Your classic car isn’t just transportation-it’s an investment that deserves protection beyond standard auto insurance. At Tower Insurance Associates, Inc., we know that classic car collectors need specialized coverage tailored to their unique vehicles and driving habits.

This classic car policy guide walks you through everything you need to know about insuring your collection, from understanding what makes a policy right for your car to finding the provider that gets it.

What Qualifies as a Classic Car and Why It Matters

Classic cars typically need to be at least 25 years old, though some insurers set the bar at 20 years while others require 45 years for antique classifications. The exact threshold varies by provider, so you’ll want to verify eligibility with your insurer before purchasing a policy. What matters more than age alone is condition and rarity. A 1985 Porsche 911 in excellent shape might qualify, while a 1990 sedan in poor condition likely won’t. American Collectors Insurance, which has specialized in collector vehicles since 1976, focuses on vehicles that hold or appreciate in value rather than depreciate like daily drivers. This distinction is important because classic car insurance operates on an agreed value model, meaning you and your insurer set the car’s worth upfront based on current market conditions. If your car is a total loss, you receive that full agreed amount instead of a depreciated figure. This protects your investment in a way standard auto insurance simply cannot.

Why Standard Auto Insurance Falls Short

Standard policies assume your vehicle loses value every year, so they pay out based on depreciation at claim time. For a classic car worth $50,000 that suffers a total loss, a standard insurer might calculate a current value of $35,000 and pay you that amount. With classic car insurance and an agreed value of $50,000, you get the full $50,000. Beyond valuation, classic car policies account for how you actually use the vehicle. Most collectors don’t commute daily, so mileage caps of 2,500 to 5,000 miles per year are standard and keep premiums reasonable. Coverage also includes specialized protections standard policies ignore: spare parts coverage for rare components, restoration coverage for cars under active work, and dedicated roadside assistance for older vehicles. Liability and comprehensive coverage remain essential, but classic car policies layer in protections that reflect a collector’s real needs.

