Your classic car deserves protection that standard auto insurance simply doesn’t provide. At Tower Insurance Associates, Inc., we understand that vintage vehicles need specialized coverage designed specifically for their unique value and usage patterns.

California classic car insurance works differently than regular policies because your vehicle isn’t driven daily like a modern car. We’ll walk you through the options available to you and help you find the right coverage for your prized possession.

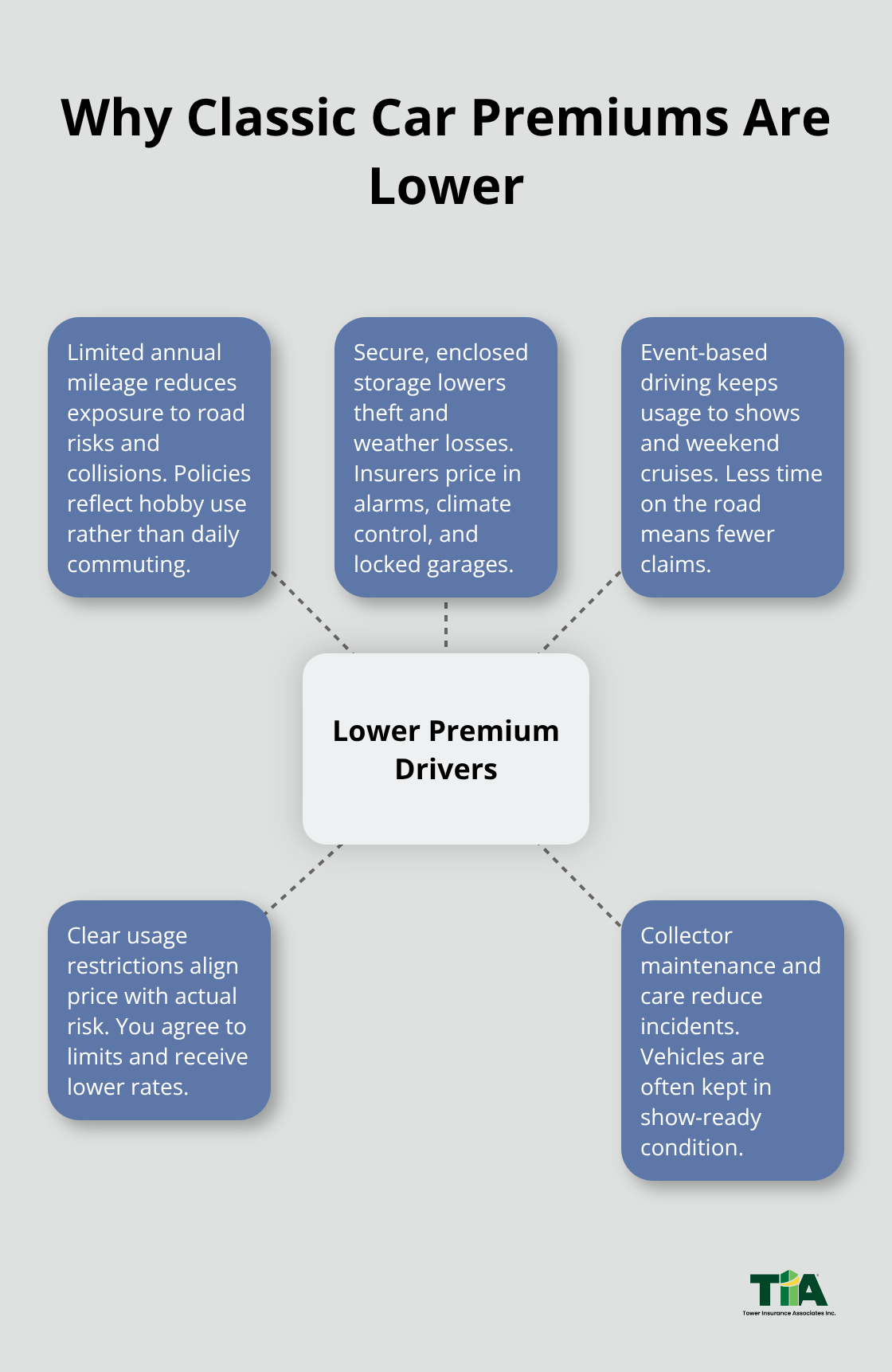

Why Classic Car Insurance Costs Less Than You Might Think

Lower Risk Means Lower Premiums

Classic car insurance operates on a fundamentally different principle than standard auto coverage because your vintage vehicle doesn’t face the same risks as a daily driver. Standard policies charge based on annual mileage and daily commute exposure, but classic car policies recognize that most vintage vehicles are driven fewer than 5,000 miles per year and spend significant time in secure storage. This dramatically reduces the likelihood of accidents, theft, and weather damage. Many collectors drive their classics only to shows, cruises, and weekend events, which means insurers can offer substantially lower rates compared to standard auto coverage. The trade-off is straightforward: you agree to limit your annual mileage and use the vehicle for hobby purposes rather than commuting, and the insurer rewards you with cheaper premiums that reflect your actual risk profile.

