A data breach can cost California businesses an average of $4.45 million, according to IBM’s 2024 Cost of a Data Breach Report. Cyber liability coverage California protects your company from these financial shocks, covering everything from notification costs to legal fees and regulatory fines.

At Tower Insurance Associates, Inc., we’ve seen too many business owners underestimate their cyber exposure. The gaps in coverage are real, and they’re expensive.

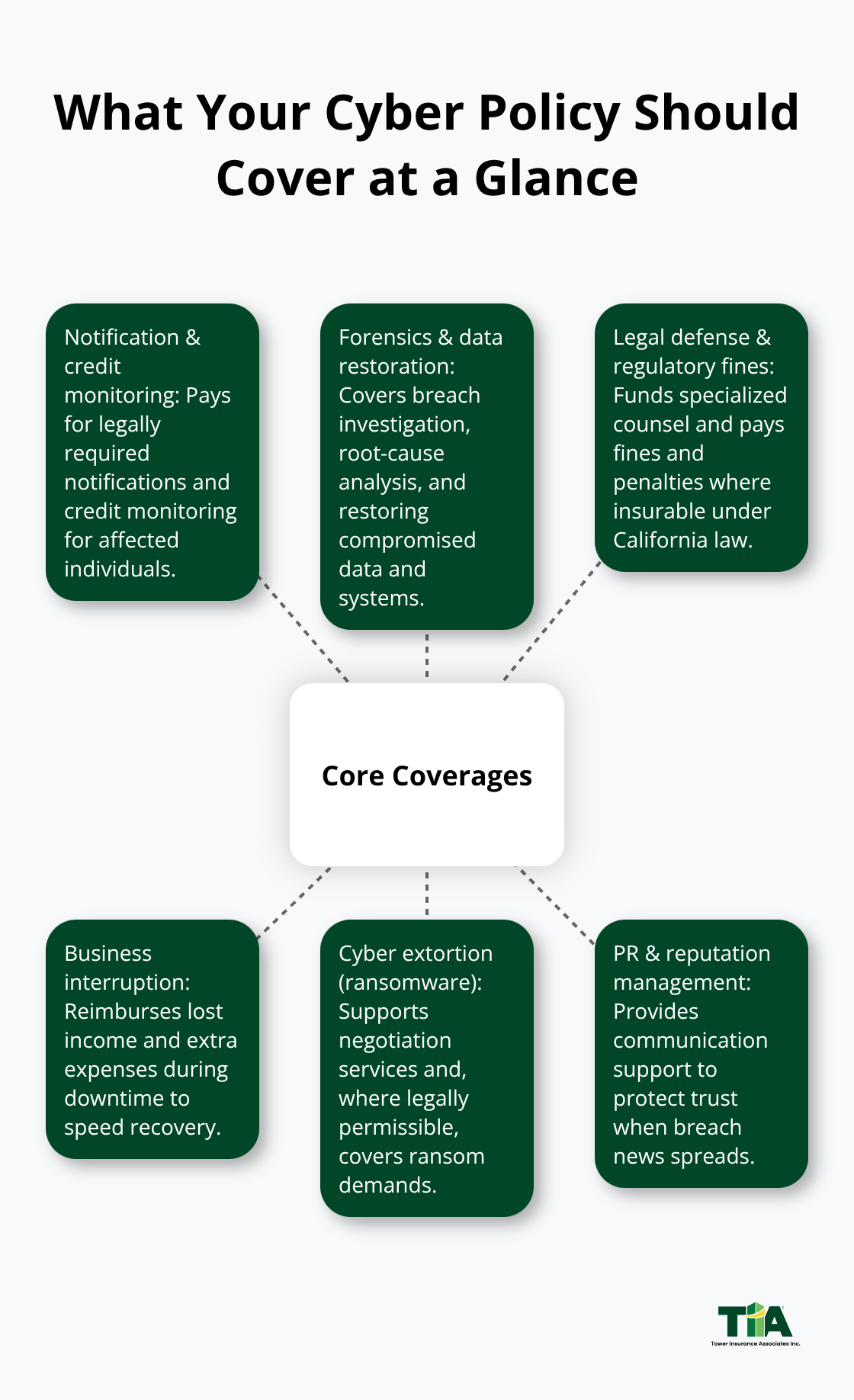

What Your Cyber Liability Policy Actually Covers

Data breach costs California businesses an average of $4.88 million, according to IBM’s 2024 Cost of a Data Breach Report. Your cyber liability policy protects against these financial shocks, covering everything from notification costs to legal fees and regulatory fines. The specifics matter far more than the marketing language.

