California tech startups face a growing wave of cyberattacks that threaten their operations and bottom line. Ransomware, data breaches, and regulatory penalties are no longer distant risks-they’re happening now to companies like yours.

Tech startup cyber insurance has become essential protection against these threats. At Tower Insurance Associates, Inc., we help innovators understand what coverage actually matters and how to choose the right protection for their specific needs.

What Cyber Threats Are Actually Hitting California Startups Right Now

Ransomware and Attack Vectors Are Targeting Your Startup

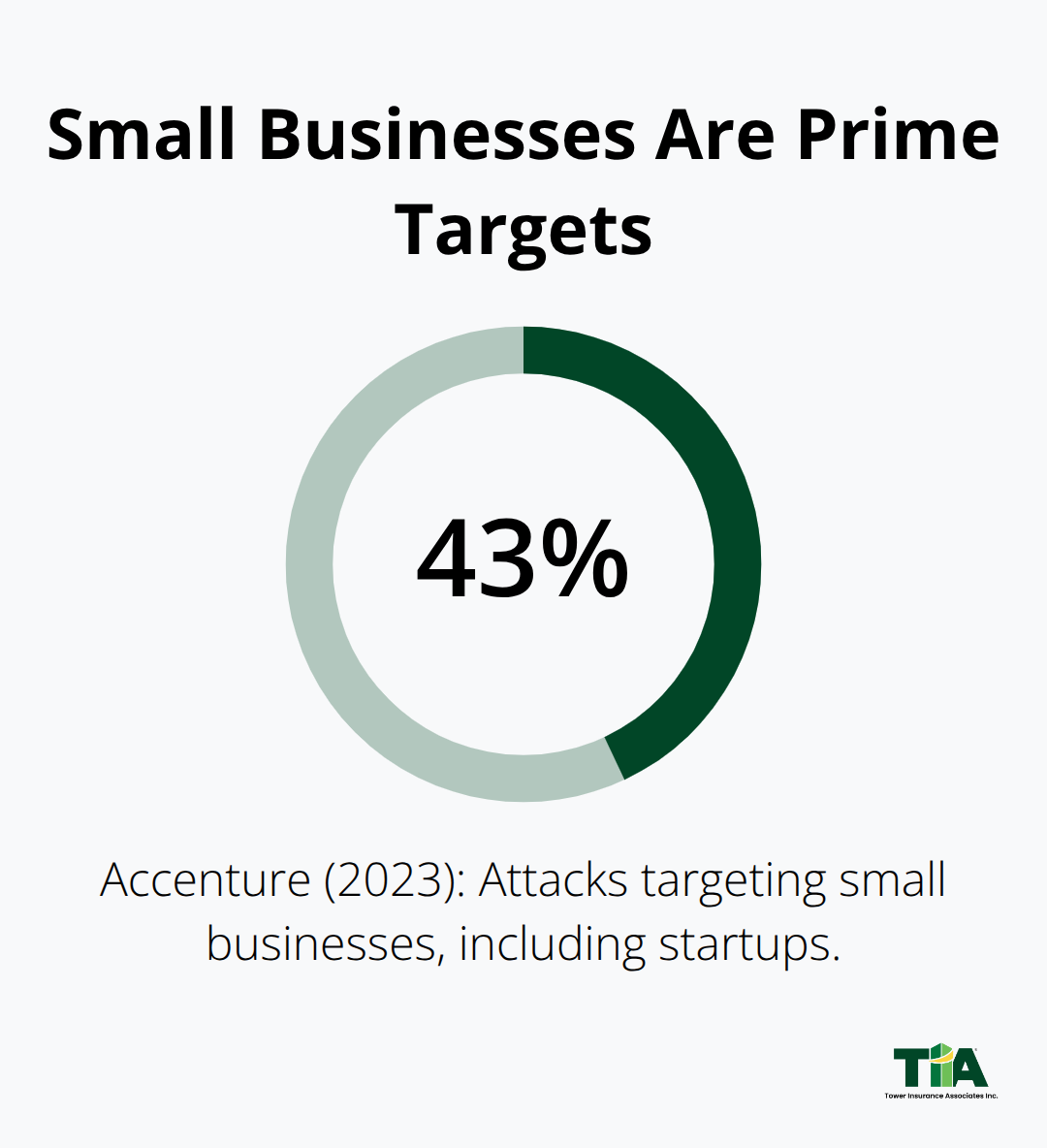

Ransomware attacks on California tech companies have accelerated dramatically. The FBI Internet Crime Report identifies business email compromise as a top attack vector nationwide, and California startups are prime targets because they typically lack mature security operations centers. Accenture’s 2023 research found that 43% of cyberattacks targeted small businesses, making your startup statistically likely to face an incident within the next few years. Guardz’s 2025 report shows that nearly half of U.S. small and medium businesses experienced a cyberattack in the past five years, with over a quarter hit in the last 12 months alone. These aren’t theoretical threats-they’re happening to your peers right now.

The attack vectors remain predictable and exploitable. Credential theft, phishing emails, and unpatched systems serve as the dominant entry points for attackers. Your startup probably operates with limited IT staff, which means attackers know you have fewer eyes monitoring your network and slower patch cycles than larger enterprises.

The Financial Damage From a Breach Threatens Your Bottom Line

