Your classic car represents decades of automotive history and craftsmanship. Standard auto insurance policies simply don’t account for the unique value and specialized needs these vehicles demand.

At Tower Insurance Associates, Inc., we understand that a California classic car policy requires a completely different approach than coverage for everyday vehicles. This guide walks you through the essential protections that keep your vintage investment safe.

Why Classic Cars Need Different Insurance

Agreed Value Coverage Protects Appreciation

Standard auto insurance treats all vehicles the same way: it calculates what your car is worth today, subtracts depreciation, and pays that amount if it’s totaled. For a classic car, this approach destroys value. A 1967 Chevrolet Corvette Stingray worth $85,000 loses thousands in value the moment you drive it off the lot under a standard policy.

Classic car insurance works backward from how you actually value your vehicle. Insurers use agreed value coverage, which eliminates depreciation and ensures you receive the full agreed-upon amount if your car is totaled, minus your deductible. This matters enormously because classic cars often appreciate. A well-maintained 1963 Jaguar E-Type might be worth $65,000 one year and $72,000 the next as the collector market strengthens. Agreed value coverage captures that appreciation instead of ignoring it.

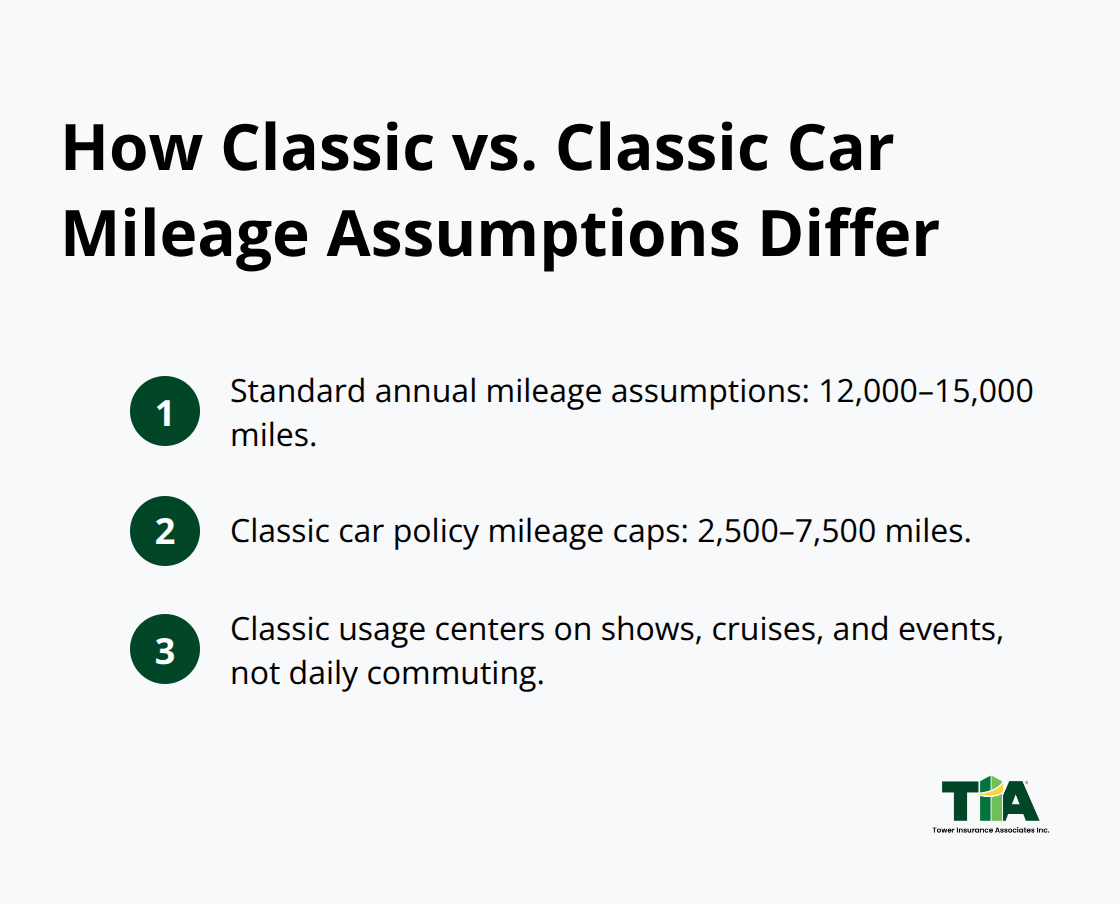

Mileage Limits Reflect How You Actually Drive

The second major difference involves how you actually drive your vehicle. Standard policies assume you commute daily, rack up 12,000 to 15,000 miles annually, and park in random places. Classic car policies impose mileage caps-typically between 2,500 and 7,500 miles per year-because these vehicles attend shows, cruises, and charity events rather than sitting in office parking lots.

