Professional liability insurance protects your career and finances when clients claim you made mistakes or failed to deliver promised services. At Tower Insurance Associates, Inc., we know that California professionals face unique coverage challenges shaped by state regulations and competitive markets.

Finding the right insurance provider means understanding what coverage actually protects you, comparing policies side by side, and recognizing how California’s specific requirements affect your options. This guide walks you through the evaluation process so you can make an informed decision.

What Professional Liability Insurance Actually Covers

Professional liability insurance protects you when clients claim you made a mistake, gave bad advice, missed a deadline, or failed to deliver what you promised. The coverage pays for legal defense costs, settlements, and judgments-even if you’re found not at fault. Technical errors, project management missteps, and inadequate documentation remain the top claims drivers across architecture and engineering firms. This means the policy responds when a client alleges negligence or breach of professional duty, not just when you’ve clearly made an obvious error. For California professionals, this distinction matters because client expectations for the highest standard of care are rising, and vague contract language can expand your liability beyond what most policies cover. E&O coverage extends to misrepresentation, negligence, missed deadlines, and contract breaches-situations where the outcome might be disputed or your responsibility unclear.

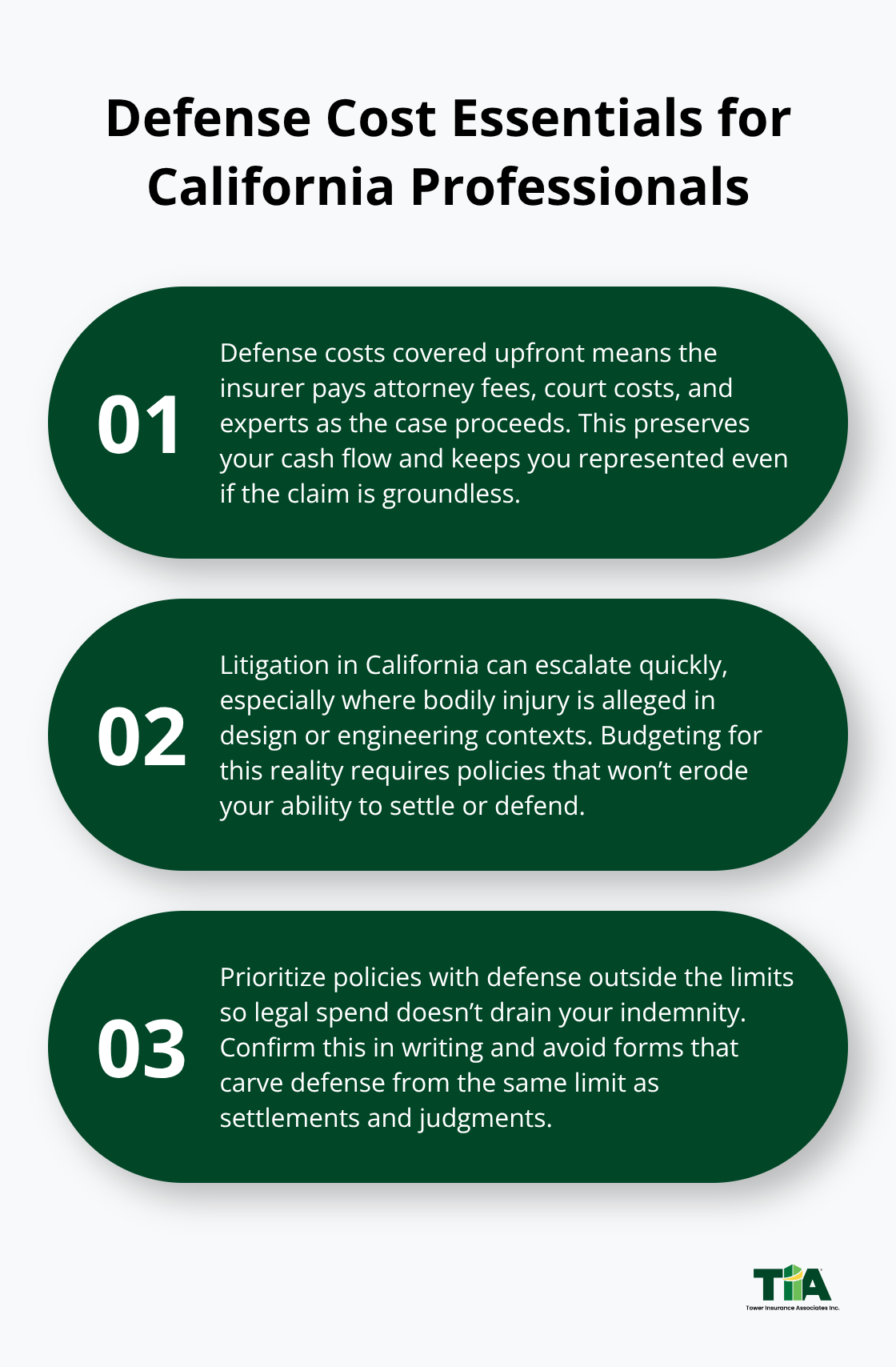

Defense Costs Come First

Many professionals assume they only receive help if they lose a claim, but solid professional liability policies cover legal defense costs upfront, regardless of the outcome. These costs include attorney fees, court expenses, and expert witness fees. The policy pays for defense before any settlement or judgment, which means you stay protected financially while your case unfolds. Litigation costs have risen significantly, particularly in states like California where bodily injury claims tied to design or engineering work can become expensive quickly. You must verify that your policy clearly states defense costs are separate from your coverage limits-not carved out of them.

Some policies reduce your indemnity coverage dollar-for-dollar as defense costs accumulate, leaving you exposed if the case drags on. California firms should verify this detail with their broker before purchasing, especially if they work on large public infrastructure or multi-family residential projects where disputes are more common.

