A single mistake in handling California professional liability claims can cost your practice thousands of dollars and damage your reputation. At Tower Insurance Associates, Inc., we’ve seen professionals lose cases simply because they didn’t know the right steps to take when a claim arrived.

This guide walks you through the entire process, from the moment you report a claim to your insurer through to resolution. You’ll learn exactly what documentation matters, which mistakes to avoid, and how to work effectively with adjusters and legal teams.

What Professional Liability Actually Covers in California

The Foundation of Professional Liability Coverage

Professional liability coverage protects your practice when a client claims you failed to meet the standard of care in your field. In California, this means the coverage responds when your professional actions or omissions cause financial harm to a client. The standard of care is typically determined by a combination of factors, including the prevailing practices within your profession. If you’re an accountant, that standard differs from what a lawyer or architect faces. The coverage pays for your legal defense, settlement costs, and judgments up to your policy limits.

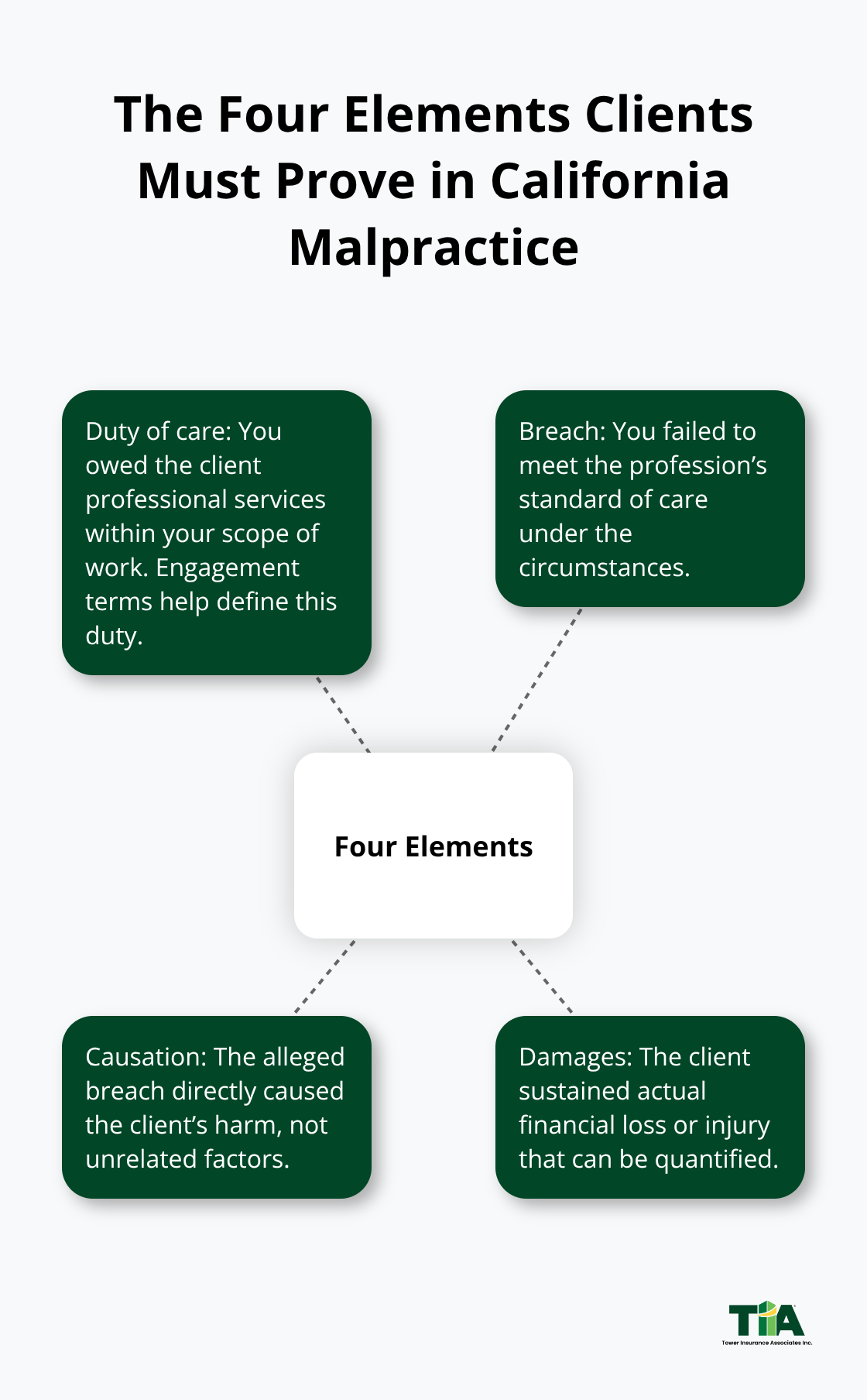

The Four Elements Clients Must Prove

California defines professional malpractice as the failure by licensed professionals to meet the standard of care, causing harm. To win a claim against you, a client must prove four elements: duty of care (you owed them professional services), breach (you failed to meet the standard), causation (your breach directly caused harm), and damages (they suffered actual financial loss or injury). Without professional liability insurance, you personally cover these defense costs and settlements, which can exceed hundreds of thousands of dollars.