Notification and Investigation Costs

When a breach hits, notification alone can run $2 to $4 per affected individual according to industry data. A company with 50,000 customer records faces $100,000 to $200,000 just to comply with California’s notification requirements. Your policy should cover these notification costs directly, including credit monitoring services you’re legally obligated to provide.

Forensic investigation and data restoration typically cost $10,000 to $50,000 depending on breach complexity. Cyber liability reimburses these investigation expenses, which are non-negotiable if you want to understand what happened and prevent it again. Many policies also cover public relations and reputation management costs-a service that protects your brand when news of the breach spreads. Customer trust erodes quickly after a breach, and PR support helps you communicate transparently and recover faster.

Legal Defense and Regulatory Penalties

California’s privacy laws create financial liability beyond the breach itself. The California Consumer Privacy Act imposes fines up to $7,500 per violation, and the California Privacy Protection Agency enforces these penalties. A single large-scale breach can trigger hundreds or thousands of violations, turning a $200,000 incident into a multimillion-dollar regulatory problem.

Cyber liability policies with regulatory defense coverage pay for legal representation during investigations and cover fines and penalties imposed by the state. Defending yourself against a privacy regulator requires specialized counsel, and legal fees alone can exceed $50,000 before any penalties are assessed. Third-party lawsuits from affected customers add another layer of cost. Under California law, consumers can sue for breaches involving unencrypted personal information if the breach results from failure to maintain reasonable security, with damages up to $750 per incident per person. Your policy should cover third-party liability claims, including settlement costs and court defense fees.

Business Interruption and Recovery

When a cyber attack shuts down your operations, you lose revenue while you spend money on incident response. Business interruption coverage reimburses lost income and extra expenses incurred during the downtime. For a mid-sized California business, even 48 hours of downtime can cost $20,000 to $100,000 depending on your revenue model.

The policy covers both your lost profits during the outage and the accelerated expenses you incur to restore operations faster-like overtime pay for IT staff or emergency contractor fees. Recovery expenses also include data restoration and system remediation beyond basic forensics, ensuring you resume normal operations without lingering vulnerabilities. Ransomware incidents create a specific recovery challenge: attackers encrypt your data and demand payment for decryption keys. Cyber extortion coverage helps pay for negotiation services and, where legally permissible, covers ransom amounts. The average ransom demand in 2022 reached $1.8 million according to industry reports, making this coverage a financial safeguard for businesses holding critical data.

These coverage components address the immediate financial impact of a breach, but gaps still exist in how many policies handle third-party exposures and evolving threats. Understanding what your current policy excludes becomes critical as your business grows and your data exposure changes.

Why Cyber Threats Have Intensified for California Businesses

Ransomware Attacks Accelerate Faster Than Most Businesses Can Respond

Ransomware attacks against California businesses have become routine, not exceptional. In 2024, around 65% of financial organizations experienced a ransomware attack, compared to 64% in 2023. Attackers now encrypt critical systems within hours of initial access, leaving businesses with minimal time to respond before operations halt completely. The financial pressure is immediate and severe. A manufacturing firm in California loses $50,000 per hour during downtime, and ransomware actors deliberately target businesses during peak revenue periods to maximize negotiation leverage. Cyber liability coverage with extortion provisions becomes non-negotiable when your business depends on continuous operations.

