Directors and officers in California face mounting legal and financial exposure. From shareholder disputes to regulatory investigations, the risks are real and costly.

At Tower Insurance Associates, Inc., we help California business leaders understand how a D&O policy protects their personal assets and company finances. This guide walks you through coverage options, risk assessment, and how to select the right protection for your firm.

What D&O Insurance Actually Covers

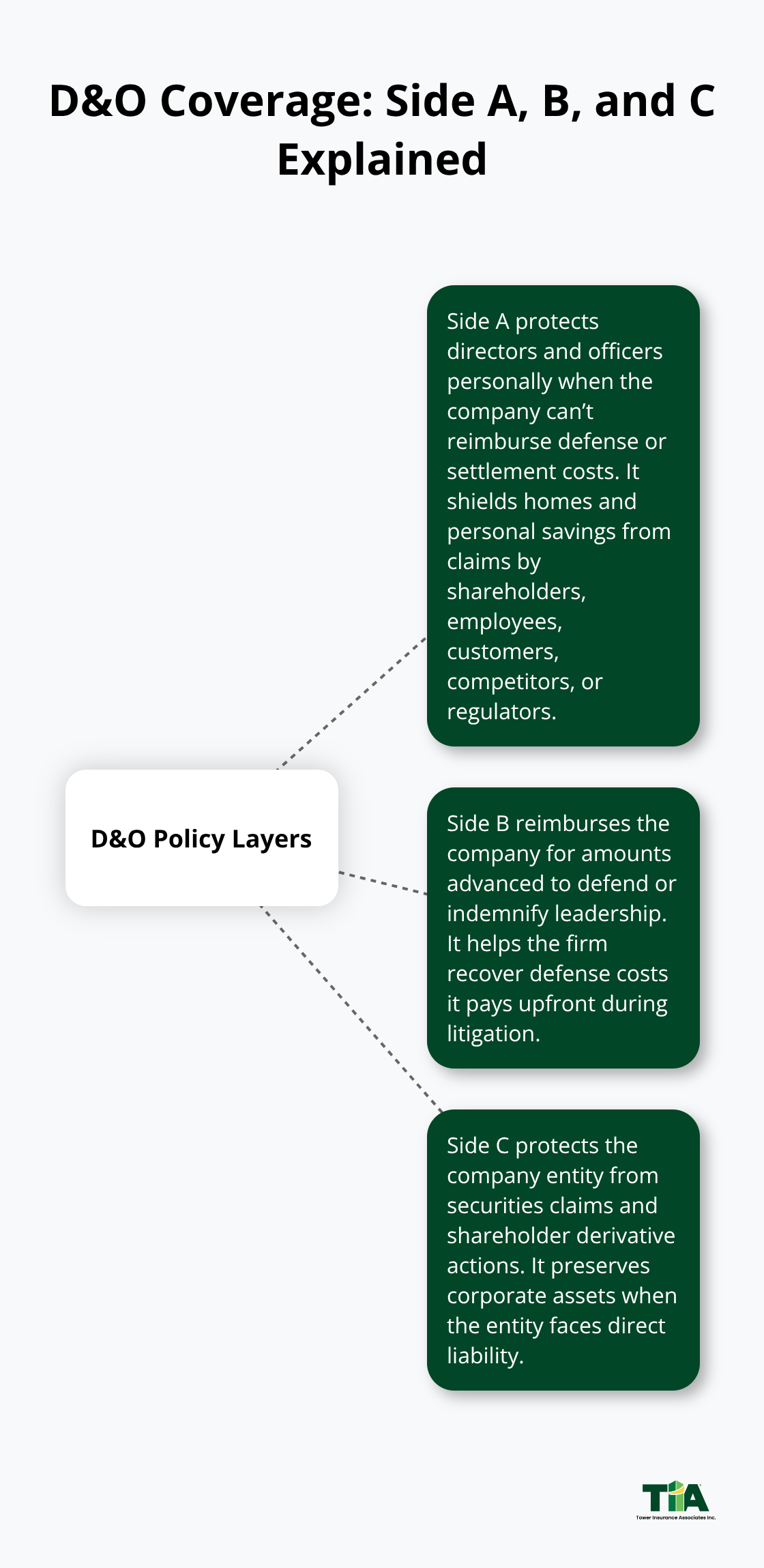

D&O insurance protects two distinct groups with separate coverage mechanisms. Side A covers directors and officers personally when the company cannot or will not reimburse their defense costs and damages, shielding their personal assets from lawsuits filed by shareholders, employees, customers, competitors, and regulators. Side B reimburses the company for amounts it pays on behalf of directors and officers as indemnification, covering defense costs the firm advances during litigation.

Side C protects the company itself from securities claims and shareholder derivative actions, preserving corporate assets when the entity faces direct liability.

