A cyber breach can happen to any California business, and when it does, your insurance claim needs to move fast. We at Tower Insurance Associates, Inc. know that filing a cyber claim correctly the first time prevents delays and denials.

This guide walks you through exactly what California insurers expect, what documentation matters most, and how to avoid the obstacles that slow down claim payouts.

What Counts as a Cyber Incident in California

Defining Cyber Incidents Under California Law

A cyber incident under California law spans far more than just ransomware attacks. The California Attorney General’s Cyber Exploitation Unit prosecutes cases involving unauthorized access, data theft, intimate image distribution, identity theft, and extortion via digital means. When your business files an insurance claim, insurers examine whether your incident fits their policy language, which typically covers data breaches, network intrusions, ransomware, business email compromise, and system failures caused by malware. The distinction matters because some policies exclude certain attack types or require specific actions within the first 24 to 48 hours.

Ransomware and Immediate Response Requirements

Ransomware cases demand immediate isolation of affected systems, rapid forensic assessment, and law enforcement notification to the FBI’s Internet Crime Complaint Center to maximize your claim’s credibility. Data breaches involving California residents trigger mandatory notification requirements under California’s data breach notification law, which means your insurer expects you to have already assessed scope and notified affected parties within specific timeframes. Cyber exploitation claims-including nonconsensual image distribution-fall under both criminal and civil remedies, and victims can sue for damages and attorney’s fees under AB 2643, so your coverage should explicitly address this exposure if your business handles sensitive customer data.

