Engineering firms face mounting exposure to costly claims that standard liability policies simply don’t cover. Design errors, construction defects, and specification failures can drain resources and damage your reputation in ways most business owners don’t anticipate.

At Tower Insurance Associates, Inc., we’ve seen how the right engineering professional liability coverage transforms risk management from a constant worry into a manageable part of operations. This guide walks you through the real threats your firm faces and the concrete steps to protect it.

What Professional Liability Actually Covers for Engineers

The Core Protection Professional Liability Provides

Professional liability insurance for AEC firms covers design and engineering errors that cause financial loss. This means claims tied to design mistakes, specification failures, inadequate construction administration, or failure to meet the standard of care in your profession. Unlike general liability, which responds to bodily injury or property damage claims, professional liability protects against financial losses that stem directly from your professional work.

Most AEC claims involve economic loss rather than physical injury, making professional liability the essential gap-filler that general liability policies explicitly exclude. Your policy responds when a client alleges that your design was flawed, your calculations were wrong, your specifications conflicted with site conditions, or your oversight during construction allowed defects to go undetected.

What Your Policy Actually Pays For

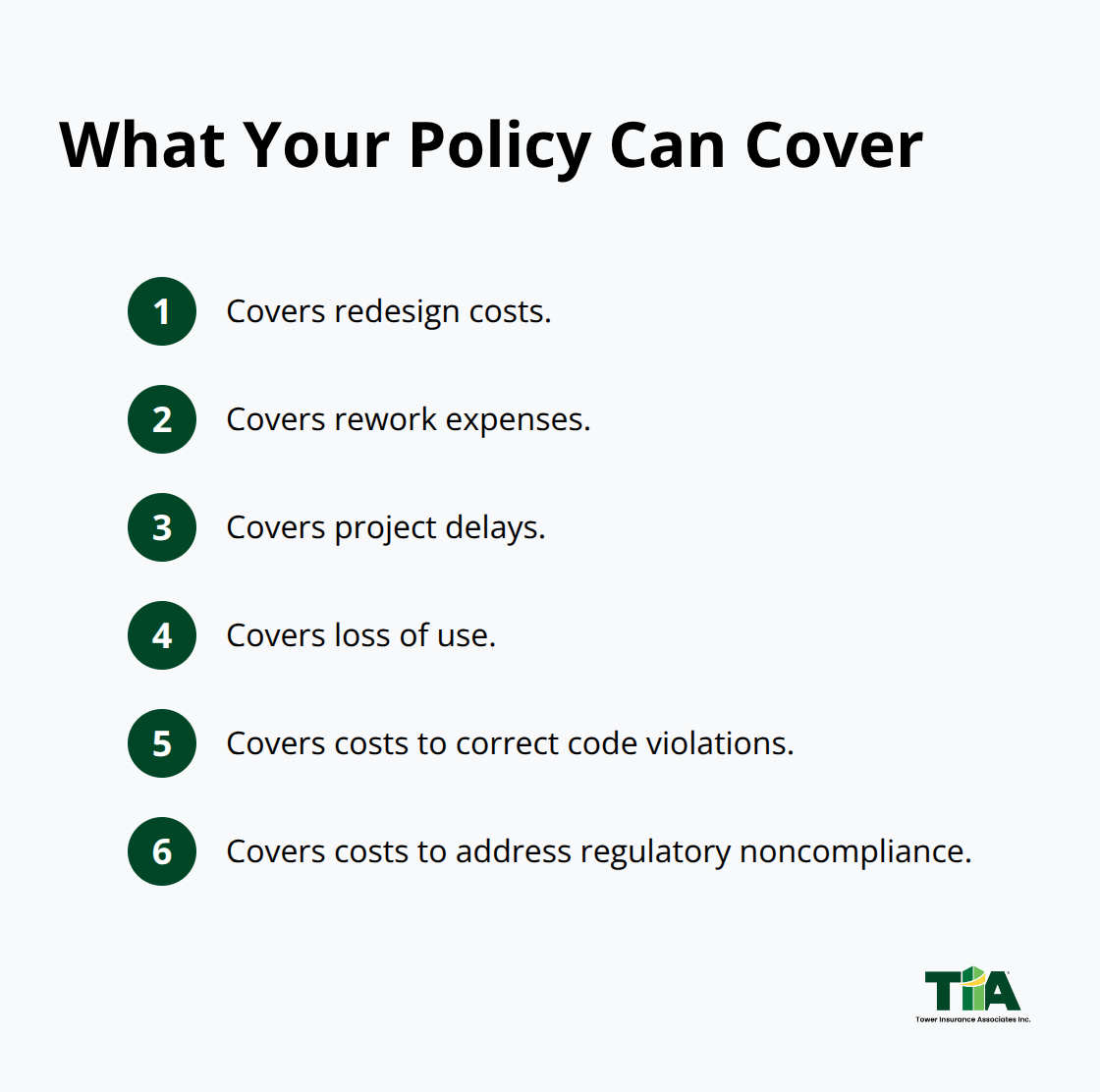

Coverage typically extends to redesign costs, rework expenses, project delays, loss of use, and the costs to correct code violations or regulatory noncompliance. However, the scope of coverage depends entirely on how your policy is written and what exclusions apply. Common exclusions block coverage for intentional wrongdoing, guarantees of cost or schedule, known defects you failed to disclose, and certain high-risk delivery methods unless specifically endorsed.

The Claims-Made Trap and Long-Tail Exposure

Claims-made policies mean you receive coverage only if the claim is filed during your policy period, not when the work was performed, which creates long-tail exposure since design defects often surface years after project completion. A $1 million policy limit that sounds adequate can evaporate quickly once defense costs mount, especially in multi-party disputes or litigation that stretches across several years.

This extended timeline means your defense costs stretch longer and chip away at available limits.

Why General Liability Leaves You Exposed

Standard commercial general liability policies actively exclude professional liability claims, leaving your firm exposed to six-figure design-error claims with no coverage backing. Your CGL policy won’t respond to a claim that your structural design was inadequate, that your MEP specifications created conflicts, or that you failed to catch a code violation during plan review. This gap between what you think you’re covered for and what you actually are covered for is precisely why design and construction defects pose such a threat to your bottom line.

