Design projects carry real financial risk. A missed deadline, miscommunication about deliverables, or a client dispute over final work can quickly become expensive problems that standard business insurance won’t cover.

Professional liability for designers protects you when things go wrong. At Tower Insurance Associates, Inc., we’ve seen how the right coverage makes the difference between a manageable claim and a business-threatening lawsuit.

What Professional Liability Actually Covers

How Professional Liability Protects Your Design Work

Professional liability insurance protects you from financial loss when your design work causes a client to suffer damages. This means coverage applies when a client claims your design created a problem that cost them money-whether that’s a faulty website that lost them sales, a brand identity that damaged their reputation, or construction documents with errors that led to costly rework. The policy covers your legal defense costs, settlements, and judgments up to your coverage limit.

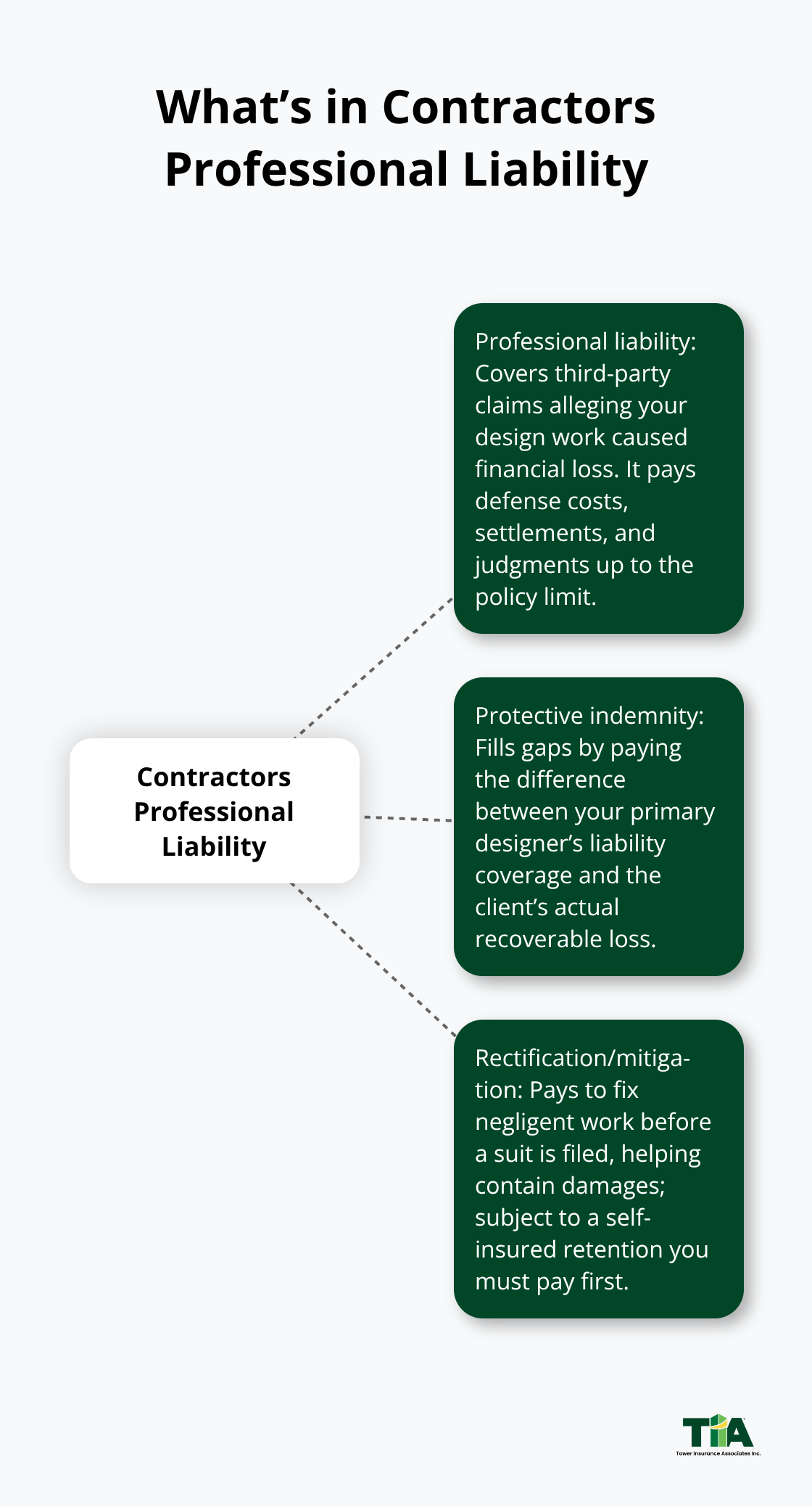

Contractors Professional Liability typically includes professional liability for third-party claims, protective indemnity for first-party losses, and rectification or mitigation coverage for the cost of fixing your negligent work. This structure matters because each component handles different scenarios. If a client sues you directly, professional liability kicks in. If you need to pay out of pocket to correct your mistake before the client sues, rectification coverage covers those repair costs, though it carries a self-insured retention you’ll pay first.

The Layered Protection Model

Protective indemnity fills gaps by paying the difference between what the designer’s liability policy covers and what the client actually needs to recover. Without this layered approach, a single claim can exceed your primary coverage limit and expose your business to catastrophic loss. The combination of these three components creates a safety net that standard policies simply cannot provide.

Why Your General Business Policy Falls Short

Standard commercial general liability insurance excludes professional services. Your CGL policy covers bodily injury and property damage from accidents on your premises or during operations-a client trips in your office, someone gets hurt at your event. It does not cover claims arising from the quality of your professional work.

A designer who causes financial loss through poor judgment, missed deadlines, or technical errors will find their CGL policy denies the claim because the damage stems from professional negligence, not a covered peril. Errors and omissions coverage is purpose-built to handle professional mistakes. It covers the cost of defending against claims that your design work was inadequate, incomplete, or caused economic loss.

Rising Claims Trends in Design Work

Claims data shows rising frequency and severity in design-related disputes, driven by design-build delivery models and construction-management errors in scheduling, cost estimating, and sequencing. Many claims settle in the hundreds of thousands, but design and engineering claims can reach into the tens of millions when they involve large construction projects or widespread brand damage.

Waiting until a claim arrives to discover your CGL won’t cover professional liability means facing legal bills and potential judgments entirely from your own pocket. The gap between what you think you’re covered for and what you actually are covered for can become the difference between staying in business and closing your doors. Understanding what protects your work-and what doesn’t-shapes every contract you sign and every project you take on.