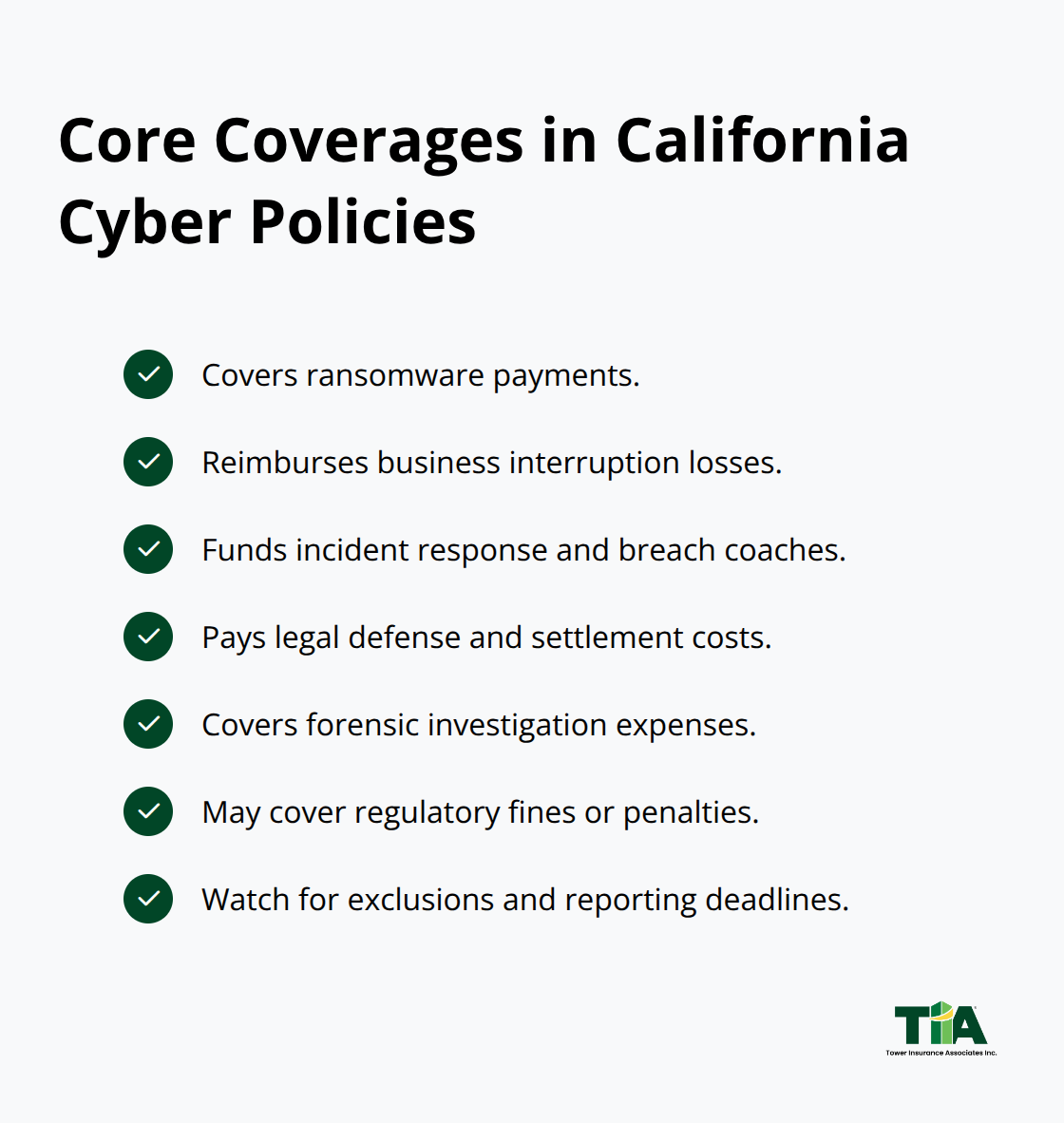

Coverage Types and Policy Scope

California cyber policies vary significantly in scope. Standard coverage includes ransomware payments, business interruption losses, incident response expenses, legal fees, forensic investigation costs, and regulatory fines or penalties in some cases. However, coverage gaps exist around claims involving alleged inadequate cybersecurity practices, late reporting past policy deadlines, misrepresentation on your application, or exclusions tied to specific ransomware strains or threat actors.

Tracking Technologies and Regulatory Exposure

The California Department of Justice’s 2025 enforcement sweep against companies like Sephora, Inc. for improper tracking and data sales shows that regulators now treat privacy violations and unauthorized data collection as cyber incidents requiring immediate remediation. If your business uses third-party software development kits, mobile apps, or tracking technologies, your cyber policy should cover regulatory fines from CCPA violations, data sales without consent, and settlements with state attorneys general. The Tilting Point settlement in 2024 resulted in a civil penalty and mandatory SDK governance programs after the company’s SpongeBob app collected personal data without proper consent. Allstate faced monetary relief under Texas enforcement for unauthorized geolocation data collection, signaling that tracking-related claims now command serious insurer and regulator attention.

Third-Party Vendor and Supply-Chain Coverage

Your policy documents should explicitly state whether third-party vendor breaches, API vulnerabilities, and supply-chain incidents trigger coverage, because many standard policies exclude or limit these scenarios. Understanding these boundaries before an incident occurs positions your business to file claims that align with what your insurer actually covers. The next section walks you through the specific documentation and evidence your insurer will request to process your claim without unnecessary delays.

