Cyberattacks against California small businesses have increased 38% over the past two years, with the average breach costing affected companies $200,000 or more. At Tower Insurance Associates, Inc., we’ve seen firsthand how unprepared many small business owners are for these threats.

The right cyber liability coverage can be the difference between recovering quickly and facing financial ruin. This guide walks you through assessing your actual risk and finding the protection that fits your business.

What Threats Are Actually Hitting California Small Businesses

Phishing and Social Engineering Lead the Attack

Phishing and social engineering attacks dominate the threat landscape for California small businesses, and they’re far more effective than most owners realize. About 43% of California small businesses reported a cyberattack in the past year, yet many operators still believe their size makes them invisible to attackers. That’s a dangerous misconception. Threat actors specifically target small businesses because they typically have fewer security defenses and less monitoring than larger enterprises.

Why Small Businesses Attract Attackers

The average cost of a California small business data breach can be financially ruinous. Beyond the immediate financial hit, ransomware attacks have surged in frequency and sophistication. These incidents lock your files and demand payment, forcing you to choose between paying extortionists or losing access to critical business data. Malware, business email compromise, and credential theft round out the most common attack vectors targeting your industry.

The Hidden Costs of a Breach Extend Far Beyond Direct Losses

When a breach occurs, the financial damage spreads across multiple categories that most owners don’t anticipate. Notification costs, credit monitoring for affected customers, forensic investigations, legal fees, and regulatory penalties all accumulate rapidly. California’s strict privacy laws amplify these costs significantly. Beyond the dollars, customer trust evaporates quickly after a breach, and rebuilding reputation takes months or years. Your competitors gain an advantage while you manage the fallout.

Regulatory Obligations Add Urgency

Compliance requirements under California’s Consumer Privacy Act and California Privacy Rights Act mean you must notify customers, law enforcement, and regulators within specific timeframes. Failure to comply triggers additional penalties on top of the breach itself. This regulatory burden makes cyber insurance not just financially prudent but operationally necessary for any California business handling customer data. Understanding your actual risk exposure requires a closer look at your specific operations and security posture.

Sizing Up Your Real Cyber Exposure

Map Your Data and Identify What Attackers Want

The first step toward choosing appropriate coverage is understanding exactly what data your business holds and how attackers could exploit it. Most California small business owners drastically underestimate their exposure because they focus only on customer information, overlooking employee records, payment processing systems, vendor credentials, and intellectual property stored on local devices or cloud services. Start by documenting every data type your operations touch: personally identifiable information, payment card data, health records if applicable, and proprietary business information. Next, map where that data lives-on employee laptops, in email systems, on mobile devices, or with third-party vendors. This inventory becomes your foundation for assessing risk.

The FCC’s Small Biz Cyber Planner 2.0 helps businesses conduct this basic data mapping exercise and identify security gaps they didn’t know existed. The gaps typically cluster around unencrypted customer data, weak password practices across teams, and unsecured Wi-Fi networks. For California businesses specifically, you must also consider which of your data types trigger compliance obligations under the California Consumer Privacy Act and California Privacy Rights Act-this determines your regulatory exposure and influences the coverage limits you’ll actually need.