Setting an Agreed Value That Reflects Reality

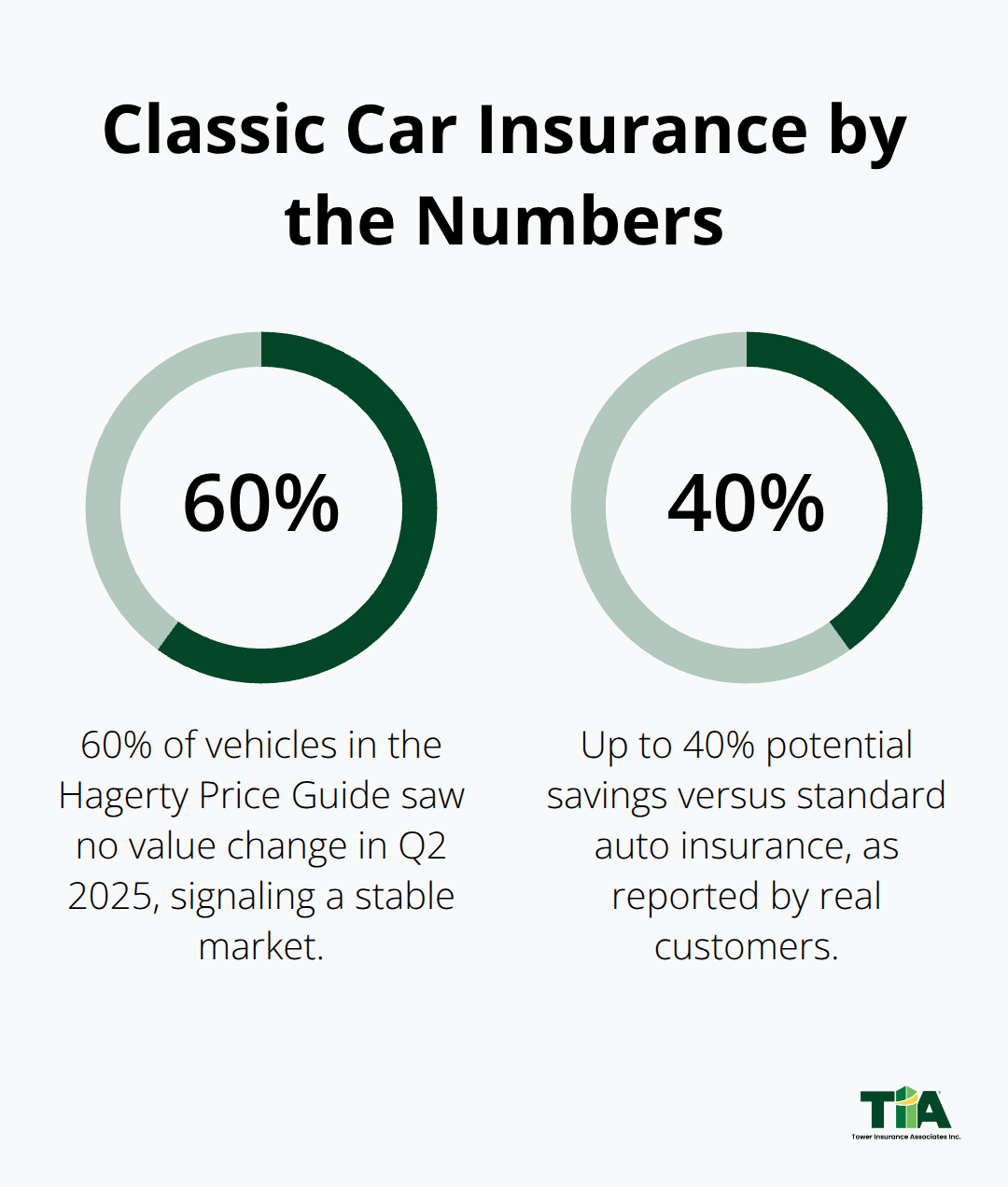

The agreed value you set directly affects what you’ll receive in a claim, so accuracy matters. Hagerty’s valuation tools track over 40,000 vehicles with more than 15 years of pricing history, providing model-specific data drawn from public auctions, private sales, dealer activity, and asking prices. The Hagerty Price Guide, updated quarterly, covers pre-war classics through modern collectibles and includes condition notes and equipment details that justify valuations. As of mid-2025, the classic car market sits roughly at the same level as early 2022 after peaking in 2022, meaning prices have stabilized and price declines have slowed. Roughly 60 percent of vehicles in the Hagerty Price Guide saw no value change in the second quarter of 2025, underscoring market stability. This steadiness allows you to set an agreed value and maintain it through semi-annual policy reviews rather than constant repricing.

Condition and Model Matter More Than Market Trends

When you check your car’s value using tools like classiccarvalue.com or Hagerty’s platform, focus on your specific model and condition rather than broad market trends. A 1965 Mustang in good condition may hold different value than a rare 1967 L88 Corvette, so detailed condition assessment matters far more than general market sentiment. The valuation data you find should reflect your car’s actual state-mileage, equipment, and maintenance history all influence what collectors will pay. Use these detailed valuations to work with your insurer on an agreed value that protects your investment without overstating it. With the right valuation in place, you’re ready to explore the specific factors that insurers consider when calculating your premium.