Human Error and System Failures Drive Most Breaches

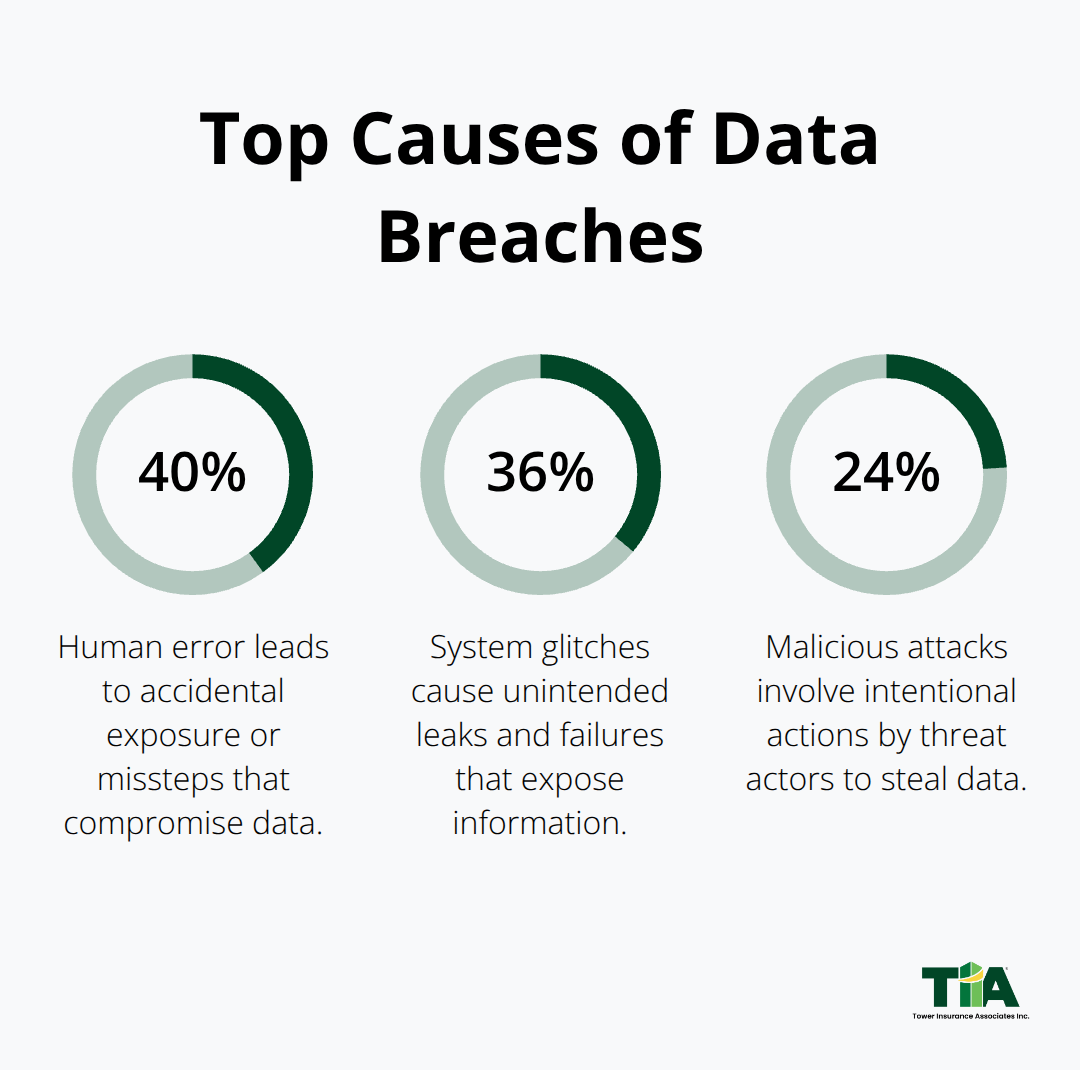

Data breaches themselves accelerate at alarming rates. About 40 percent of breaches stem from human error, 36 percent from system glitches, and only 24 percent from malicious attacks, according to industry analysis. This matters because your biggest vulnerability isn’t always an external hacker-it’s your own employees accidentally exposing customer data or your systems failing silently. The average cost per breached record sits around $194 to your business, which compounds quickly when you handle thousands of customer records.

California’s Regulatory Penalties Multiply Breach Costs

California’s regulatory environment makes cyber risk exponentially more expensive than in other states. The California Consumer Privacy Act imposes fines up to $7,500 per violation, and the California Privacy Protection Agency enforces these penalties with aggressive investigation authority. A single breach affecting 10,000 records can trigger tens of thousands of violations if your notification or response falls short of regulatory standards. Third-party lawsuits add another dimension-California law permits consumers to sue for breaches involving unencrypted personal information when businesses fail to maintain reasonable security, with statutory damages up to $750 per person per incident.

Small Businesses Face Disproportionate Targeting

Small and medium-sized businesses face particular targeting because attackers recognize they typically have weaker defenses but still hold valuable customer data. According to Accenture’s Cost of Cybercrime Study, 43 percent of all cyber attacks target small businesses, yet only 14 percent have adequate cyber defenses. This gap makes SMBs profitable targets for automated attack campaigns and ransomware-as-a-service operations. Attackers use vulnerability scanning tools to identify exposed systems, then deploy malware to establish persistence before launching their actual attack. Your IT team often notices suspicious activity only after the attacker already has administrative access.