Where Design Errors Become Financial Disasters

Structural Design Errors and Their Hidden Costs

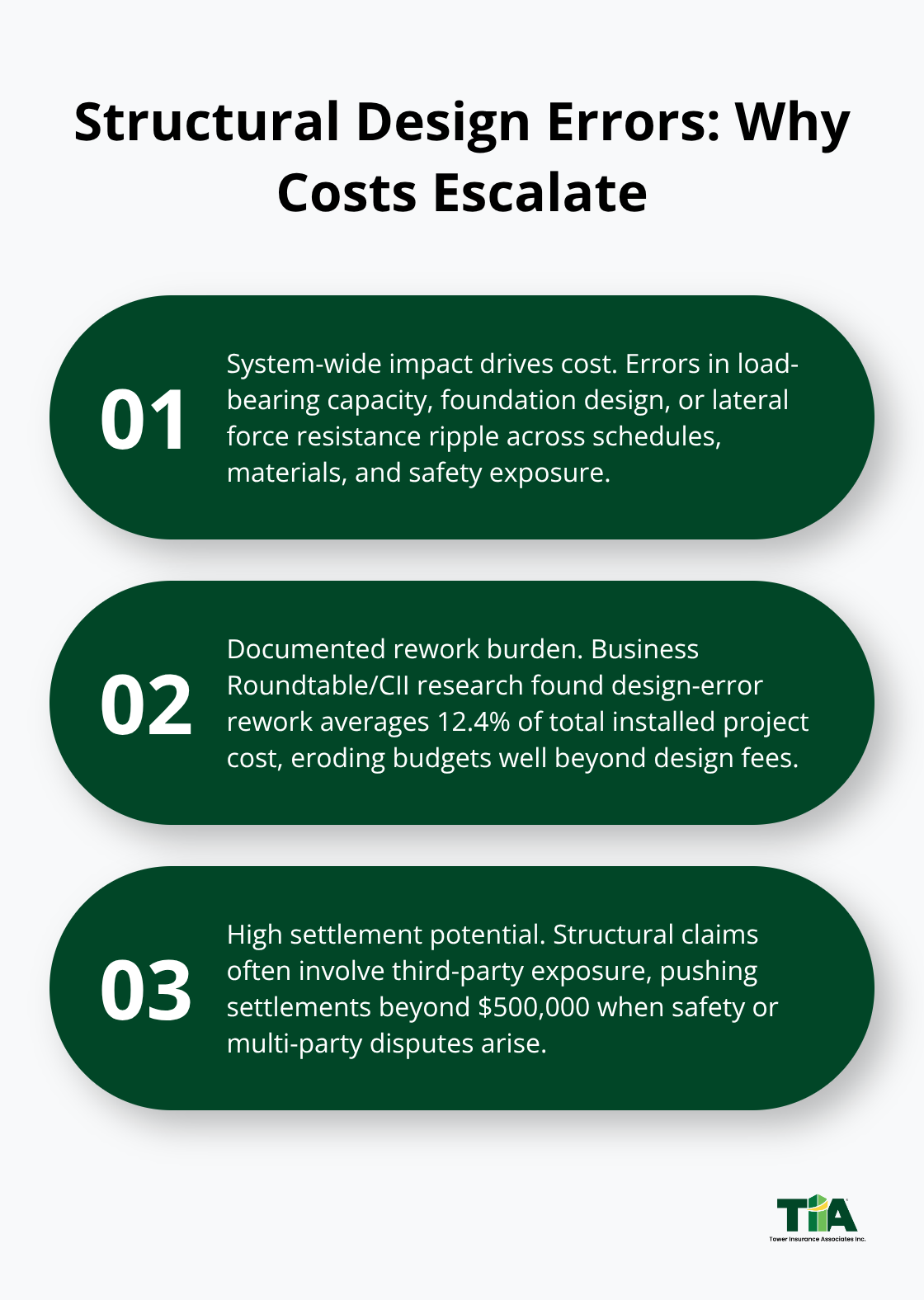

Structural design errors represent one of the costliest categories of engineering claims because they affect entire project systems rather than isolated components. A miscalculation in load-bearing capacity, foundation design, or lateral force resistance triggers not just redesign costs but also construction halts, material waste, and potential safety liability. The Business Roundtable and Construction Industry Institute documented that rework costs from design errors account for an average of 12.4% of the total installed project cost.

These errors often remain hidden during early construction phases, surfacing only when contractors encounter field conflicts or structural inspections reveal inadequate capacity. At that point, corrective measures demand emergency redesigns, accelerated schedules, and compounded labor costs that dwarf the original design fee. Settlement costs for structural claims frequently exceed $500,000 because they involve third-party exposure-not just the owner’s loss, but potential liability to contractors, subcontractors, and future occupants if safety is compromised.

Construction Defect Claims and Blurred Responsibility

Construction defect claims present a different but equally damaging exposure because they blur responsibility between design and construction execution. A specification that conflicts with site conditions, MEP coordination failures that create field clashes, or incomplete approved-for-construction drawings that force contractors to improvise all generate defect claims that linger for years after project completion. Great American Insurance Group data shows that claims arising from client-drafted contracts average around 401 days to resolve, compared to 261 days for industry-standard forms, meaning disputes over who designed what and who built it wrong stretch timelines and drain resources.

Late RFIs-requests for information-during construction trigger defect claims because they force field changes under time pressure, increasing the likelihood of errors or incomplete solutions. Your firm bears vicarious liability for subconsultant errors unless you implement rigorous prequalification, require proof of insurance, and maintain documented quality control over their work.