What Drives Your Classic Car Insurance Premium

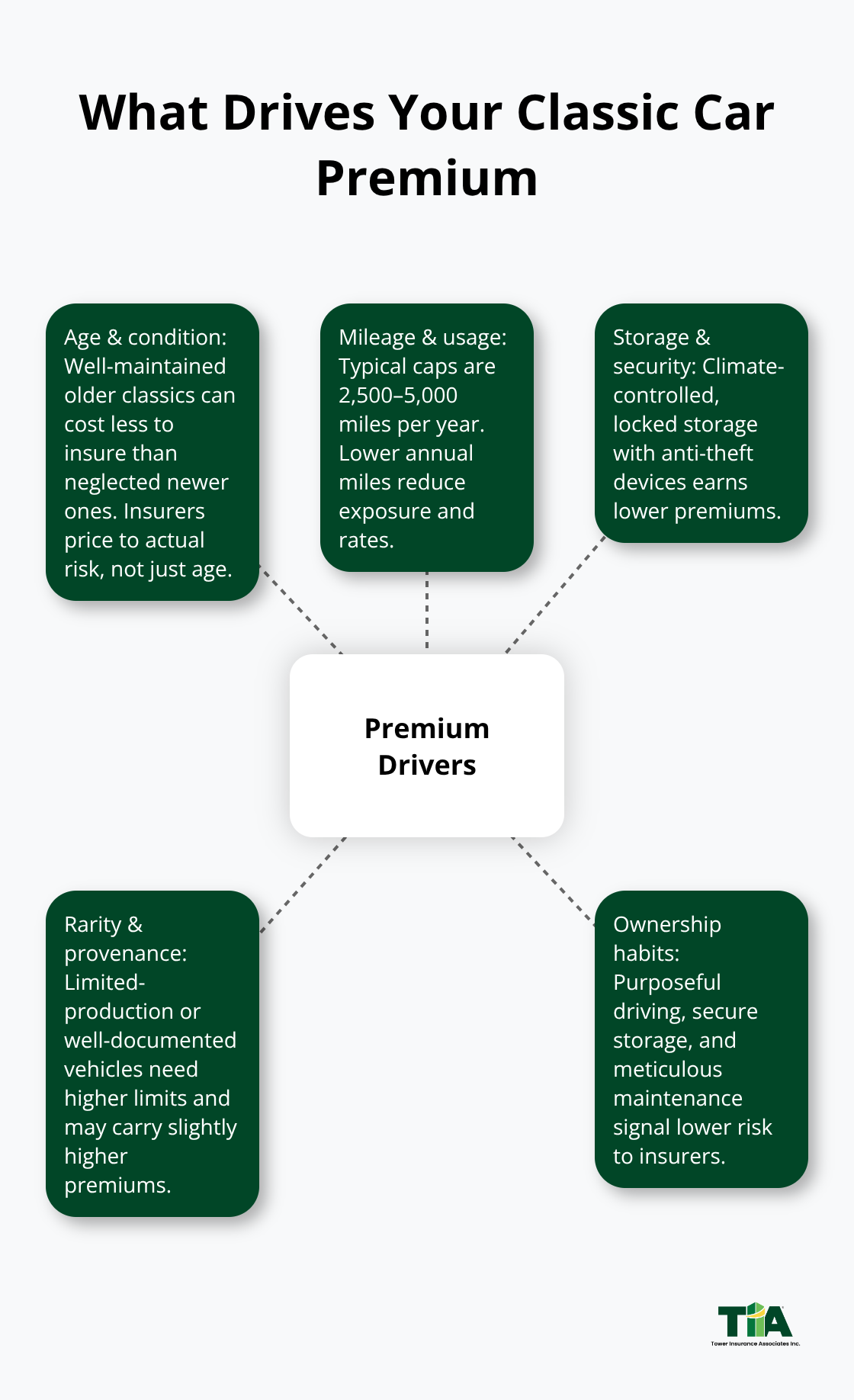

Age and Condition Set the Foundation

Your classic car’s age and condition form the foundation of your premium, but not in the way standard auto insurance calculates rates. A well-maintained 1972 Chevrolet Chevelle in excellent condition will cost less to insure than a neglected 1965 Ford Mustang in poor shape, even though the Mustang is older. Insurers recognize that older cars in stellar condition represent lower risk than newer classics that have been abused. Vehicle rarity also matters significantly-a limited-production model or a car with documented provenance requires higher coverage limits and may carry slightly higher premiums to protect that investment adequately.

Mileage and Usage Control Your Rate

How often you actually drive your classic car shapes your rate more than almost any other factor. Most classic car policies cap annual mileage between 2,500 and 5,000 miles, reflecting typical collector usage for shows, club events, and weekend drives rather than daily commuting. If you drive your classic fewer than 2,500 miles per year, you’ll pay less than someone who pushes toward 5,000 miles. This direct link between usage and premium makes sense: less time on the road means less exposure to accidents, theft, or weather damage.