You declare your expected usage upfront, and lower mileage translates to lower premiums. This structure rewards owners who treat their classics as weekend treasures rather than daily transportation. Your actual driving habits determine your rate, not arbitrary industry assumptions.

Original Parts Coverage Preserves Authenticity

The third distinction centers on repairs and parts. When your daily driver needs a new door panel, the shop installs a standard replacement. With a classic car, you might specify original factory parts instead of aftermarket substitutes, and that preference affects coverage and repair costs.

Some policies include original parts coverage, which pays the premium for authentic components rather than cheaper modern alternatives. Your 1955 Mercedes-Benz 300SL deserves a period-correct fuel pump, not a generic one that saves money but compromises authenticity and resale value. This coverage option protects both your investment and the historical integrity of your vehicle.

These three pillars-agreed value, mileage flexibility, and parts authenticity-form the foundation of proper classic car protection. Understanding how they work together helps you evaluate which coverage options align with your specific vehicle and how you plan to use it.

Essential Coverage Types for Classic Car Owners

Comprehensive and Collision Protection Form Your Foundation

Comprehensive and collision protection form the backbone of any classic car policy, but they work differently than standard auto insurance. Comprehensive covers theft, vandalism, weather damage, and animal strikes, while collision handles accidents with other vehicles or objects. For a classic car worth $50,000 or more, these protections are non-negotiable.

The real question is your deductible. Most classic car owners choose higher deductibles like $1,000 or $2,500 because they drive infrequently and store their vehicles carefully, reducing the likelihood of small claims. This choice lowers your premium substantially. If your 1972 Porsche 911 sits in a climate-controlled garage and only attends five car shows per year, a $2,500 deductible makes financial sense compared to a $250 deductible that costs significantly more in annual premiums.

Liability Coverage Protects Your Assets

Liability coverage protects you when you cause injury or property damage to others, and California requires minimum liability limits of 15/30/5 (meaning $15,000 per person, $30,000 per accident for bodily injury, and $5,000 for property damage). However, this minimum is dangerously low for a classic car owner. If your 1965 Ford Mustang causes an accident that injures someone seriously, California’s medical costs often exceed $100,000 per person.

Increasing your liability limits to 100/300/100 costs only slightly more in premium but protects your assets from lawsuits. Many classic car insurers automatically align your liability limits with your regular auto policy, which simplifies coverage and ensures consistency across all your vehicles.