The financial damage from a breach is staggering and often underestimated by founders focused on product development. IBM’s 2025 breach-cost study found U.S. breach costs average about $10.22 million, driven by forensics, notification expenses, downtime, and lost productivity. For a startup with $5 to $20 million in annual revenue, a breach can be existential. Cybercrime damages are projected to reach $10.5 trillion annually by 2025 globally, according to Cybersecurity Ventures, underscoring the scale of risk.

California Privacy Laws Multiply Your Regulatory Exposure

California’s privacy laws compound the financial problem significantly. The California Consumer Privacy Act and California Privacy Rights Act impose fines up to $7,500 per violation for mishandled personal data, and a large breach can trigger hundreds or thousands of violations instantly. If your startup stores customer payment information, health data, or personally identifiable information, regulatory penalties alone can bankrupt you before you address the technical remediation.

This regulatory exposure makes cyber insurance a financial survival mechanism rather than an optional expense. The next section examines the specific coverage types that protect your startup from these mounting threats.

What Your Cyber Insurance Actually Needs to Cover

First-Party Breach Costs Demand Immediate Coverage

Your cyber insurance policy must address three financial realities that hit your startup after an attack: the immediate costs of managing the breach itself, the revenue you lose while systems are down, and the legal bills from customers or regulators demanding answers. Most founders underestimate how quickly these costs compound.