How Claims Hit California Leadership

California courts see shareholder derivative suits increase steadily, with claims often centered on alleged breaches of fiduciary duty, mismanagement, and inadequate board oversight. Defense costs alone in these cases frequently exceed $1 million for mid-size firms, making this coverage essential for protecting both leadership and balance sheets. Terminated employees file claims alleging wrongful termination and breach of fiduciary duty, sometimes naming individual board members alongside the company. Shareholders launch derivative actions claiming the board failed to monitor cybersecurity risks adequately-the Boeing 737 Max derivative settlement reached $237.5 million, establishing that courts take Caremark-duty oversight claims seriously. Contract disputes with major vendors occasionally escalate into claims against officers for alleged misrepresentation or breach of fiduciary duty during negotiations.

Why California Multiplies Leadership Risk

California’s regulatory environment and litigious culture create exposure levels higher than most states. The state’s gender-diversity mandate for public company boards (enacted in 2018) and its underrepresented-communities law (passed in 2020) remain enforceable, generating governance-related claims when boards fall out of compliance. Nasdaq’s comply-or-explain diversity guidelines, approved by the SEC in 2021, have further intensified board accountability expectations across California-based firms. Cybersecurity breaches represent another acute exposure-the SEC has brought enforcement actions against California technology firms for inadequate disclosure of cyber incidents, with directors facing personal liability for negligent oversight. Employment practices claims against California leadership have grown substantially, particularly regarding sexual misconduct and hostile workplace allegations, as evidenced by high-profile settlements at companies like L Brands.

Growth-Stage Companies and Insurance Requirements

Growth-stage companies raise venture capital in California at exceptional rates, and investors now routinely require proof of D&O coverage before funding rounds, making this insurance a practical prerequisite for scaling businesses. Real-world exposure data shows that even private California firms with $50 million in revenue typically spend $25,000 to $45,000 annually on D&O premiums, reflecting the genuine frequency and severity of claims in the state. Activist investors have filed suits challenging board decisions on compensation, strategic direction, and capital allocation, with private California companies now facing this risk as PE and VC ownership structures evolve. Regulatory investigations by the SEC and California state agencies trigger defense-cost exposure that D&O policies commonly cover, including expenses for legal counsel and expert witnesses.

The combination of activist shareholders, aggressive plaintiff attorneys, and evolving state and federal regulations means California directors and officers operate in an environment where claims aren’t hypothetical-they’re a foreseeable cost of doing business. Understanding what your policy covers is only the first step; selecting the right coverage structure for your firm’s specific risk profile requires a closer look at the protection levels available.

How D&O Coverage Actually Protects California Leaders

California companies need to understand the three distinct protection layers within a D&O policy because each covers different exposure and different parties. Side A shields directors and officers personally when the company cannot reimburse their legal defense or settlement costs, protecting their homes and personal savings from claims filed by shareholders, employees, or regulators. This layer matters most when company finances deteriorate or insolvency looms-situations where corporate indemnification becomes impossible. Side B reimburses the company for amounts it advances to defend or indemnify its leadership, covering the defense costs firms typically pay upfront before any settlement or judgment. Side C protects the company entity itself from securities claims and shareholder derivative actions, preserving the corporate balance sheet when the firm faces direct liability. Most California private companies with $50 million in revenue allocate $25,000 to $45,000 annually across these three sides, with the distribution depending on ownership structure and growth stage. Public companies typically weight Side C more heavily due to securities litigation exposure, while growth-stage private firms often prioritize Side A to attract and retain qualified board members who fear personal liability.

Align Coverage Limits to Your Actual Risk Profile

The coverage limits you select should match your specific risk profile, not industry averages. A California technology firm facing cybersecurity oversight claims needs different Side A limits than a manufacturing company defending employment practices disputes. Most private California firms select limits between $1 million and $5 million, but this range reflects guesswork rather than risk analysis. Examine three concrete factors to determine your limits: the size of contracts your executives negotiate, the number of shareholders or investors who could file derivative suits, and the regulatory jurisdiction intensity in your industry. A firm with major government contracts faces higher SEC and federal agency investigation costs, justifying higher defense-cost coverage. A company preparing for acquisition or IPO needs robust Side C coverage because post-closing litigation frequently targets purchase price adjustments and disclosure accuracy.

Add Endorsements Where Standard Policies Fall Short

Additional endorsements extend core protection where standard policies create gaps. Employment practices liability endorsements add coverage for wrongful termination and harassment claims that standard D&O excludes, critical for California firms given the state’s active employment litigation environment. Fiduciary liability endorsements protect plan administrators from ERISA violations, relevant if your company sponsors retirement plans with significant assets. Crime coverage endorsements address employee theft and fraud, separate from standard D&O exclusions for intentional misconduct.