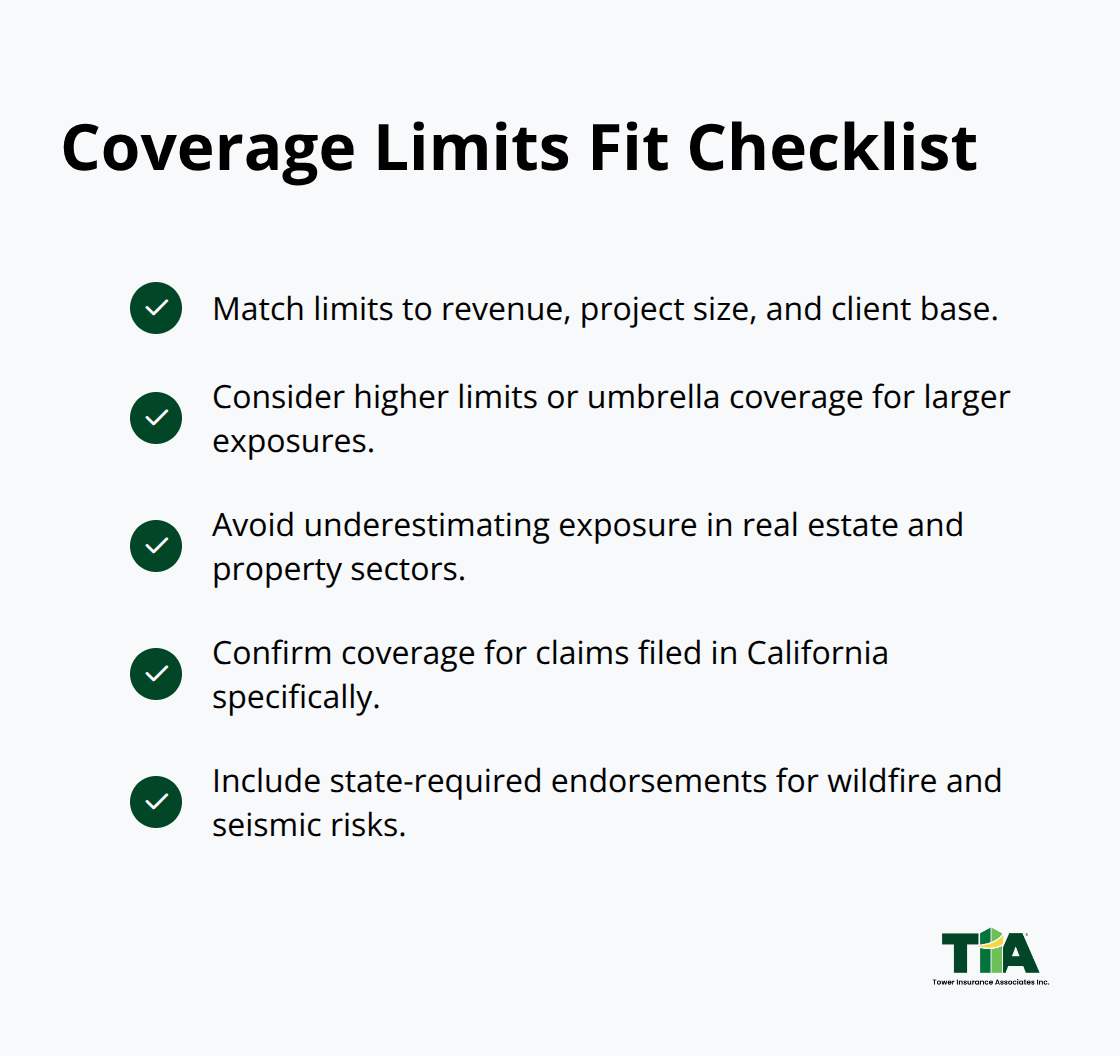

Coverage Limits Must Match Your Exposure

Your coverage limit is the maximum the insurer will pay for any single claim or all claims combined during the policy period. Larger projects drive higher exposure, so firms handling bigger contracts need higher limits to avoid under-insurance. A $1 million limit may sound adequate, but jury awards are rising in California and other states, with bodily injury claims leading to the largest losses. You won’t receive excessive awards from a $1 million policy, but higher limits and umbrella coverage protect you if a claim exceeds your primary policy. Evaluate your revenue, project size, and client base to set appropriate limits. Real estate consultants, home inspectors, and property management professionals often underestimate their exposure and purchase limits that don’t match their actual risk. California professionals should also confirm that their policy covers claims filed in California specifically and includes any state-required endorsements for local risks like wildfire or seismic damage.

Verify What Your Policy Actually Covers

Not all professional liability policies cover the same risks, and gaps in coverage can leave you exposed when you need protection most. Some policies exclude certain claim types (such as sexual misconduct allegations or licensing-board complaints) unless you add them as endorsements. You should request a detailed policy summary that lists exactly what the insurer covers and what it excludes. Ask your broker whether the policy covers claims you file after the policy period ends (tail coverage) and how long that protection lasts. These details separate adequate coverage from coverage that fails you when a claim arrives. California firms working in high-risk areas like residential design, geotechnical services, or multi-family residential projects face elevated underwriting scrutiny, so clear policy language becomes even more important.

How to Evaluate Insurance Providers

Comparing professional liability policies requires more than shopping for the lowest price. You need to assess whether an insurer understands your profession, handles claims efficiently, and offers coverage that actually protects your specific exposure. Start by requesting detailed policy summaries from at least three providers, then place them side by side to compare coverage limits, deductibles, exclusions, and what triggers a claim. Many professionals focus only on the premium, but a cheaper policy with gaps in coverage or slow claims processing will cost far more when you need it.

Price Alone Won’t Protect You

According to the 2025 Professional Liability Trends report from NSPE, AIA, and ACEC, premiums for architecture and engineering firms are driven mainly by annual billings and claims history, with rates remaining relatively stable even as project sizes grow. This means you have room to shop for better coverage terms rather than accepting whatever price appears first. Look specifically at whether the insurer offers separate defense limits, which protect your indemnity coverage by allocating dedicated funds for legal defense costs. This detail matters enormously because litigation costs in California have risen sharply, especially for claims involving bodily injury or large public infrastructure projects.