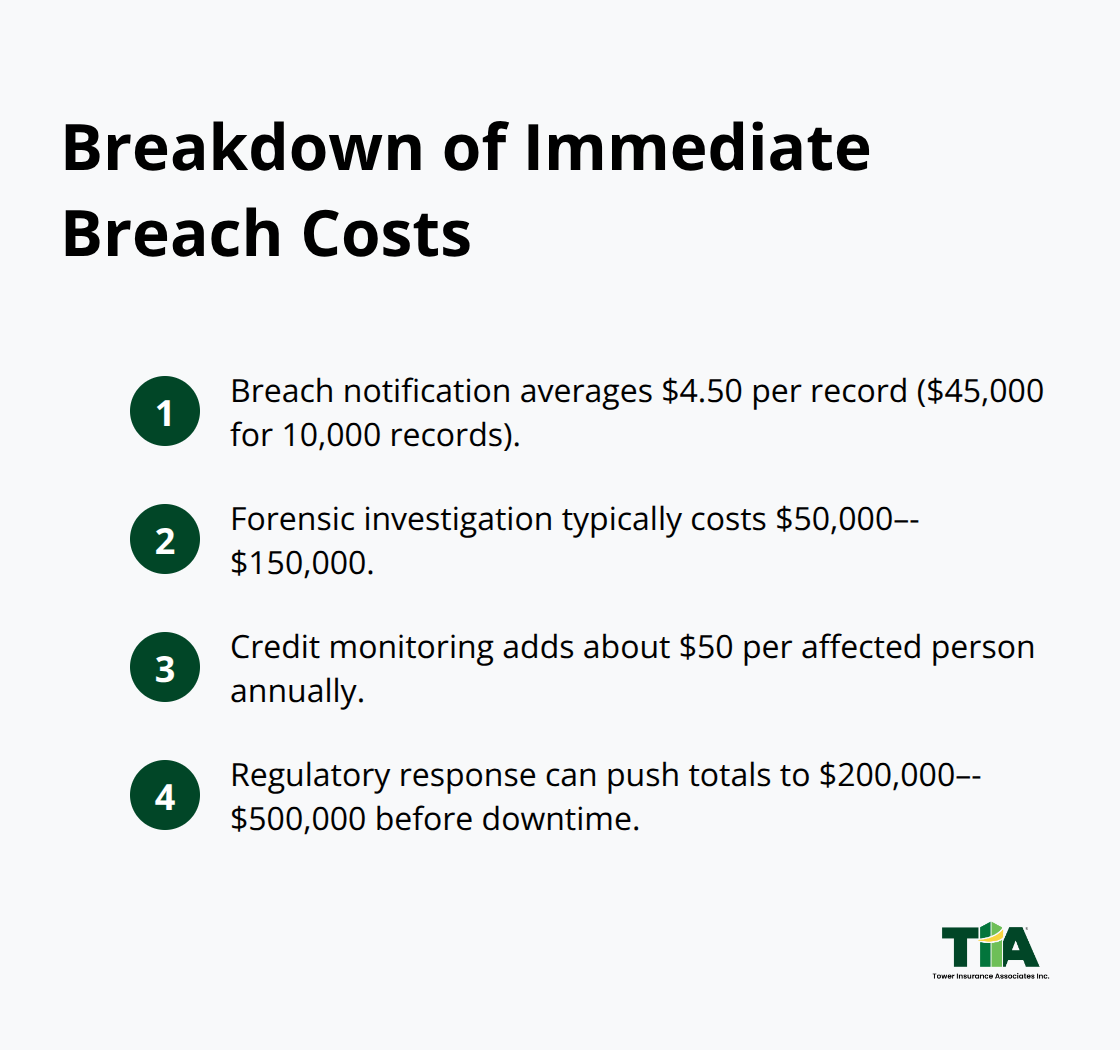

Breach notification costs $4.50 per compromised record according to IBM’s 2025 data, meaning a breach affecting 10,000 customer records runs $45,000 just to notify people. Forensic investigation typically costs $50,000 to $150,000, and credit monitoring services for affected customers adds another $50 per person annually. Regulatory response costs pile on top, and you’re easily at $200,000 to $500,000 before your business loses a single dollar to downtime.

Your policy must cover these first-party expenses because they happen regardless of whether you face a lawsuit. Ransomware incidents specifically require coverage for incident response retainers, which means having pre-negotiated forensics and legal firms ready before an attack occurs-not scrambling to find them afterward when attackers demand payment within 72 hours.

Business Interruption Coverage Protects Your Runway

Business interruption coverage protects your runway when a breach forces you offline. If your SaaS platform goes down for five days during remediation, every hour of downtime costs you revenue and undermines your ability to deliver service to customers who may then demand refunds or terminate contracts. A startup with $2 million in annual recurring revenue loses roughly $27,000 per day of downtime. Your policy should cover both the direct income loss and your ongoing fixed costs-payroll, rent, cloud infrastructure-that continue even when you generate zero revenue.