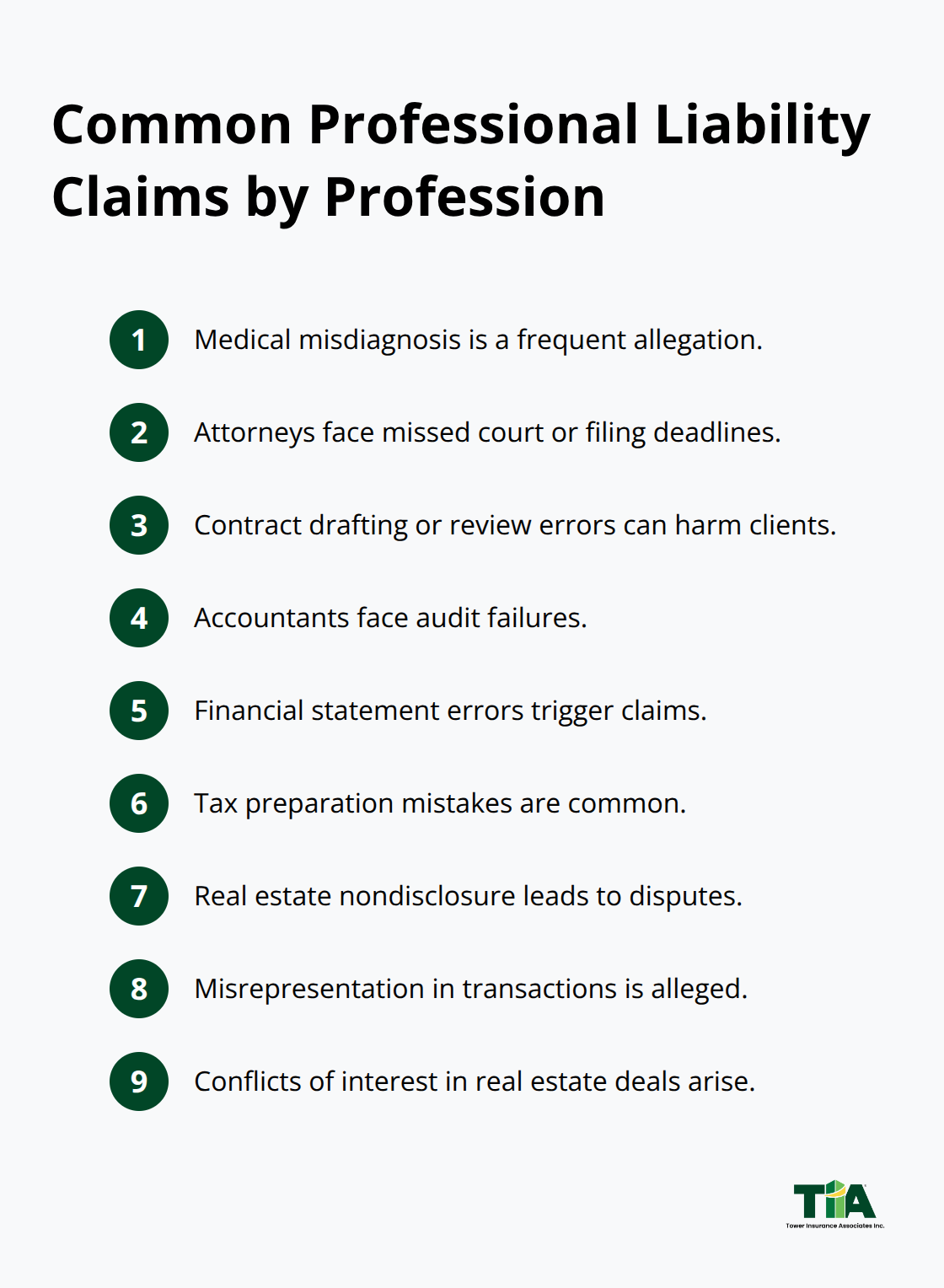

Common Claims Across Professional Fields

Medical misdiagnosis, missed court deadlines, and incorrect tax filings represent the most common malpractice claims. Lawyers face claims when they miss filing deadlines or make contract errors that harm clients. Accountants defend claims involving audit failures, financial statement errors, and tax preparation mistakes. Real estate professionals face claims for nondisclosure, misrepresentation, and conflicts of interest in both residential and commercial transactions.

The Rising Cost of Large Claims

Large claims are accelerating across professional fields. The share of claims with indemnity payments of 1 million dollars or more has risen significantly, and claims exceeding 5 million dollars have increased even more noticeably. Social inflation and third-party litigation funding are driving these larger settlements and judgments.

Matching Your Coverage to Your Actual Exposure

Your policy must match your actual exposure. A solo practitioner handling simple tax returns needs different limits than a firm managing complex audits for multiple clients. Most policies operate on a claims-made basis, meaning a claim must be reported during the policy period when it’s made, not when the error occurred. This distinction matters enormously: an error you discover in a prior year must be reported immediately to your current insurer to qualify for coverage. Understanding these coverage mechanics now prevents costly gaps later when you report a claim to your insurer.