Coverage Protects Your Business When Prevention Fails

Cyber liability coverage becomes your financial backstop when prevention fails, covering the notification costs, legal defense, regulatory fines, and incident response expenses that would otherwise devastate your cash flow. Understanding which threats pose the greatest risk to your specific business-and which coverage gaps could expose you to catastrophic losses-requires a detailed assessment of your current policies and your actual data exposure.

Common Gaps in Cyber Coverage and How to Avoid Them

Third-Party Vendors Create Hidden Liability Exposure

Your cyber liability policy covers your own breach response costs, but most policies contain a dangerous blind spot: third-party vendor exposure. When a software vendor, cloud provider, or payment processor suffers a breach, your customer data flows through their systems regardless of how strong your own defenses are. You remain liable for the breach even though you didn’t cause it. Outsourcing IT does not eliminate your risk-your business stays responsible for breaches caused by third-party vendors.

Consider a healthcare provider in California that outsources patient record storage to a cloud vendor. That vendor suffers a ransomware attack, exposing 50,000 patient records. California law still holds the healthcare provider accountable for notification, regulatory fines, and lawsuits from affected patients. Your standard cyber liability policy may not cover third-party vendor breaches unless you specifically purchased Network and Information Security Liability coverage that extends to service providers.

This coverage addresses vendor incidents, regulatory fines resulting from vendor failures, and business interruption costs when a critical vendor’s systems go down. Without it, you absorb the full financial impact of someone else’s security failures. Verify whether your current policy extends coverage to third-party service providers and whether it requires the vendor to carry their own cyber insurance. Many policies impose sublimits on vendor-related claims, meaning your coverage caps at $50,000 or $100,000 even though the actual breach costs exceed $500,000. Ask your broker specifically: does this policy cover breaches caused by my software vendors, payment processors, and cloud providers? If the answer is vague or qualified with exceptions, you need a policy amendment or a standalone vendor liability endorsement.