Evaluate Your Current Security Controls Against Industry Standards

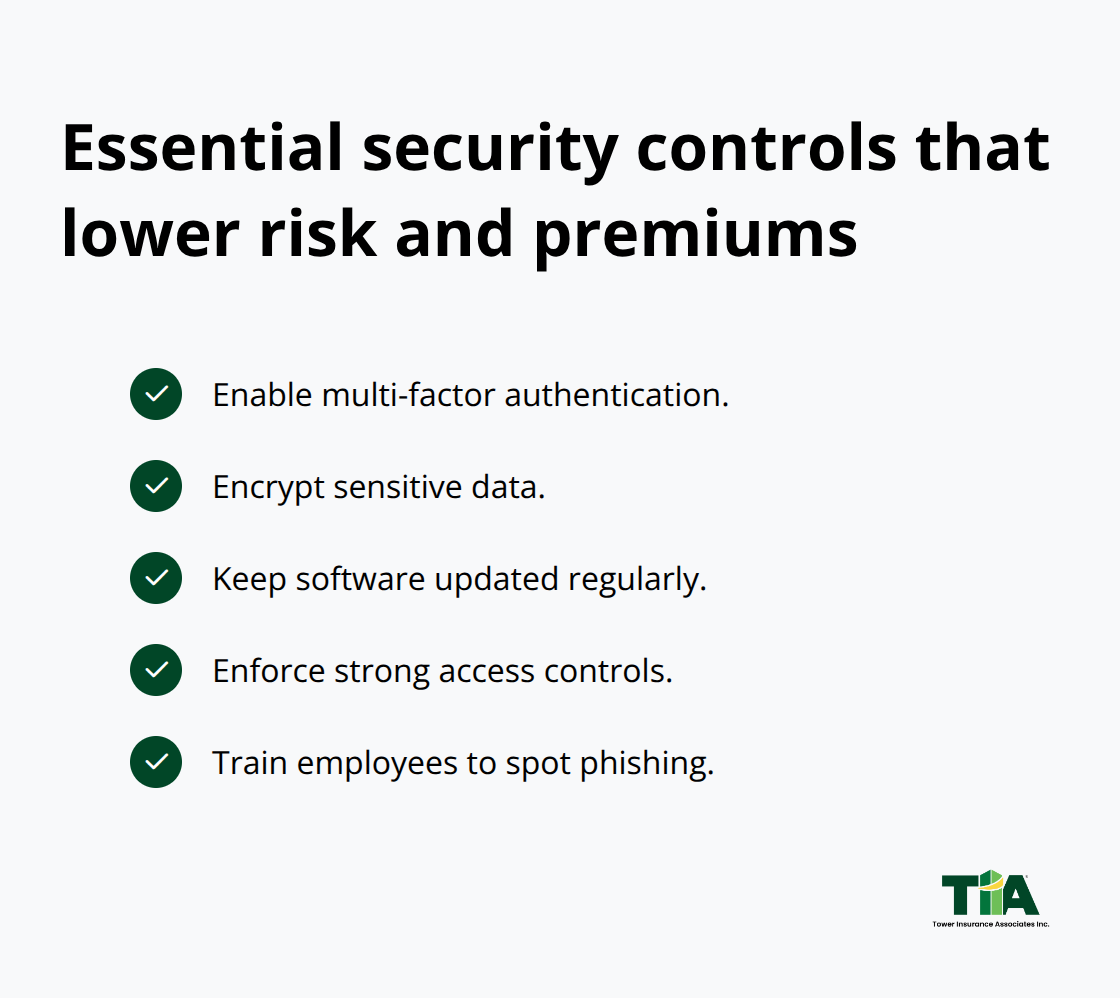

Your industry and operational structure directly shape your cyber risk profile in ways that generic risk assessments often miss. Retail businesses handling credit cards face different threats than service firms storing client contracts, yet both need coverage tailored to their actual exposure. The FCC recommends that small businesses implement multi-factor authentication, encryption for sensitive data, regular software updates, strong access controls, and ongoing employee training on phishing-these controls meaningfully reduce your breach likelihood and typically lower insurance premiums.

If your team lacks dedicated cybersecurity staff, external security partnerships become essential; roughly 43% of cyberattacks target small and medium-sized businesses specifically because of this resource gap. Before selecting a cyber policy, conduct a security assessment that honestly evaluates your current controls against these standards. This assessment informs both your coverage needs and your premium costs, since insurers price policies based on your security maturity level.

Connect Your Risk Profile to Coverage and Premium Costs

Businesses with robust controls and minimal data exposure typically qualify for lower premiums, while those with weak defenses face higher rates or coverage restrictions. Working with an independent insurance professional who understands California’s regulatory environment helps you align your coverage limits and deductible choices to your actual risk profile rather than guessing at numbers that may leave you underprotected. Once you understand your exposure level, you’re ready to evaluate the specific coverage types that address your identified risks and determine which policy limits make financial sense for your operation.

What Coverage Actually Protects Your Business

First-Party and Third-Party Coverage Work Together

Cyber liability policies split into two fundamental categories: first-party coverage pays for your direct costs after a breach, while third-party coverage handles claims from customers and regulators. First-party protection covers forensic investigations, notification expenses, credit monitoring services for affected customers, legal defense, and regulatory fines-the immediate financial fallout that most owners underestimate. Third-party liability covers claims from customers alleging you failed to protect their data, as well as network security liability if your systems accidentally spread malware to clients or partners. California’s strict privacy laws amplify these third-party exposures significantly, making comprehensive first-party and third-party combinations essential rather than optional.