Third-Party Liability Coverage Shields You From Lawsuits

Third-party liability coverage matters because customers, vendors, or regulators will sue you after a breach, and your legal defense costs often exceed the settlement itself. California privacy law gives customers a private right of action to sue for statutory damages, meaning a breach affecting 5,000 customers could theoretically trigger 5,000 individual lawsuits. Your policy must cover defense counsel, regulatory fines up to the $7,500-per-violation threshold, and settlements.

Coverage Gaps That Derail Claims

When comparing carriers, demand explicit coverage for ransomware variants, social engineering losses, and third-party vendor breaches-these are the gaps where startups get denied claims. The next section walks you through how to evaluate carriers and select the protection that actually matches your startup’s risk profile.

Selecting a Cyber Insurance Carrier That Matches Your Startup’s Reality

Map Your Data and Coverage Needs First

Your startup operates differently from an enterprise with dedicated security teams and massive budgets, so your policy needs to reflect that operational reality. Start by mapping what data your startup actually handles and where it lives. If you process customer payment information, you need PCI compliance coverage explicitly stated in your policy. If you store health data, your policy must cover HIPAA breach notification costs. If you’re a SaaS platform, your policy must explicitly cover business interruption from ransomware attacks that force your infrastructure offline.

Select Carriers With Tech Startup Experience

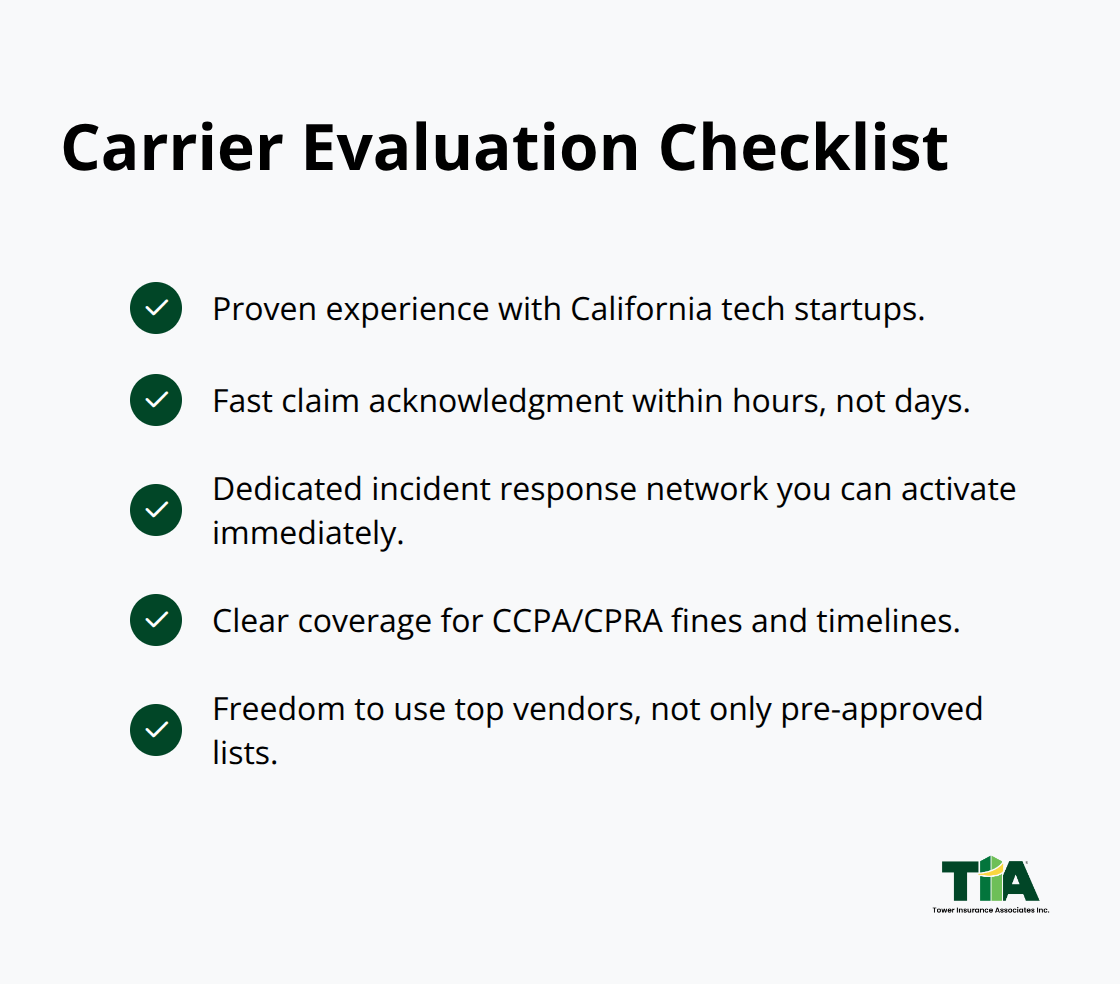

The carrier you select should have underwritten other California tech startups in your specific vertical because they’ll understand your attack surface better than a generalist insurer. Chubb, AIG, AXA XL, and Beazley have invested substantially in tech-focused underwriting and maintain dedicated incident response networks that startups can activate immediately after an attack. These carriers also understand California’s regulatory landscape, which matters because a carrier unfamiliar with CCPA fines and breach notification timelines will underprice your regulatory defense coverage.

Scrutinize Deductibles and Sublimits

Deductibles and sublimits determine what your startup actually pays out of pocket when a breach happens. A $10,000 deductible sounds reasonable until you’re paying forensics firms $75,000 to $150,000 from your own cash reserves while waiting for insurance reimbursement. Ransomware coverage frequently comes with separate sublimits that cap how much the insurer will pay for ransom negotiation, incident response, or extortion payments. Ask your carrier directly whether ransomware coverage includes pre-incident retainers for forensics and legal counsel because startups that lack these relationships pre-attack waste critical hours finding vendors while attackers demand payment.