Incident Response Costs Exceed Notification Expenses

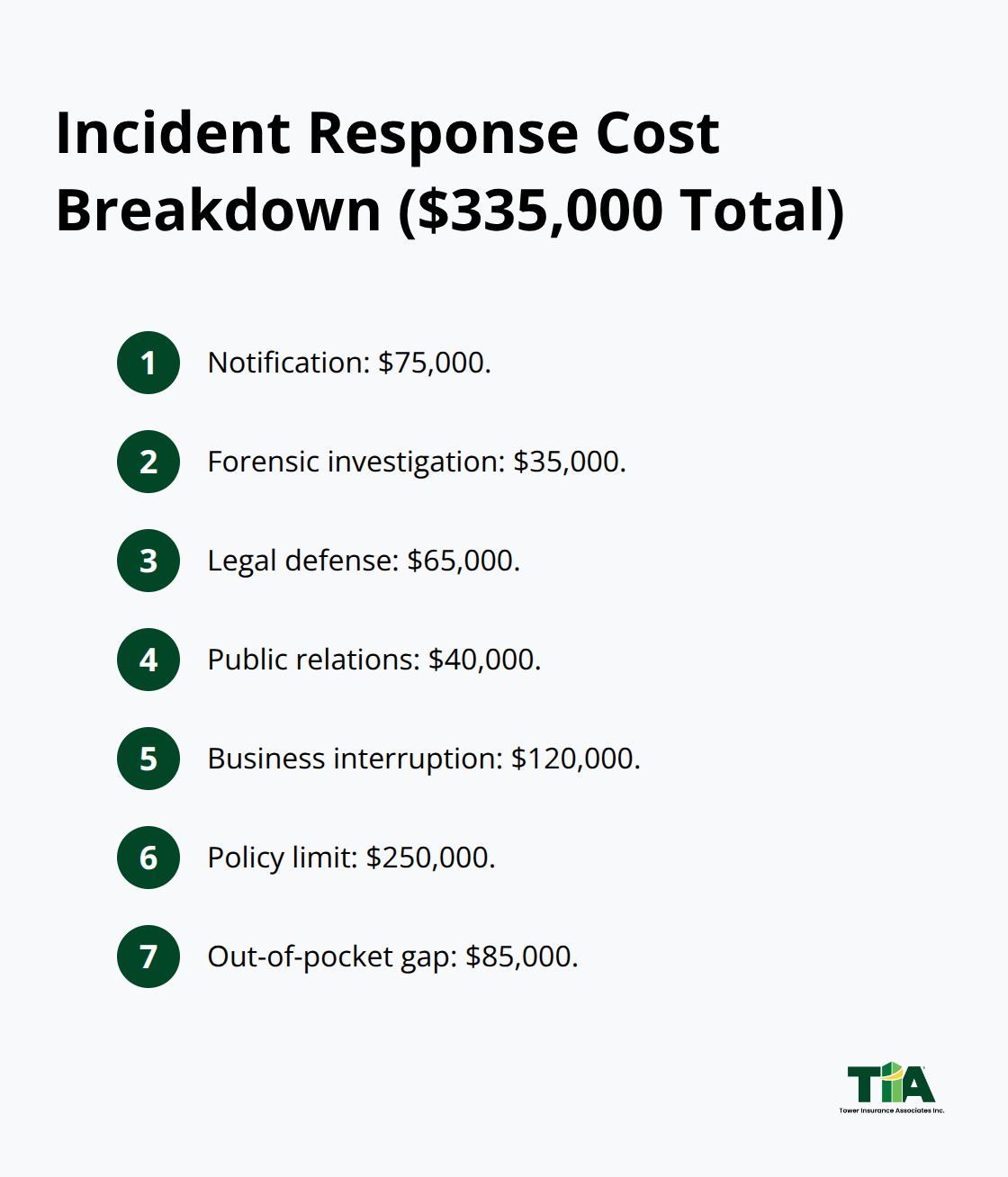

The second gap appears when businesses underestimate incident response costs beyond the obvious expenses. Notification and forensics consume money quickly, but the hidden costs accumulate during the investigation phase. A mid-sized California business faced a data breach affecting 25,000 customer records. Notification costs ran $75,000. Forensic investigation consumed $35,000. Legal defense against regulatory inquiries cost $65,000.

Public relations and reputation management added $40,000. Business interruption during the three-week response period cost $120,000. Total: $335,000.

The business’s cyber policy had a $250,000 limit, leaving an $85,000 gap the company paid from operating cash. This scenario repeats constantly because business owners focus on the headline number-notification costs-and ignore the ecosystem of expenses surrounding incident response. Your policy needs sufficient limits to cover notification, forensics, legal defense, regulatory fines, PR costs, and business interruption simultaneously, not sequentially. A $500,000 combined limit sounds substantial until a forensic firm charges $60,000, lawyers bill $80,000, notification costs $150,000, and regulatory fines reach $200,000. You’ve exhausted your limit before addressing business interruption or data restoration.

Evaluate your actual exposure: how many customer records do you maintain, what would forensics realistically cost for your systems, what regulatory fines could California impose under the CCPA, and how much revenue would you lose during a 72-hour incident response window? These questions reveal whether your current limits match your real risk.

Coverage Limits Lag Behind Business Growth

The third critical gap emerges as your business grows and your data exposure expands. A startup cyber policy covering 5,000 customer records becomes inadequate when the company scales to 500,000 customers three years later. The policy limits remain unchanged, but your breach costs have multiplied tenfold. Regulatory exposure expanded proportionally-larger datasets trigger larger potential fines under California’s privacy laws.

Many businesses never revisit their cyber coverage after the initial purchase, assuming the original policy still fits their risk profile. Schedule an annual review of your cyber liability policy, specifically examining whether your coverage limits align with your current customer data volume, revenue size, and regulatory exposure under CCPA standards. This review prevents the costly discovery that your protection has become obsolete while your business has grown.

Final Thoughts

Cyber liability coverage California protects your business from financial devastation when breaches happen, not if they happen. The coverage components we’ve outlined-notification costs, legal defense, regulatory fines, business interruption, and incident response-form a complete financial safety net that prevents a single breach from destroying your company’s cash flow and reputation. California’s regulatory environment makes this protection non-negotiable, as the California Consumer Privacy Act and California Privacy Protection Agency create financial penalties that compound breach costs exponentially.

Pull your current cyber liability policy and answer three specific questions about your protection. First, do your coverage limits match your actual data exposure, or are you underinsured relative to the customer records you maintain? Second, does your policy cover third-party vendor breaches, or are you absorbing that risk alone? Third, what exclusions exist in your current coverage that could leave you exposed when you need protection most?

We at Tower Insurance Associates help California businesses evaluate their cyber exposure and build coverage that matches their actual risk. Contact us to review your cyber liability protection and ensure your business has the financial safeguards it needs when threats materialize.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.