How to Report a Claim and What Happens Next

Contact Your Insurer Immediately

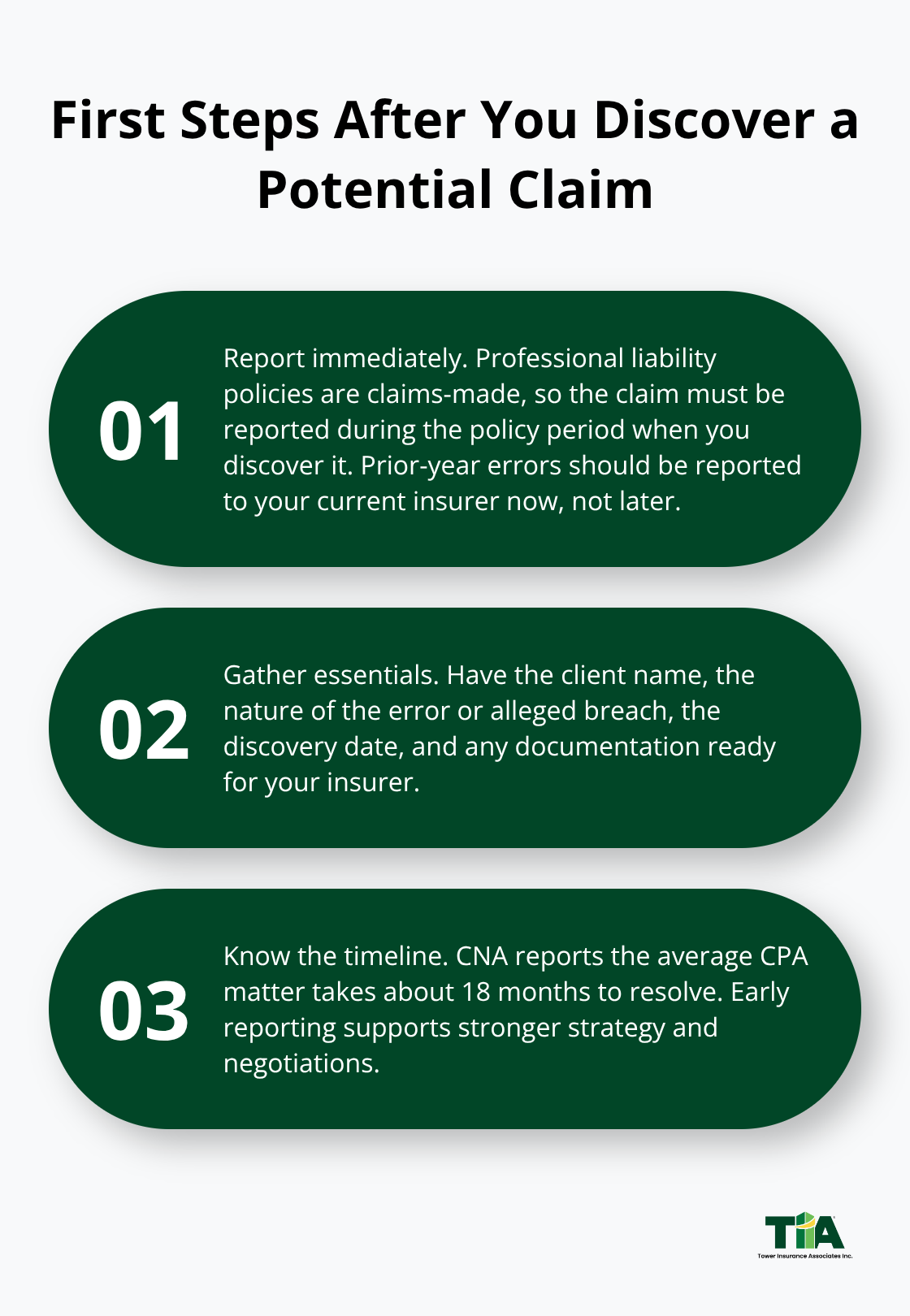

The moment you discover a potential claim, contact your insurer immediately. This is not a suggestion-it’s the single most important action you can take. Your professional liability policy operates on a claims-made basis, which means the claim must be reported during the policy period when you discover it, regardless of when the error actually occurred. An error you find in prior-year work must be reported to your current insurer now, not when the client eventually sues. Delayed reporting complicates defense strategy and settlement negotiations, and outcomes generally do not improve with time.

CNA, the underwriter of the AICPA Professional Liability Insurance Program, reports that the average CPA matter takes about 18 months to resolve. When you call your insurer, have ready the client name, the nature of the error or alleged breach, the date you discovered the problem, and any documentation you’ve already gathered.

Your Dedicated Claim Professional Becomes Your Partner

Your insurer will assign a dedicated claim professional with experience in your field. This person becomes your partner in navigating the process. Request their direct contact information and establish a communication cadence-weekly calls are standard for active claims. Ask specifically about the engagement letter from your original client work, as this document defines the scope of services you promised and establishes the standard of care that will guide your defense.

Your insurer’s defense counsel will request this letter early, along with all engagement workpapers and client communications related to the matter. Communicate openly with your defense team about the facts, your recollection of events, and any concerns you have. Your insurer requires written consent from you before settling any claim, so your input directly influences the outcome.

Gather Documentation and Evidence in Parallel

Documentation and evidence gathering happen in parallel with your insurer’s investigation. Create a filing system to organize every email, memo, spreadsheet, and file related to the engagement before the claim was reported. Arrange these chronologically so your defense team can trace your decision-making and demonstrate you followed proper procedures. Medical records, financial statements, audit workpapers, or tax returns-whatever shows your work-become critical evidence.

An expert will be engaged to evaluate whether you adhered to the standard of care in your field by reviewing these materials. If your documentation is sparse or disorganized, the expert’s assessment weakens, and settlement leverage disappears. California professional liability claims require expert testimony to establish the standard of care and explain how your actions deviated from it. Without solid documentation, your expert has little to work with.