Evaluate Claims Support Quality

Claims support quality separates adequate carriers from exceptional ones. Request references from other California startups who’ve filed claims with each carrier and ask specifically about response time to initial breach notification and how quickly the insurer deploys incident response resources. A carrier that takes 48 hours to acknowledge your claim while attackers maintain access to your systems costs you significantly more than a carrier responding within hours.

Guardz’s 2025 report on SMB cyberattacks documents the scale of threats facing small businesses, meaning your peers have filed claims and can tell you which carriers actually perform when crisis hits. Avoid carriers that require you to use their pre-approved vendors because those relationships often prioritize cost over speed, and in a breach, speed determines whether you lose $100,000 or $1 million in damages.

Final Thoughts

Cyberattacks against California tech startups accelerate every quarter, and the financial consequences of inaction far exceed the cost of proper insurance coverage. Ransomware, data breaches, and regulatory penalties will strike your startup unless you transfer that risk to a carrier prepared to respond within hours when crisis hits. Tech startup cyber insurance separates companies that recover from incidents and those that fail to survive them.

The coverage you need addresses three financial realities that emerge after a breach: first-party costs for forensics and notification that exceed $500,000 before your business loses a single dollar to downtime, business interruption protection that preserves your runway when systems go offline, and third-party liability coverage that shields you from lawsuits and regulatory fines that California privacy law explicitly permits customers to file against you. Carriers with tech startup experience understand your attack surface, California’s regulatory landscape, and the incident response resources you need activated immediately (not days later) after a breach occurs. Deductibles and sublimits determine what you pay out of pocket, so scrutinize these numbers carefully before signing any policy.

Map the data your startup handles, identify your specific coverage gaps, and request quotes from carriers with proven experience protecting California tech companies. Tower Insurance Associates, Inc. represents multiple top-rated carriers and specializes in tailored cyber liability coverage for startups in your market.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.