Uninsured Motorist Protection Covers the Gaps

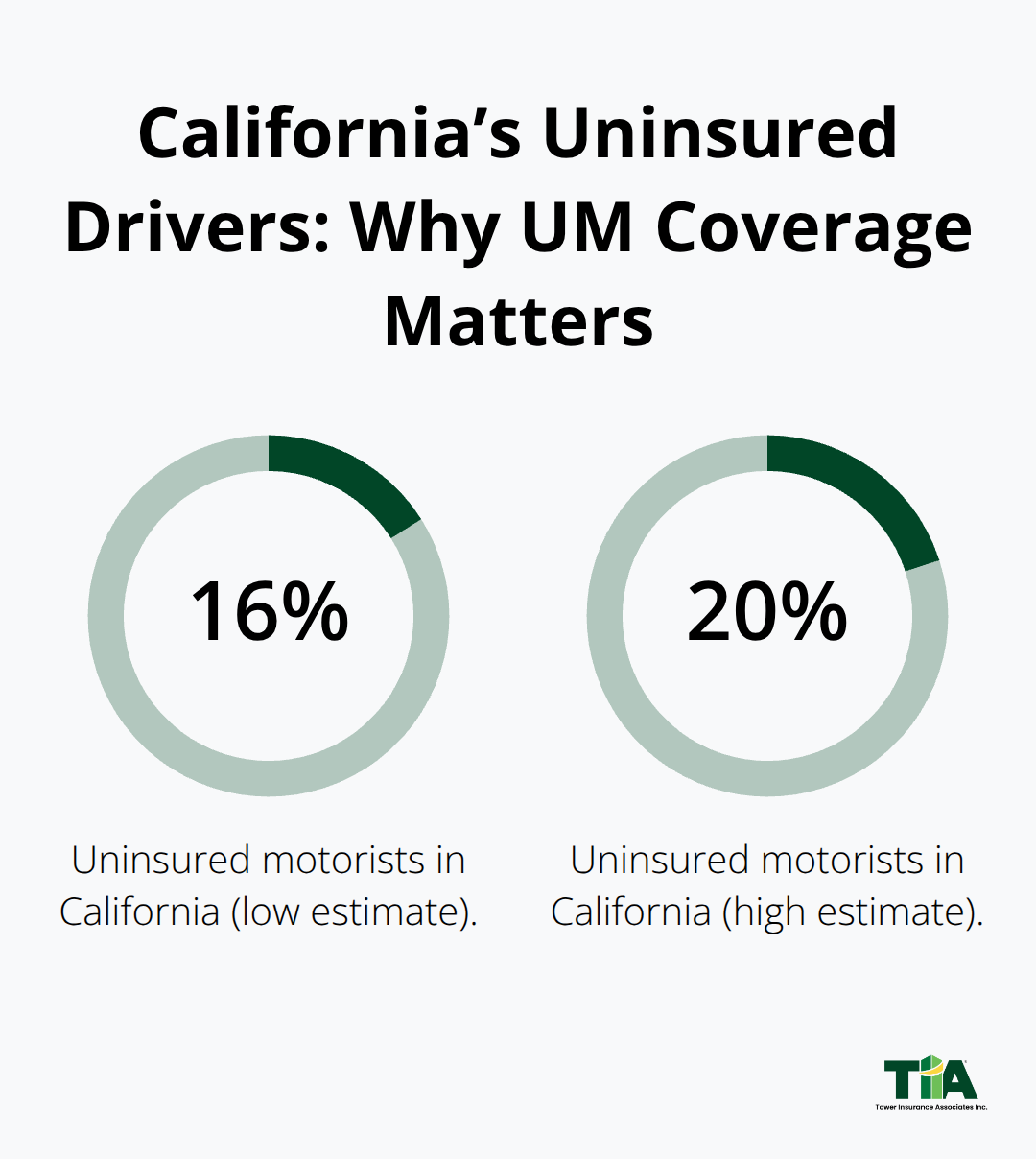

Uninsured and underinsured motorist protection covers you if an uninsured driver hits your classic car or if their insurance limits are too low to cover your damages. California has a high uninsured rate of 16-20%, making this coverage essential. If an uninsured driver totals your 1959 Chevrolet Corvette valued at $95,000, uninsured motorist property damage coverage pays the agreed value minus your deductible, not some depreciated amount.

This protection directly complements your agreed value coverage by ensuring you receive full value regardless of who caused the damage. Beyond these three core protections, classic car policies often include additional options that address the specific risks your vintage vehicle faces. Understanding what each coverage type does helps you build a policy that matches both your vehicle’s value and your actual driving patterns.