Select Deductibles Based on Cash Reserves

Deductibles in California D&O policies range from $10,000 to $250,000, and selecting the right level directly impacts your annual premium. Evaluate deductibles based on cash reserves rather than revenue percentage. A firm with $2 million in liquid reserves should not select a $100,000 deductible because a single claim could exhaust that cushion before insurance responds. Instead, try a deductible your company can absorb without disrupting operations-typically $25,000 to $50,000 for mid-size private firms. Higher deductibles reduce premiums by 15 to 25 percent, but only if your balance sheet can absorb the out-of-pocket exposure. California’s regulatory intensity means claims frequency is genuine, not theoretical, making the deductible decision financially significant over a five-year policy period. Carriers weight deductible selection heavily in underwriting because it signals your financial stability and risk awareness. A firm that selects a low deductible despite weak cash reserves appears to lack financial discipline, potentially triggering higher premiums or coverage restrictions from underwriters.

Once you understand how coverage layers and deductibles work, the next step involves comparing what different carriers actually offer and how to work with an agent who knows California’s specific business environment.

Selecting the Right D&O Policy for Your Firm

Map Your Actual Claims Exposure

Start by mapping your actual claims exposure rather than relying on industry benchmarks. California firms commonly waste money purchasing coverage that doesn’t match their specific risk profile, then discover gaps when claims arrive. Examine three concrete exposure drivers: your company’s revenue and asset base, the regulatory intensity of your industry, and your ownership structure. A $50 million revenue firm in technology faces substantially different cybersecurity oversight claims than a $50 million manufacturing company defending employment practices disputes. Technology firms need robust Side A protection because SEC enforcement actions against officers for inadequate cyber disclosures have accelerated, with First American and Pearson facing agency action. Manufacturing firms operating in California need stronger employment practices endorsements given the state’s aggressive wage-and-hour enforcement and sexual misconduct litigation trends. Real estate and construction companies face contract-related officer liability claims from vendors and subcontractors that don’t appear in other industries.

Set Coverage Limits Based on Actual Risk

Once you identify your industry’s actual claim drivers, your coverage limits become clearer. Most private California firms select $1 million to $5 million in limits, but this range reflects default thinking, not risk analysis. A firm preparing for acquisition needs substantially higher Side C limits because post-closing litigation over purchase price adjustments and disclosure accuracy occurs in roughly 40 percent of deals. A company with multiple institutional investors should weight Side A coverage higher because venture capital and private equity investors file derivative suits when exits disappoint, and defense costs can exceed $500,000 before any settlement. Growth-stage companies raising capital should verify that carriers will maintain coverage through acquisition or IPO, since some insurers impose blackout periods or refuse to cover post-closing claims.

Evaluate Carriers Beyond Ratings and Quotes

Comparing carriers requires moving beyond AM Best ratings and premium quotes to evaluate actual claims-handling practices and policy language specifics. Contact three to five carriers directly rather than relying on broker summaries, because subtle policy language differences create enormous coverage gaps. Ask each carrier specifically how they handle defense-cost advancement, whether they require consent before settling claims, and whether they cover SEC investigations at the same level as shareholder derivative suits. Some carriers cover SEC defense costs at 100 percent while others impose sublimits, a distinction that matters when federal investigations run $750,000 to $2 million. Request sample policies from each carrier and have your employment counsel review the employment practices endorsement language, since policy definitions of wrongful termination vary significantly between insurers.

Partner with an Independent Agent for Claims Advocacy

An independent agent relationship matters most during claims because the agent advocates for you with the carrier, negotiates defense counsel selections, and monitors billing to prevent cost overruns. Carriers shift claims handling burden to policyholders who lack representation, so the agent becomes your practical leverage when disputes arise over coverage or defense strategy. Ask potential agents directly how many D&O claims they’ve managed in California over the past three years and whether they’ve successfully negotiated coverage for claims the carrier initially denied. Agents without claims experience often lack credibility with underwriters, which translates to weaker coverage terms and higher premiums. An independent agent can source tailored D&O Insurance USA coverage, source quotes across the market, and eliminate the need to contact insurers individually while providing personalized service and claims advocacy.

Final Thoughts

D&O policy California firms need reflects three core realities: California’s regulatory intensity creates genuine claims frequency, coverage limits must match your specific risk profile rather than industry defaults, and the agent relationship matters most when claims arrive. The protection you select today determines whether your leadership team and balance sheet survive tomorrow’s litigation. A $50 million revenue firm spending $25,000 to $45,000 annually on D&O coverage funds a practical necessity in a state where shareholder derivative suits, employment practices claims, and regulatory investigations happen regularly, not hypothetically.

Start by mapping your actual claims exposure based on your industry, revenue size, and ownership structure rather than accepting industry benchmarks. Request sample policies from three to five carriers and have your counsel review the employment practices endorsement language, since policy definitions vary significantly and create coverage gaps when claims arrive. Evaluate carriers based on their actual claims-handling practices and defense-cost advancement policies, not just premium quotes and ratings.

We at Tower Insurance Associates, Inc. represent multiple top-rated carriers and provide personalized service and claims advocacy, helping you find tailored D&O coverage while acting as a trusted local adviser. Our team understands California’s specific business environment and can source competitive quotes across the market without requiring you to contact insurers individually. Contact Tower Insurance Associates, Inc. to discuss your D&O protection needs and secure coverage that matches your firm’s risk profile.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.