Navigate Regulatory Inquiries and Defense Counsel Selection

Many claims also involve regulatory inquiries or licensing board investigation running simultaneously with the civil claim. Your policy may offer supplemental benefits to assist with subpoenas, depositions, or regulatory responses at little or no cost-ask your claim professional about this coverage immediately.

Your insurer will select defense counsel after vetting for experience in your specific profession and jurisdiction. Mediation often emerges as a faster, less costly resolution path than litigation, especially for mid-range claims. The entire process-from assignment through expert review to interviews with your staff and formal resolution planning-typically takes time, but your insurer’s resources and dedicated focus will substantially reduce both your stress and your financial exposure.

How to Build an Unshakeable Defense

Documentation Forms the Core of Your Defense Strategy

Documentation is your defense. The moment your insurer assigns a claim professional, you should already organize every piece of evidence related to the engagement. Your engagement letter, workpapers, email correspondence, client communications, and internal memos form the foundation of your defense strategy. An expert will review these materials to assess whether you adhered to the standard of care in your field, and sparse or disorganized documentation directly weakens that expert’s opinion. If your files show clear decision-making, proper procedures, and timely communication with the client, your defense team gains leverage in settlement negotiations. If your records are incomplete or unclear, settlement outcomes deteriorate.

The expert witness cannot reconstruct your reasoning or demonstrate adherence to professional standards without tangible evidence. Organize documents chronologically so your defense counsel can trace your work step by step. Medical records, audit workpapers, tax returns, engagement letters, email trails-every artifact matters. This is not busywork; this directly influences whether your claim settles favorably or escalates to costly litigation.

Understand Your Policy Limits and Exclusions

Your policy limits and exclusions determine your financial exposure, and many professionals misunderstand these boundaries until a claim arrives. Most professional liability policies operate on a claims-made basis with specific coverage limits per claim and aggregate limits across all claims in a policy year. If a claim exceeds your per-claim limit, you pay the difference out of pocket. Some policies exclude coverage for claims arising from dishonesty, regulatory violations, or prior known errors, so review your policy language now before you need it.

Professional liability policies can require reporting of both actual claims and potential claims. This knowledge prevents surprises when settlement discussions begin.

Avoid Common Mistakes That Derail Claims

Common mistakes that delay claims include late reporting to your insurer, failure to preserve evidence, and withholding information from your defense team. Delayed reporting complicates strategy because settlement leverage weakens over time, and regulators may have already launched investigations that now run parallel to your civil claim. Preserve all communications and files the moment you suspect a problem; do not delete emails or reorganize files after discovering a potential claim, as this appears evasive and undermines your credibility.

Finally, communicate openly and honestly with your claim professional and defense counsel about the facts, your recollection of events, and any weaknesses in your case. Attempting to hide unfavorable facts only emerges later during depositions or expert review, damaging your defense at critical moments. Your insurer requires written consent before settling any claim, so your transparency and partnership with your defense team directly shape the outcome and your firm’s financial recovery.

Final Thoughts

California professional liability claims demand immediate action, clear documentation, and partnership with your insurer. The steps outlined in this guide-reporting promptly, organizing evidence, understanding your policy, and communicating openly with your defense team-directly determine whether your claim settles favorably or escalates into costly litigation. Claims-made policies require you to report claims during the policy period when you discover them, not years later when litigation begins, and delayed reporting weakens your defense at every stage.

Beyond managing individual claims, you need coverage that matches your actual exposure. A solo accountant handling tax returns faces different risks than a firm managing complex audits, so your policy limits, exclusions, and coverage terms must align with your practice. At Tower Insurance Associates, Inc., we help California professionals find tailored coverage that protects your actual work and secures competitive pricing without sacrificing quality.

The professionals who navigate California professional liability claims with confidence prepare before a claim arrives. Review your engagement letters, strengthen your documentation practices, and confirm your policy covers your actual work so that when a claim surfaces, you know exactly what to do and who to call.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.