How to Build Contracts That Prevent Design Disputes

Specify Your Scope and Deliverables in Writing

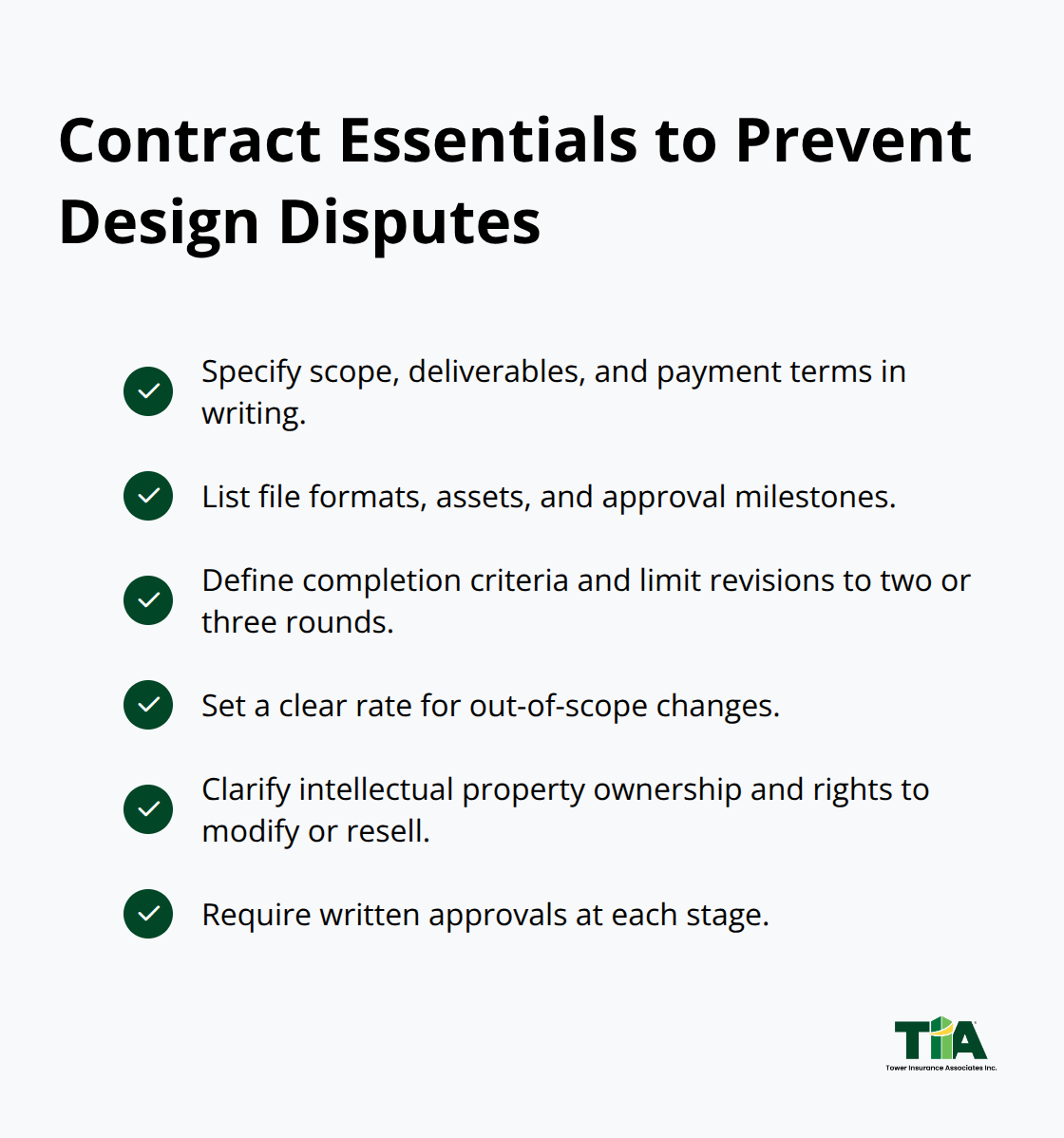

The contract you sign before starting a design project is your first and most important risk management tool. A vague scope of work invites disputes because the client’s expectations and your deliverables won’t align. Your contract must specify exactly what you’re designing, how many rounds of revisions are included, what happens if the client requests changes outside the scope, and when payment is due.

Include a detailed deliverables section that lists every file format, every design asset, and every approval milestone. Define what constitutes completion so the client cannot claim unfinished work months later. Set a clear limit on revision rounds-typically two to three-and charge a defined rate for additional revisions. Specify who owns the intellectual property, especially if the client pays for custom work.

Many design disputes stem from disagreements over IP ownership or the client’s right to modify and resell your work.

Protect Yourself with Liability Limits and Written Approvals

Add a limitation of liability clause that caps what you’re responsible for if something goes wrong. This protects you from catastrophic claims and often qualifies for a premium discount on professional liability insurance.

Your contract should also require the client to approve deliverables in writing at each stage, creating a documented trail that proves they reviewed and accepted your work before moving forward. This written approval becomes your defense if the client later claims you delivered something different from what they expected.

Document Every Decision and Change Request

Documentation throughout the project is equally critical because claims often hinge on whether you can prove you did what you promised. Create a project file that contains every email exchange, every revision request, every approval email from the client, and every invoice. When the client requests changes, respond in writing-not verbally-and confirm what they asked for and what the cost or timeline impact will be.

Take screenshots of client approvals in your design tools if they’re reviewing work there. If a client claims you missed a deadline or delivered the wrong asset, your email trail and timestamped files become your defense against liability. This paper trail demonstrates that you acted professionally and met your obligations.

Implement Quality Control and Client Communication Checkpoints

Quality control processes reduce the risk that your work contains errors that trigger claims. Before delivering anything, have a second person review the design for accuracy, consistency, and completeness. For construction documents or technical designs, a peer review catches errors in measurements, specifications, or sequencing that could lead to costly rework on the job site.

Establish communication checkpoints where you confirm the client’s priorities, constraints, and success criteria before you start designing. Ask specific questions: What is the budget? Who is the end user? What problem does this design solve? What are the non-negotiables? Document their answers in writing. This prevents the client from later claiming they never told you something critical.