Storage Quality and Security Measures Matter

Storage and security create the final piece of your rate calculation. A climate-controlled garage with anti-theft devices and secure locks will earn you a meaningfully lower premium than a car stored outdoors or in an unprotected structure. Insurers factor in storage quality when pricing your policy. Completing a defensive driving course or holding membership in a verified car club can unlock additional discounts, though availability varies by state and insurer, so confirm what applies in your location.

How These Factors Work Together

The practical reality is that you control most of these premium drivers through your ownership decisions. Store your car securely, drive it purposefully rather than constantly, and maintain it in excellent condition-these actions directly reduce your insurer’s risk and translate into lower premiums that reward responsible ownership. With your premium factors understood, the next step is selecting an insurer who recognizes the true value of your collection and structures coverage to match it.

Finding the Right Insurer for Your Collection

Specialists Versus Standard Carriers

Choosing between general auto insurers and specialists fundamentally shapes what you pay and how well your car stays protected. Most standard carriers either won’t insure classics at all or force them into policies designed for depreciating daily drivers, leaving coverage gaps that matter. Specialists like American Collectors Insurance, operating since 1976, structure policies around how collectors actually use their vehicles and what makes them valuable. At Tower Insurance Associates, Inc., we represent multiple top-rated carriers and work to match your classic car with the right specialist coverage, providing personalized service and claims advocacy that standard insurers rarely offer.

