whether your 1967 Mustang stays garaged except for weekend shows or your 1972 Chevelle participates in regional car club events, your coverage should reflect your actual usage and restoration status.

Your next step is straightforward: obtain a professional appraisal, document your mileage and usage honestly, and connect with an independent agent who understands collector vehicles. Visit Tower Insurance Associates, Inc. to discuss your vintage car’s protection with someone who respects automotive heritage and can match your timeless investment to appropriate coverage.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.