Productivity Loss and Extended Settlement Demands

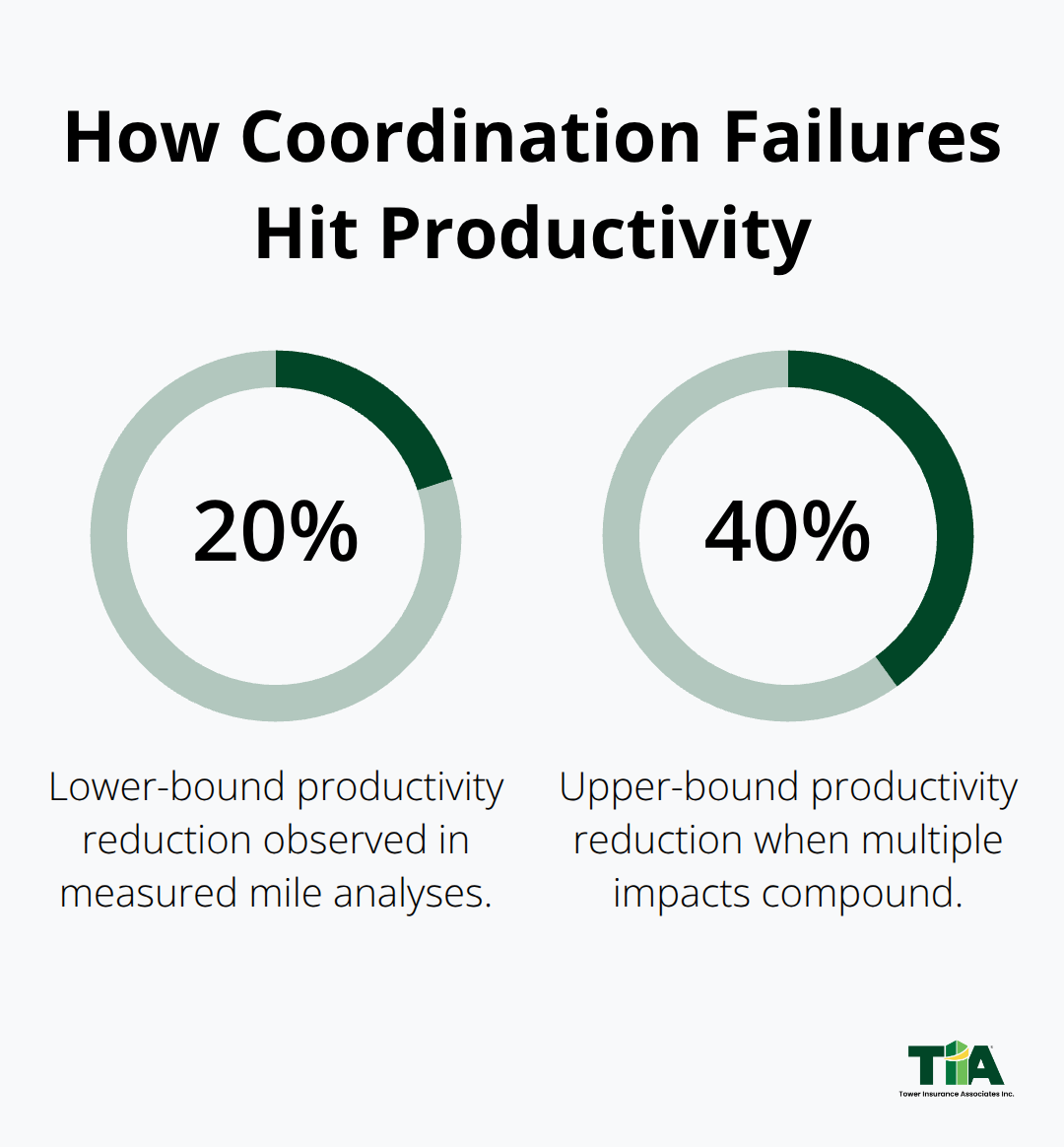

The measured mile approach, which compares productivity on unimpacted versus impacted project phases, shows that coordination failures alone reduce labor productivity by 20–40%, translating into settlement demands that reflect both direct rework costs and extended overhead allocations calculated under the Eichleay formula. These productivity losses compound quickly when multiple trades experience delays or when field changes force crews to work inefficiently.