How to File Your Cyber Claim Without Delays

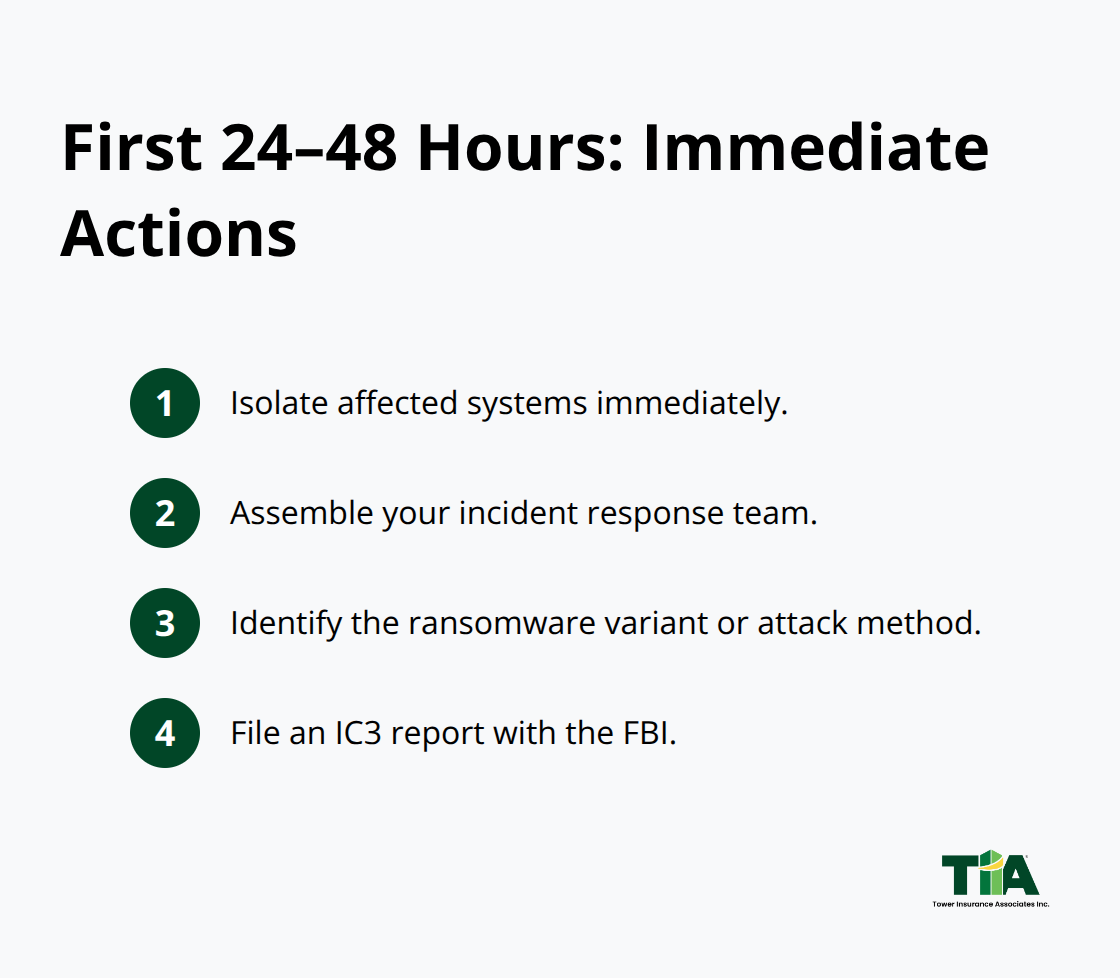

Act Fast in the First 24 to 48 Hours

The first 24 to 48 hours after a cyber incident determine whether your claim moves forward smoothly or gets tangled in documentation disputes. Isolate all affected systems immediately to prevent the breach from spreading further. Assemble your incident response team or hire external IT security professionals to assess the scope and identify the ransomware variant or attack method. Contact the FBI’s Internet Crime Complaint Center to file a report, which demonstrates due diligence to your insurer and creates an official record that strengthens your claim credibility.

Notify Your Insurer Without Delay

Call your insurance provider within hours, not days. NexGen policyholders should dial 833-45-EVOLVE or email mh-evolveincident@mcdonaldhopkins.com to open the claim officially and confirm your policy’s notice deadlines. Many insurers impose strict reporting windows, and missing that deadline gives them grounds to deny coverage entirely, so treat this phone call as non-negotiable. Simultaneously, review whether your incident involves California residents’ personal data, because if it does, you must comply with California’s data breach notification law and notify affected parties within specific timeframes. Your insurer expects this documentation to already be underway, and delays here create red flags that suggest inadequate incident response.

Build a Comprehensive Documentation Package

Documentation separates fast approvals from months-long disputes. Preserve everything: the ransom note, screenshots of the attack, system logs, forensic reports from your IT security firm, timelines of when the breach occurred and when systems were isolated, emails between your team and external responders, and any communications with the attacker. Create a comprehensive claim package that includes forensic findings, your recovery steps, invoices from cybersecurity experts, calculations of business interruption losses with supporting financial records, and internal communications showing how you managed the incident. Adjusters scrutinize claims for reasons to limit coverage, so precision matters more than volume-vague loss calculations or incomplete timelines give them ammunition to reduce your payout.

Address Tracking and Regulatory Violations

If your incident involves tracking technology violations or CCPA breaches, include documentation of which third-party SDKs or data collection methods triggered the incident, because regulators now treat these violations as cyber incidents requiring immediate remediation. The 2024 Tilting Point settlement resulted in a $500,000 civil penalty after the company failed to govern third-party SDKs collecting personal data without consent. Your claim needs to show you understand this regulatory landscape and took corrective action promptly.

Engage Legal Support and Negotiate Strategically

Consider hiring a cyber insurance attorney early-not after a denial-to help structure your claim and protect your rights during negotiations. Avoid accepting rushed settlement offers that undervalue your losses; adjusters often present initial offers as final, but they rarely are. Your attorney can challenge low offers and preserve litigation options if the insurer refuses fair compensation. The claims process through Evolve Cyber Insurance Services LLC is supported by McDonald Hopkins, a law firm partner, so expect formal incident response involvement that requires detailed, organized documentation from day one. With your claim filed, documented, and supported by legal counsel, you now face the reality that some insurers still dispute coverage or delay payouts-and knowing how to navigate those obstacles determines whether you recover fully or accept a reduced settlement.