Understanding Policy Limits and Deductibles

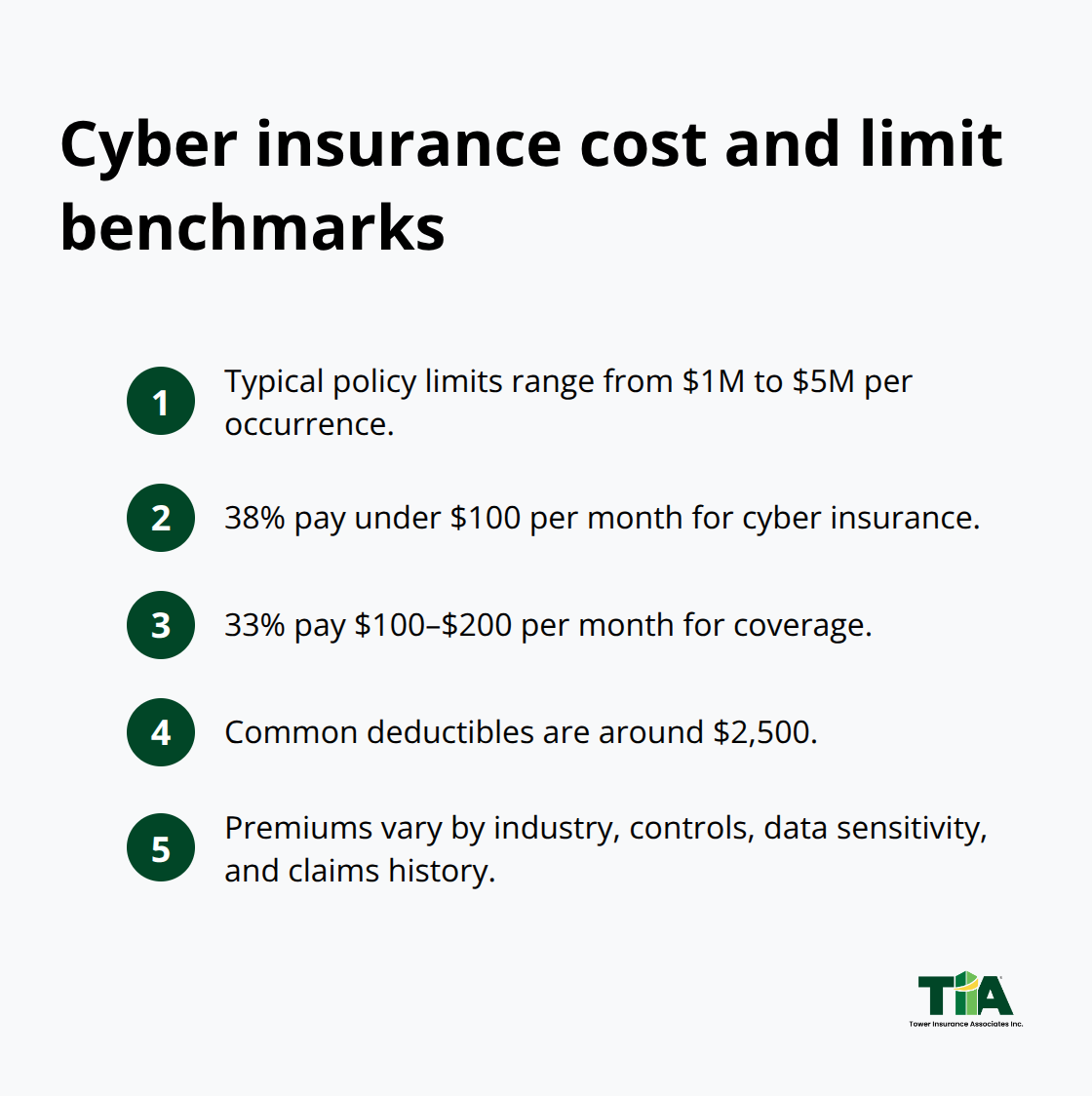

The average cost of a California small business data breach reached $9.5 million, yet most small business owners purchase policies with limits far below this figure, leaving themselves dramatically underprotected. Policy limits typically range from $1 million to $5 million per occurrence, with annual aggregate limits determining your total coverage across multiple incidents in a single year. About 38% of small businesses pay less than $100 monthly for cyber insurance, while 33% pay between $100 and $200 monthly, according to Insureon data-costs that vary based on your industry, security controls, data sensitivity, and claims history. Deductibles commonly sit around $2,500, though higher deductibles lower premiums while forcing you to absorb more out-of-pocket costs when incidents occur.

Tailoring Coverage to Your Industry and Operations

Retail and financial services businesses typically need higher limits due to payment card processing exposure, while professional service firms might prioritize technology errors and omissions coverage protecting against negligence claims. A cyber risk assessment before selecting limits reveals whether your chosen protection actually matches your exposure. Underinsurance leaves you vulnerable to the exact scenarios you’re trying to prevent, so honest evaluation of your data types and operational risks matters more than selecting the lowest premium available.

Business Interruption and Ransomware Protection

Business interruption coverage reimburses lost revenue during downtime after an incident-critical protection since ransomware attacks can halt operations for days or weeks. Cyber extortion and ransomware coverage addresses ransom demands and negotiator fees, reflecting the reality that extortion scenarios have nearly doubled in frequency. These protections acknowledge that operational disruption often costs more than the direct breach response itself.

Additional Coverage Options Complete Your Strategy

Crime insurance addresses employee theft, while vendor management liability addresses third-party breaches affecting your operations. Additional coverage options like these complete a comprehensive protection strategy tailored to your specific operational risks and regulatory obligations.

Final Thoughts

Your cyber risk assessment reveals the actual threats your California small business cyber operations face, and this clarity transforms insurance from an abstract expense into a targeted financial strategy. Select coverage that reflects what you learned about your data, security controls, and regulatory obligations under California’s privacy laws. If your assessment exposed weak access controls or minimal employee training, prioritize policies that include incident response resources and security awareness support alongside traditional breach coverage.

Implement security fundamentals on one front while working with an insurance professional on the other. Multi-factor authentication, encryption for sensitive data, regular software updates, and ongoing employee training on phishing threats reduce both your breach likelihood and your insurance premiums. These controls signal to insurers that you take risk seriously, which translates directly into lower rates and better coverage terms.

Contact Tower Insurance Associates, Inc. to discuss your cyber risk profile with someone who understands California small business cyber threats and can compare policies from multiple carriers. Our team has guided California businesses through this process since 1961, representing top-rated carriers to find coverage that actually fits your operation and budget without generic recommendations that leave you underprotected.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.