Move Beyond Email: Schedule Formal Approval Meetings

Schedule formal approval meetings at key milestones rather than sending designs via email and hoping for feedback. In a meeting, you can discuss concerns in real time, clarify misunderstandings, and get explicit sign-off that moves the project forward. A designer who communicates clearly and documents everything creates a record that demonstrates professional competence if a claim ever arises. This foundation of clear contracts and documented communication sets the stage for selecting insurance coverage that actually protects the risks you face on every project.

How Much Coverage Do You Actually Need

Calculate Your True Exposure

The most dangerous mistake designers make is selecting a coverage limit based on price instead of actual risk. A designer with a $1 million limit might think they’re protected until a construction document error costs a client $3 million in rework, leaving them personally liable for the gap. Firms underestimate their exposure because they focus on keeping premiums low rather than matching coverage to the scope and dollar value of projects they undertake. Your coverage limit should reflect the largest financial loss a single project could create, not the smallest premium you can afford.

If you design websites, your exposure per project might reach $250,000 to $500,000 in lost sales claims. If you produce construction documents for commercial buildings, a single error can trigger claims exceeding $2 million. Bodily injury claims are resulting in much higher verdicts, often referred to as ‘nuclear verdicts,’ and settlements that insurers continue to monitor closely.

Start by calculating the total contract value of your largest projects, then add 50 percent as a buffer for indirect damages like lost revenue or reputational harm. That number should inform your minimum coverage limit.

Choose Between Project-Specific and Practice Programs

Most insurers writing professional liability for designers offer limits ranging from $1 million to $10 million, with a few markets extending to $25 million for large firms or specialized practices. Your policy structure matters as much as the limit itself.

A project-specific policy provides a dedicated limit for a single project during its duration and extended reporting period, which works well for high-value, one-off engagements. A practice program provides an annual aggregate limit that can reinstate but gets eroded by claims on other projects throughout the year, making it better suited to firms handling multiple smaller projects. If you work on design-build contracts or construction management, add protective indemnity coverage-it pays the difference between your primary designer’s liability limit and what a client actually needs to recover. Without it, you’re exposed to gaps that can bankrupt the business.

Understand Current Pricing Trends

The cost of professional liability insurance has increased significantly in recent years. Industry data shows practice program rates have trended upward 2 to 5 percent year over year, with residential and heavy civil projects facing stricter underwriting. Your premium depends on firm size, number of projects, geographic location, prior claims history, and the specific services you offer.

A small firm with less than $1 million in annual revenue might pay $1,500 to $3,000 annually for a $1 million limit. A mid-sized firm with $5 million in revenue typically pays $4,000 to $8,000 for similar coverage. These are baseline figures-rates climb significantly if you have prior claims, work in high-risk sectors like construction management, or operate in states with aggressive litigation environments.