Why Insurers Deny or Delay Cyber Claims

Inadequate Security Controls as a Denial Tactic

Insurers frequently dispute coverage by claiming your business failed to maintain adequate cybersecurity controls before the breach occurred. This argument appears in denial letters constantly, and it sticks because most policies include vague language about expected security standards without defining what adequate actually means. The reality is that adjusters use this tactic to shrink payouts, and you need specific documentation proving your security posture was reasonable for your business size and industry. If your company had multi-factor authentication, regular security updates, employee training, and incident response procedures documented before the breach, you have a defense. Collect screenshots of your security configurations, employee training records with dates, and any third-party security assessments completed in the 12 months before the incident.

Late reporting past your policy’s notice deadline gives insurers legitimate grounds to deny coverage entirely, so calling within hours matters more than perfect documentation. The 2024 Tilting Point case shows how misconfigurations in third-party SDKs triggered a $500,000 penalty, and if your incident stems from vendor negligence rather than your own security failures, your claim language must distinguish between the two. Adjusters also scrutinize whether you misrepresented your security practices on your initial application, so review what you told your insurance broker about your systems, data encryption, and incident response capabilities. If reality diverged significantly from your application, expect coverage disputes. Documentation of your actual practices before the incident protects you here.

Documentation Gaps That Trigger Claim Reductions

Insufficient documentation creates the second major obstacle, and it’s entirely preventable. Adjusters need forensic reports that identify the exact attack vector, timeline of discovery, scope of affected systems, and data compromised-vague statements that you suffered a breach without specifics give them room to deny or reduce your claim. Hire a certified forensic firm immediately after isolation, not weeks later, because the quality of early investigation determines claim outcomes. Business interruption losses require granular financial records showing revenue decline during downtime, not estimates, and you need detailed invoices from every vendor involved in recovery.

If you paid a ransom, document the attacker’s communications, the amount demanded versus paid, and your reasoning for the decision, because some policies exclude ransom payments entirely while others cover them. Regulatory fines from CCPA violations or data breach notification failures need documentation showing exactly which violations triggered penalties and what corrective actions you implemented afterward. The California Attorney General’s enforcement actions against Sephora, Inc. for improper third-party tracking resulted in detailed findings about specific data categories and SDKs involved, so your documentation must match that level of specificity. Create a timeline spreadsheet with dates of discovery, notification, system isolation, forensic engagement, law enforcement contact, and claim filing-adjusters use timeline gaps to suggest delayed response and inadequate incident management. Missing any single piece of documentation gives adjusters ammunition to reduce your payout by citing incomplete claim packages.