Financial Strength and Claims Responsiveness Matter Most

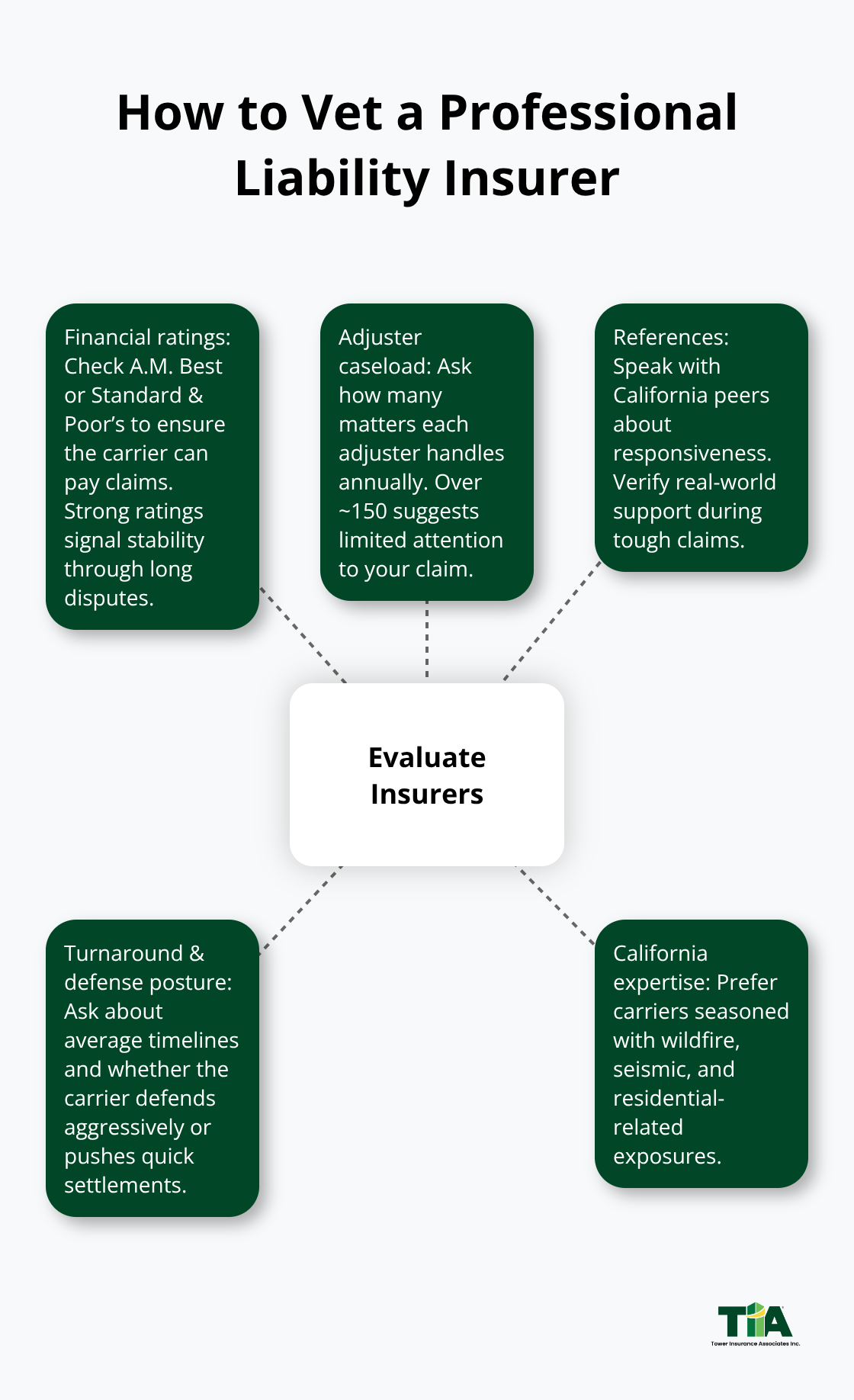

Financial strength and claims responsiveness separate insurers that will back you when disputes arise from those that disappear when you need help. Verify the insurer’s financial rating through A.M. Best or Standard & Poor’s to confirm they can actually pay claims. Then ask how many claims each adjuster handles on average; if the answer exceeds 150 matters per year, the insurer is likely stretched too thin to provide thoughtful advocacy. Request references from other California professionals in your field and ask specifically about claim turnaround times and whether the insurer defended them aggressively or pressured them to settle quickly.