Questions That Reveal True Coverage

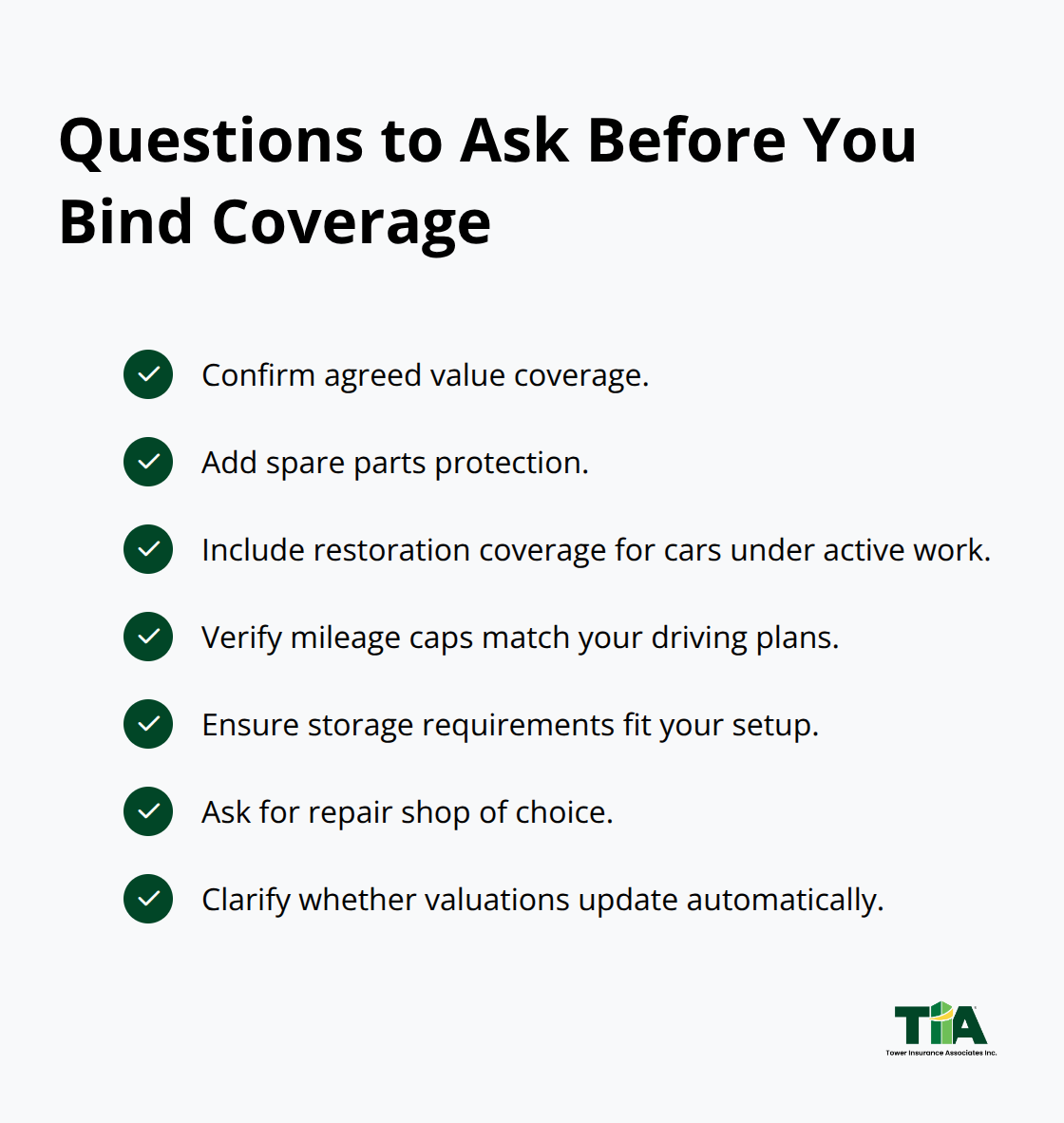

When you request a quote, ask directly whether the insurer offers agreed value coverage, spare parts protection, and restoration coverage for vehicles under active work. Ask about mileage caps and whether they align with your driving plans, and confirm that storage requirements match your actual setup. Ask if they have a repair shop of choice benefit, meaning you select where damaged cars go rather than the insurer dictating a facility unfamiliar with classics.

A critical question many collectors skip is whether the insurer updates valuations automatically or requires you to request reviews, because market shifts can leave your coverage misaligned with your car’s actual worth.

Evaluating Real Customer Experience

American Collectors Insurance maintains a 4.9 Trustpilot rating from over 20,000 reviews, reflecting real customer experience rather than marketing claims. Their C.A.R.E. program reimburses roadside and towing costs up to your policy limit while letting you choose the service provider, which matters when your 1970 Dodge Challenger breaks down 50 miles from home. Real customers report potential savings of up to 40 percent versus standard auto insurance, though your actual savings depend on your car’s value, driving habits, and storage quality. A 2-minute online quote from specialists lets you compare options quickly without lengthy phone calls.

Comparing Quotes Beyond Price Alone

Resist the temptation to pick the lowest number without examining what’s included. A $600 annual premium from a specialist covering agreed value, spare parts, and roadside assistance beats a $450 quote from a standard insurer that pays depreciated value and excludes restoration work. Request sample policy documents before committing, and review the specific coverage limits and exclusions rather than skimming summaries. Verify that any discounts mentioned during the quote process actually apply in your state, since defensive driving and car club discounts vary by location.

Alignment with Valuation Tools

Check whether your insurer participates in valuation tools like Hagerty’s platform, which tracks 40,000 vehicles with quarterly updates, because this alignment simplifies keeping your agreed value current without repeated appraisals. Ask how claims are handled for total loss situations, since the difference between an agreed value payout and a depreciated settlement can amount to thousands of dollars on a $50,000 classic. Specialists in collector vehicles understand that your car isn’t depreciating like a Honda Civic, and they price policies accordingly by focusing on your specific model, condition, and usage rather than applying broad depreciation formulas.

Final Thoughts

Your classic car represents years of passion and investment, and protecting it requires more than a standard auto policy can offer. Agreed value coverage, spare parts protection, and mileage allowances designed for weekend driving and car shows exist because classic cars operate differently than daily drivers. Your 1972 Chevelle isn’t depreciating like a new sedan, and your insurance shouldn’t treat it that way.

Setting an accurate agreed value using tools like Hagerty’s platform or classiccarvalue.com protects you from underpayment in a total loss claim. Storing your car securely and driving it purposefully reduce your premiums while keeping your investment safe. Request quotes from specialists who have built their business around collectors rather than treating classics as an afterthought, and ask about agreed value, repair shop choice, and roadside assistance tailored to older vehicles.

At Tower Insurance Associates, Inc., we represent multiple top-rated carriers and match collectors with the right coverage through personalized service. Visit our website to discuss your collection and find coverage that reflects what your classic car actually means to you.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.