Earn Premium Credits Through Risk Controls

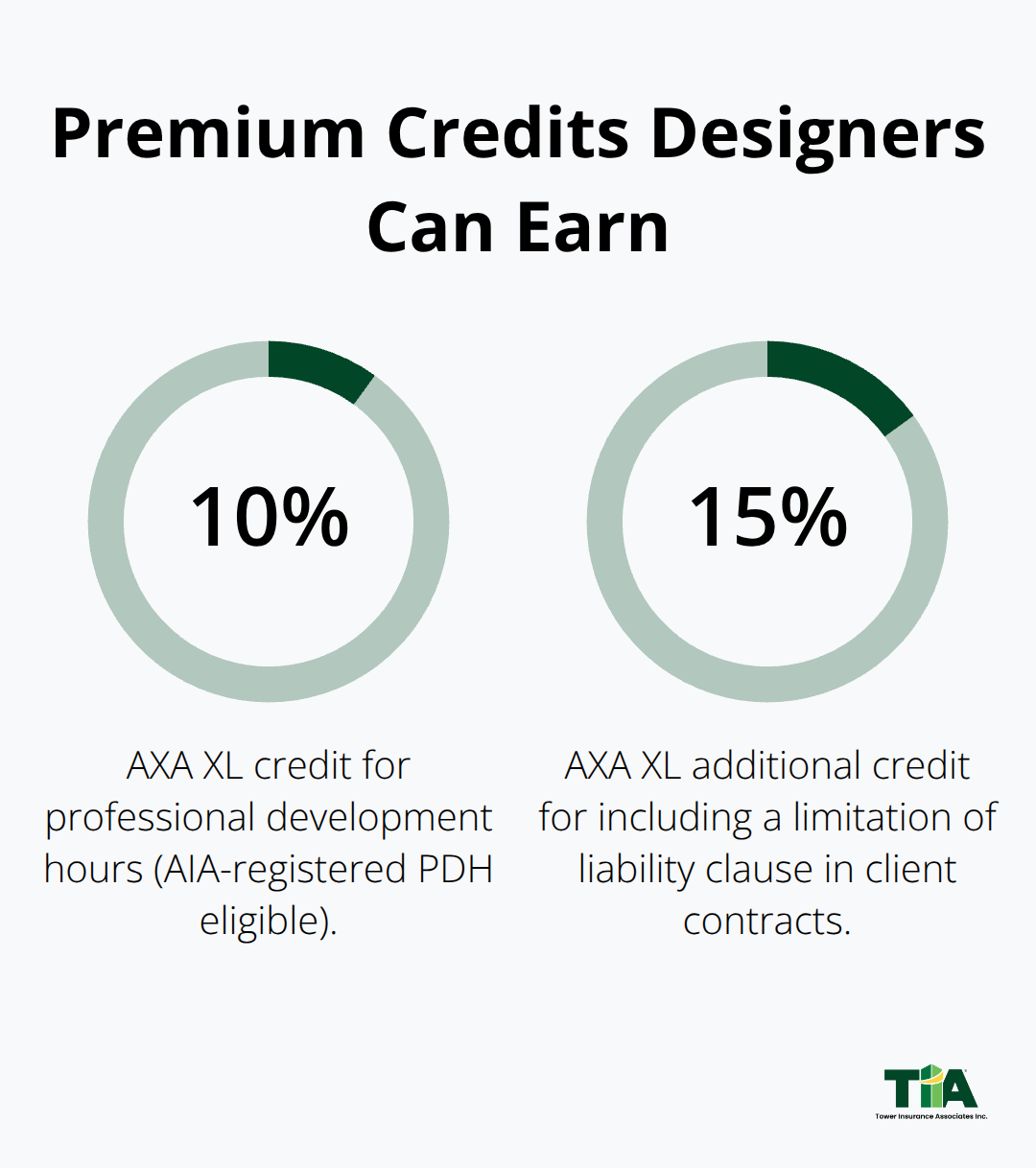

Some carriers offer premium credits worth 5 to 15 percent if you implement risk controls like peer review processes, written scope documentation, or continuing education in your field. AXA XL offers up to 10 percent premium credit for professional development hours earned during the policy year, with architects earning AIA-registered PDH credits. They also provide up to 15 percent additional credit for including a limitation of liability clause in client contracts, which directly rewards the risk management practices you already implemented in your agreements.

Get Competitive Quotes from Multiple Carriers

Request quotes from at least three carriers because rates and appetite vary widely based on how underwriters assess your specific risk profile. An independent insurance agency representing multiple top-rated carriers can help you find competitive pricing and tailored coverage that matches your actual exposures rather than forcing you into a one-size-fits-all program.

Final Thoughts

Professional liability for designers protects your business when claims arrive, and they will arrive. A client misunderstands your deliverables, a construction document contains an error, or a website redesign underperforms-without coverage, you pay these costs from your own pocket. With the right policy matched to your actual exposure, your insurer covers legal defense, settlements, and judgments up to your limit, protecting both your business and your personal assets.

The market is tightening rapidly. Fewer insurers write professional liability coverage, especially for high-risk sectors like construction management and design-build projects, while rates climb 2 to 5 percent annually. Waiting to purchase coverage becomes more expensive and harder to obtain as capacity shrinks. Designers who secure adequate limits now avoid the risk of becoming uninsurable later or facing significantly higher premiums.

Calculate the largest financial loss a single project could create, then add a buffer for indirect damages and request quotes from multiple carriers to compare limits, pricing, and premium credits. We at Tower Insurance Associates, Inc. represent multiple top-rated carriers and can match you with professional liability insurance that protects your actual exposures without overpaying for unnecessary coverage.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.