Look for Proven Experience in Your Field

Customer reviews on industry sites and professional association forums reveal patterns that individual conversations may miss, particularly complaints about slow response times or denials on borderline claims. Check whether the insurer has demonstrated experience with California-specific risks like wildfire exposure, seismic damage, or cannabis-related coverage if relevant to your work. Not all insurers understand A/E work equally well, so prioritize those with proven track records in professional liability for your specific profession rather than generalist carriers that treat all businesses the same.

Assess How the Insurer Treats You

An insurer’s willingness to provide clear policy language, accessible coverage definitions, and proactive risk management resources indicates they view you as a partner rather than just a premium. At Tower Insurance Associates, Inc., we represent multiple top-rated carriers, which means we can match you with an insurer whose underwriting expertise aligns with your actual risk profile instead of forcing you into a one-size-fits-all program. The next step involves understanding which specific coverage features matter most for California professionals and how state regulations shape your options.

What Makes California Coverage Different

California’s regulatory environment and risk landscape create specific coverage demands that national insurers often mishandle. The 2025 Professional Liability Trends report from NSPE, AIA, and ACEC identifies residential and condominium projects, geotechnical services, large public infrastructure, multi-family residential work, and condominium condition assessments as underwriting red flags in California. Carriers apply stricter scrutiny and higher premiums to these project types, so your insurer must understand California’s unique exposure rather than applying generic national standards.

Cannabis Coverage and Emerging Risks

Cannabis coverage is explicitly required for many California design and engineering firms facing liability from cannabis-related projects, yet most national carriers either exclude this coverage entirely or charge premiums that make it unaffordable. Wildfire and seismic risk also shape coverage availability in California, with some insurers declining to cover firms in high-risk zones or adding climate-related exclusions that leave you exposed when a project involves wildfire-prone areas or seismic design considerations. Your policy must address these California-specific risks directly through clear endorsements and coverage language rather than hoping a national carrier will respond when a claim arises from wildfire or seismic damage.

Market Competition and Pricing Reality

Pricing in California reflects these elevated risks, and the market remains competitive overall because new entrants are entering after some carriers exit. However, not all insurers understand A/E work equally well, so you should compare both price and insurer expertise rather than selecting the lowest quote blindly. Verify that your insurer has handled claims from California professionals working on the exact project types you pursue, then confirm they offer project limits that let you allocate specific coverage to individual projects to meet client requirements without exhausting your entire policy.

Extended Coverage and Project Limits

Extended reporting period options of up to five years help capture claims on older or completed projects, which matters in California where construction disputes often surface years after project completion. As average project size increases in California, scale your coverage limits accordingly to avoid under-insurance on larger, higher-stakes projects. Separate defense limits preserve indemnity coverage by allocating dedicated funds for legal defense costs, protecting you when litigation expenses mount during complex disputes.

Finding the Right Carrier Match

Tower Insurance Associates, Inc. represents multiple top-rated carriers with proven experience in California professional liability. This allows us to match you with an insurer whose underwriting expertise and coverage terms align with California’s specific regulatory environment and market conditions rather than forcing you into a national program designed for other states.

Final Thoughts

Evaluating professional liability insurance providers in California requires you to balance price against coverage quality, financial stability, and claims responsiveness. The best policy matches your actual risk profile rather than offering the lowest premium with gaps that leave you exposed when disputes arise. Your insurer must understand California’s specific regulatory environment, including elevated risks from residential projects, geotechnical work, and multi-family residential exposure, and should offer separate defense limits to protect your indemnity coverage as litigation costs mount.

California professional liability reviews consistently show that carriers with proven experience in your field outperform generalist insurers that apply national standards to state-specific risks. Verify financial strength through A.M. Best ratings, confirm that adjusters handle manageable caseloads, and request references from other California professionals in your industry. Ask whether the insurer covers cannabis-related projects, wildfire exposure, and seismic design considerations if those risks apply to your work.

The next step is requesting detailed policy summaries from multiple carriers and comparing coverage limits, deductibles, exclusions, and what triggers a claim. Tower Insurance Associates, Inc. represents multiple top-rated carriers and can match you with an insurer whose expertise aligns with California’s unique professional liability landscape. Contact us to discuss your specific exposure and receive quotes that reflect your actual risk rather than generic industry assumptions.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.