How to Protect Your Classic Car Investment

Document Your Vehicle’s Condition and Value

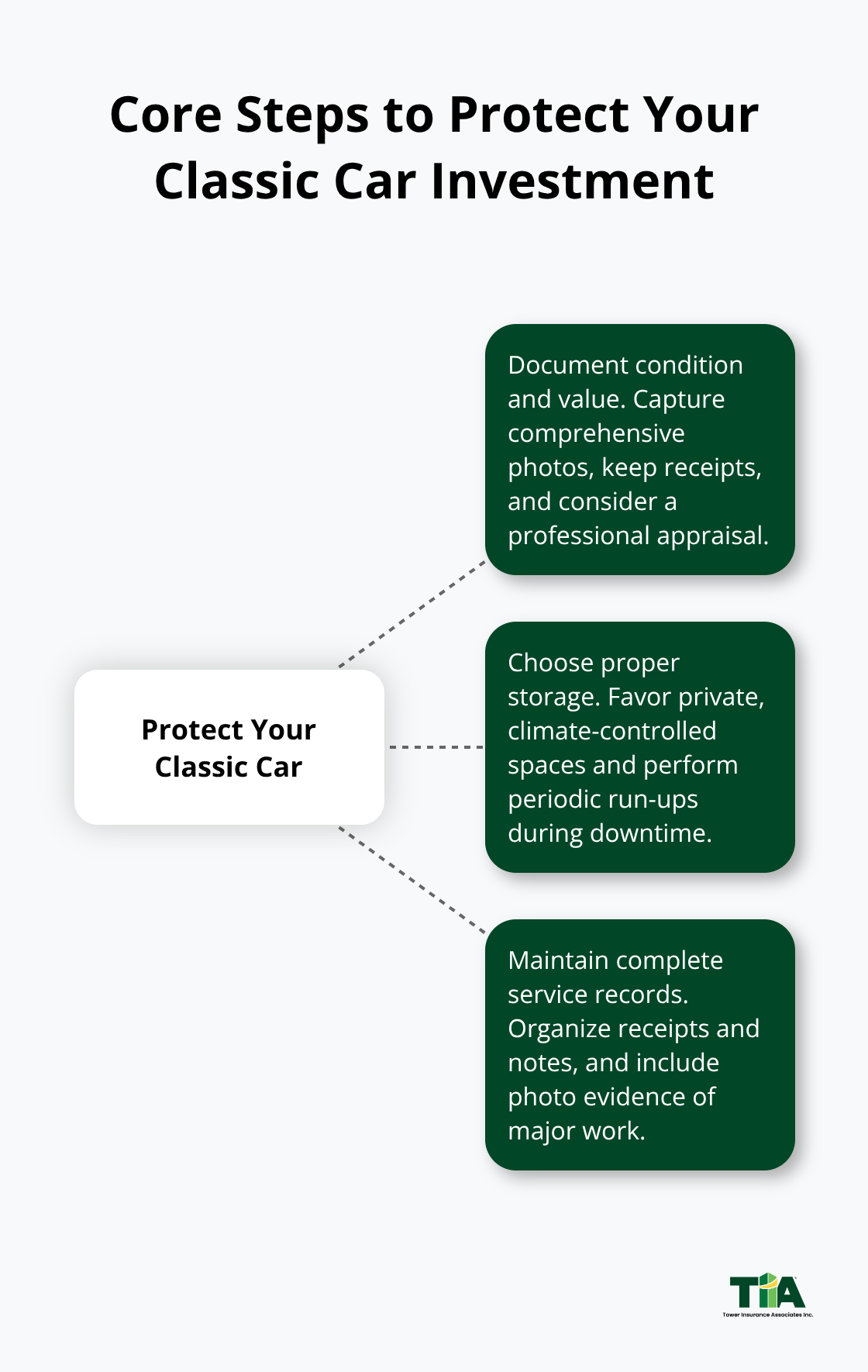

Protecting a classic car investment starts with proving what you own and what it’s worth. Insurance companies need documentation before they’ll agree to cover your vehicle at its actual value, and this paperwork becomes critical when you file a claim. Photograph your classic car from multiple angles in good lighting, capturing the exterior, interior, engine bay, and any unique features or restoration work. Include close-ups of the VIN, odometer, and any custom modifications. If your 1955 Chevrolet Bel Air underwent a frame-off restoration, document each stage of that work with dated photos and receipts from the restoration shop.

Professional appraisals carry significant weight with insurers. Many classic car owners obtain formal appraisals from certified automotive appraisers who specialize in collector vehicles, which typically cost $300 to $500 but provide the documentation insurers require to establish agreed value. Hagerty’s valuation tools offer another approach, allowing you to research comparable sales and market trends for your specific vehicle model and year.

Create a detailed inventory that includes the vehicle’s year, make, model, engine type, current mileage, color, and any factory options like a rare transmission or original paint. Store this documentation digitally and physically in separate locations so you have access even if your home is damaged.

Choose Proper Storage Solutions

Storage conditions directly affect both your vehicle’s preservation and your insurance coverage. Many insurers prefer private garage or storage-unit protection rather than carports or driveways, and some policies offer restoration coverage that applies specifically while your car is actively being worked on. Climate-controlled storage protects against rust, mold, and mechanical deterioration that could invalidate coverage or reduce your car’s market value.

If your classic car remains parked during winter months, start the engine every couple of weeks to circulate oil, check that all fluids remain fresh, and ensure tires don’t develop flat spots from months of stationary weight. For cars in regular use attending shows and cruises, follow monthly maintenance to keep systems functioning.

Maintain Complete Service Records

Service records become your proof that you’ve maintained the vehicle properly, and insurers view well-documented maintenance as evidence of responsible ownership. Keep receipts from every repair, oil change, and restoration work, organized by date with notes about what was performed and why. These records protect your claim if damage occurs and demonstrate to insurers that your vehicle remains in the condition you described during policy application.

Document any major work with photos showing before-and-after conditions, especially restoration projects. This combination of current condition documentation, proper storage practices, and complete service history creates the foundation that allows agreed value coverage to function exactly as intended.

Final Thoughts

Your California classic car policy succeeds when it matches your vehicle’s actual value, your driving habits, and your long-term ownership goals. Agreed value coverage, mileage flexibility, and specialized repair options work together to protect what standard auto insurance ignores: the appreciation, authenticity, and historical significance of your vintage vehicle. These differences compound over years of ownership, protecting both your investment and your peace of mind.

Specialized classic car policies deliver tangible advantages over standard coverage. You pay premiums based on realistic mileage rather than daily-commute assumptions, receive full agreed value in a total loss instead of depreciated amounts, and specify original parts instead of settling for cheaper aftermarket replacements. An independent insurance agency like Tower Insurance Associates, Inc. represents multiple carriers and provides personalized service that goes beyond online quotes, acting as a trusted local adviser rather than a faceless corporation.

Your classic car deserves protection built specifically for its unique circumstances. Connect with specialists who understand the difference between insuring a daily driver and preserving a collector vehicle-they’ll help you document your vehicle’s value, select appropriate coverage limits, and build a policy that reflects how you actually use your vintage treasure.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.