Realistic Timelines for Claim Resolution

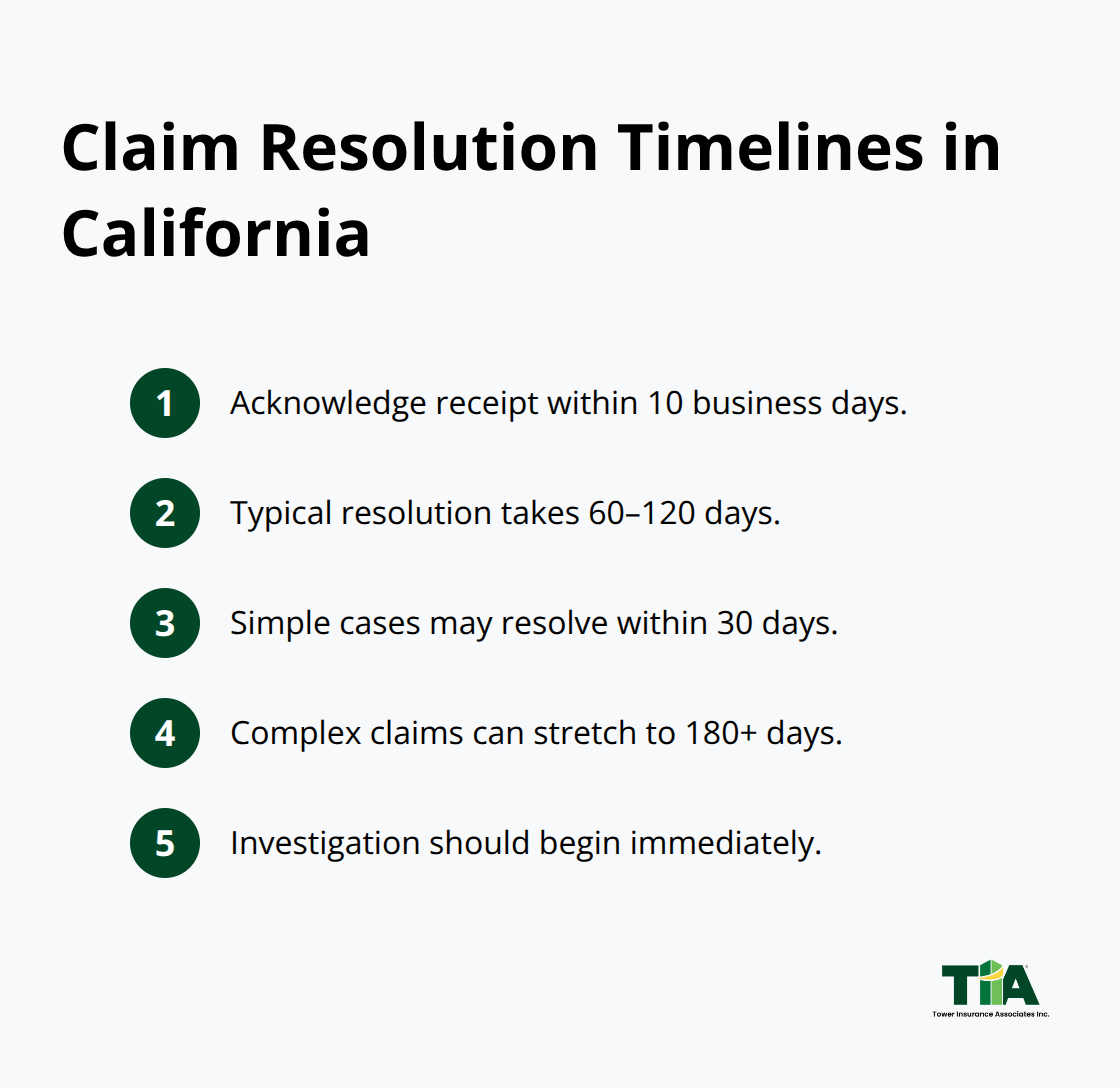

Timeline expectations vary wildly depending on claim complexity and insurer responsiveness, but most California cyber claims take 60 to 120 days from filing to settlement if documentation is complete and coverage is clear. Simple breach notification claims without ransomware demands or regulatory fines resolve faster, sometimes within 30 days, while claims involving law enforcement investigations, forensic disputes, or coverage interpretation disagreements stretch to 180 days or longer. Your insurer must acknowledge receipt of your claim within 10 business days under California Insurance Code requirements, and they must start investigating immediately, but acknowledgment is not approval.

If your claim sits without adjuster contact for more than two weeks after filing, escalate to the claims supervisor and demand a timeline for coverage determination. Adjusters sometimes deliberately slow-walk claims to pressure settlement negotiations in their favor, so proactive communication prevents this tactic. If your insurer denies coverage or offers substantially less than your documented losses, you have the right to appeal the decision and request a written explanation of the denial reasons tied to specific policy language. Hiring a cyber insurance attorney at this stage shifts leverage significantly because insurers take attorney-backed appeals more seriously than unrepresented claimant pushback. California’s unfair claims practices act prohibits insurers from delaying claims without reasonable cause, so if you face unexplained delays beyond 120 days for straightforward claims, your attorney can file a complaint with the California Department of Insurance or pursue bad-faith litigation.

Final Thoughts

Filing a California cyber claims guide successfully requires speed, documentation, and expert support. The first 24 to 48 hours after a breach determine whether your claim moves forward or gets delayed by months of disputes over coverage and documentation gaps. Call your insurer immediately, isolate affected systems, hire forensic professionals, and notify law enforcement to demonstrate due diligence.

Audit your cyber policy before an incident occurs to identify coverage gaps around ransomware payments, business interruption losses, regulatory fines, and third-party vendor breaches. Many standard policies exclude or limit scenarios that actually happen in real attacks, so understanding your coverage boundaries now prevents surprises later. Document your security controls, employee training records, and incident response procedures, because adjusters will scrutinize whether your business maintained adequate cybersecurity before the breach.

Hire a cyber insurance attorney early to shift leverage during negotiations and preserve litigation options if your insurer refuses fair compensation. We at Tower Insurance Associates, Inc. work with California businesses to build cyber liability coverage that matches your risk profile and claims experience. Contact us at insurewithtower.com to review your current coverage and close gaps before a breach tests your policy’s real-world value.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.