Understanding how design errors cascade into construction defects and productivity losses reveals why your professional liability coverage must account for both immediate redesign costs and the extended financial exposure that emerges months or years later. The next section examines how engineering firms can implement quality control procedures and documentation practices that reduce these risks before claims arise.

How to Build a Risk Management System That Actually Prevents Claims

Implement Peer Reviews Before Documents Leave Your Office

Quality control procedures separate firms that manage claims from firms that prevent them entirely. Firms implementing structured peer reviews of design documents catch potential errors before release, compared to firms relying on individual designer accountability alone. A peer review means assigning an experienced professional unconnected to the original design to examine structural calculations, MEP coordination, code compliance, and specification consistency against site conditions.

This review must happen before documents go to the contractor, not after field problems surface. Document the reviewer’s findings in writing and require the original designer to address each flagged item with documented corrections or justification. Many firms skip this step because it feels like duplicate work, but the cost of one prevented structural claim far exceeds years of peer review expenses.

Track Deliverables and Maintain Submittal Logs

Establish a project checklist system that tracks deliverable deadlines, document completeness, and approval signatures throughout design and construction phases. Your checklist should flag incomplete approved-for-construction drawings before 50% of construction documents reach the contractor, because late or incomplete drawings force field improvisation that generates defect claims. Assign one person to maintain a submittal log recording when shop drawings and RFIs arrive and when responses leave your office, because response delays during construction create schedule impacts that contractors quantify into settlement demands.

Centralize all project communications, contracts, and approvals in a single document management system so that critical decisions made in person get documented in writing immediately afterward and remain retrievable years later when a claim surfaces.

Create an Evidence Trail Through Documentation

Detailed records transform disputes into defensible positions because they create an evidence trail showing your standard of care and good-faith effort to coordinate and communicate. Maintain shop drawing logs that document received dates, your review comments, and your response dates, because these records prove you performed adequate construction administration even when field conditions changed. When a contractor or subconsultant proposes a field solution that deviates from your design, require written documentation of that proposal and your approval or rejection so no ambiguity exists about who made the decision.

Use standard contract forms aligned with AIA or EJCDC language because these forms define professional services scope more precisely than custom agreements and reduce post-project disputes over what you were hired to do.

Protect Your Firm Through Subconsultant Controls

Require all subconsultants to carry their own professional liability insurance and provide proof before they begin work, because your firm bears vicarious liability for their negligence unless indemnification and insurance provisions protect you. Conduct a thorough risk assessment before project kickoff to identify site hazards, structural feasibility concerns, environmental factors, and material availability issues that could affect constructibility and trigger claims later. This assessment should produce a written document that gets shared with the owner and contractor so expectations align about known risks and your firm’s role in addressing them.

Final Thoughts

Engineering professional liability claims surface months or years after project completion, often triggered by field conditions your firm never anticipated or subconsultant errors you missed during prequalification. Redesign costs mount quickly, contractors file settlement demands, and your firm’s reputation suffers in ways that affect future work. The firms that avoid catastrophic claims implement peer reviews before documents leave the office, maintain detailed submittal logs that create an evidence trail, and require subconsultants to carry insurance with documented risk assessments before project kickoff.

Engineering professional liability coverage fills the gap that standard business insurance leaves open, protecting your firm against redesign costs, rework expenses, project delays, and the extended overhead allocations that emerge when claims drag on for years. Your general liability policy won’t respond to design errors, specification failures, or construction administration oversights, but professional liability does. The right coverage limit depends on your project size, complexity, and contractual obligations to clients, though most firms find that base limits plus excess coverage for severe claims provide adequate protection.

We at Tower Insurance Associates, Inc. work with engineering firms to align professional liability coverage with real project risks and contractual requirements. As an independent agency representing multiple top-rated carriers, we identify tailored coverage and competitive pricing while providing personalized service and claims advocacy when disputes arise. Contact Tower Insurance Associates, Inc. to review your current coverage and identify gaps that could expose your firm to costly claims.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.