Agreed Value Protects Your Investment Better

The biggest advantage of classic car insurance is agreed value coverage, which sets a predetermined payout amount based on your vehicle’s actual worth at the time you purchase the policy. Standard auto insurance uses actual cash value, meaning the insurer pays what the car is worth on the open market at the time of loss, accounting for depreciation. For a restored 1965 Ford Mustang with $50,000 in restoration work, actual cash value might only cover $35,000 after depreciation, leaving you substantially short. Agreed value eliminates this gap entirely. You establish the value upfront using documentation like restoration receipts, professional appraisals, and market data. If your classic is totaled, you receive the agreed value minus your deductible, regardless of what similar vehicles sell for. This means your restoration investments and customizations are fully protected. California collectors especially benefit because the state’s mild weather allows year-round driving, so you can document usage patterns and show insurers exactly how you maintain and protect your vehicle, supporting the agreed value you’ve established.

Storage and Usage Shape Your Premium

How and where you store your classic car directly affects your insurance rate. Vehicles kept in an enclosed, locked garage with climate control and security systems qualify for the lowest premiums because they face minimal environmental and theft risk. If your classic sits in an open carport or outdoor storage, premiums increase significantly. This isn’t theoretical-insurers track claims data showing that proper storage prevents everything from weather damage and wildfire smoke staining to theft and vandalism. You’ll also need to specify your annual mileage limit when you purchase a policy. Most collectors choose between 2,500 and 5,000 miles annually, though some policies allow up to 7,500 miles for owners who drive more frequently. Exceeding your stated mileage voids coverage, so be honest about your plans. If you attend multiple car shows or take longer trips in your classic, choose a higher mileage tier. The premium difference between a 2,500-mile policy and a 5,000-mile policy is typically modest, making it worth the extra cost for peace of mind if you’re uncertain about your actual usage.

What Comes Next in Your Coverage Decision

Your storage setup and mileage patterns form the foundation of your premium calculation, but other factors also influence what you’ll pay. The type of policy you select-whether agreed value, stated value, or a specialized collector car policy-matters significantly. Understanding these options helps you match your coverage to your specific situation and budget.

California Classic Car Insurance Policy Types

Agreed Value Policies Protect Your Full Investment

Agreed value policies stand as the gold standard for classic car owners. These policies set your vehicle’s value upfront using documentation like restoration receipts, professional appraisals, and market comparables. If your 1965 Ford Mustang is totaled, you receive the agreed value you established minus your deductible, with zero depreciation applied. This matters enormously because a fully restored classic might have $60,000 in documented work but sell for $45,000 on the open market. Standard actual cash value policies would pay that lower amount, leaving you short. Agreed value eliminates this problem entirely.

The process requires honesty about your vehicle’s condition and realistic pricing, but once approved, you know exactly what you’ll receive in a total loss. Most California insurers require an appraisal for vehicles valued above $10,000, which costs between $300 and $500 but protects your investment. You’ll need to document all restoration work with receipts and photos, which most serious collectors already maintain. Some policies allow you to increase the agreed value annually if you continue restoration work, so your coverage grows with your investment.

Specialized Endorsements Tailor Coverage to Your Needs

Specialized collector car policies go beyond agreed value by adding endorsements tailored to how you actually use your vintage vehicle. These policies cover spare parts stored at home or in workshops, provide trip interruption coverage if you break down at a car show, and include flatbed towing to prevent undercarriage damage. In-process restoration coverage adjusts your vehicle’s value as restoration progresses, protecting you during the rebuild phase when the car is partially dismantled.

Multi-car policies bundle multiple classics into one comprehensive package with a single deductible and coordinated coverage, simplifying management and often reducing your overall premium. Multi-car policies work best when your vehicles have similar values and usage patterns, though some insurers allow you to customize each car’s mileage limit separately. This flexibility means you can insure a weekend cruiser and a show-only restoration under one policy without overpaying for coverage you don’t need.

California’s Car Club Network Provides Real-World Guidance

California’s car club ecosystem offers invaluable resources for collectors evaluating coverage options. Local clubs host monthly shows and cruises where you’ll encounter other collectors using different policies, giving you real-world feedback about what actually works versus marketing hype.

These connections matter because collectors understand the specific challenges you face-from wildfire smoke damage to earthquake risk to the need for specialized mechanics. Talking with other owners at shows reveals which insurers handle claims quickly, which ones require excessive documentation, and which policies actually deliver on their promises. This peer network often provides more honest assessments than marketing materials alone.

Your choice between agreed value, specialized endorsements, and multi-car policies depends on your specific situation, but the next step involves evaluating which insurance providers can actually deliver the coverage you’ve selected.

Selecting an Insurer That Specializes in Classic Cars

Work with Carriers Who Understand Classic Vehicles

Finding the right insurance provider matters far more than most collectors realize. Many standard auto insurers claim to cover classic cars, but they treat your vintage vehicle like a regular sedan with low mileage-they don’t understand the unique value of restoration work, the importance of agreed value coverage, or how California’s specific risks affect your policy. You need an insurer with genuine expertise in classic car coverage, not a mainstream carrier offering a stripped-down product as an afterthought.

Start with insurers who specialize exclusively in collector vehicles. These companies employ specialists who understand why your 1965 Ford Mustang’s value isn’t depreciation-based like a modern car, why storage conditions dramatically affect risk, and why agreed value matters more than actual cash value. When you call for a quote, ask specific questions about how they calculate agreed value, whether they require appraisals, and what endorsements they offer for spare parts coverage and trip interruption. A specialist insurer answers these questions with confidence and detail; a generalist fumbles or redirects you to a vague policy document.

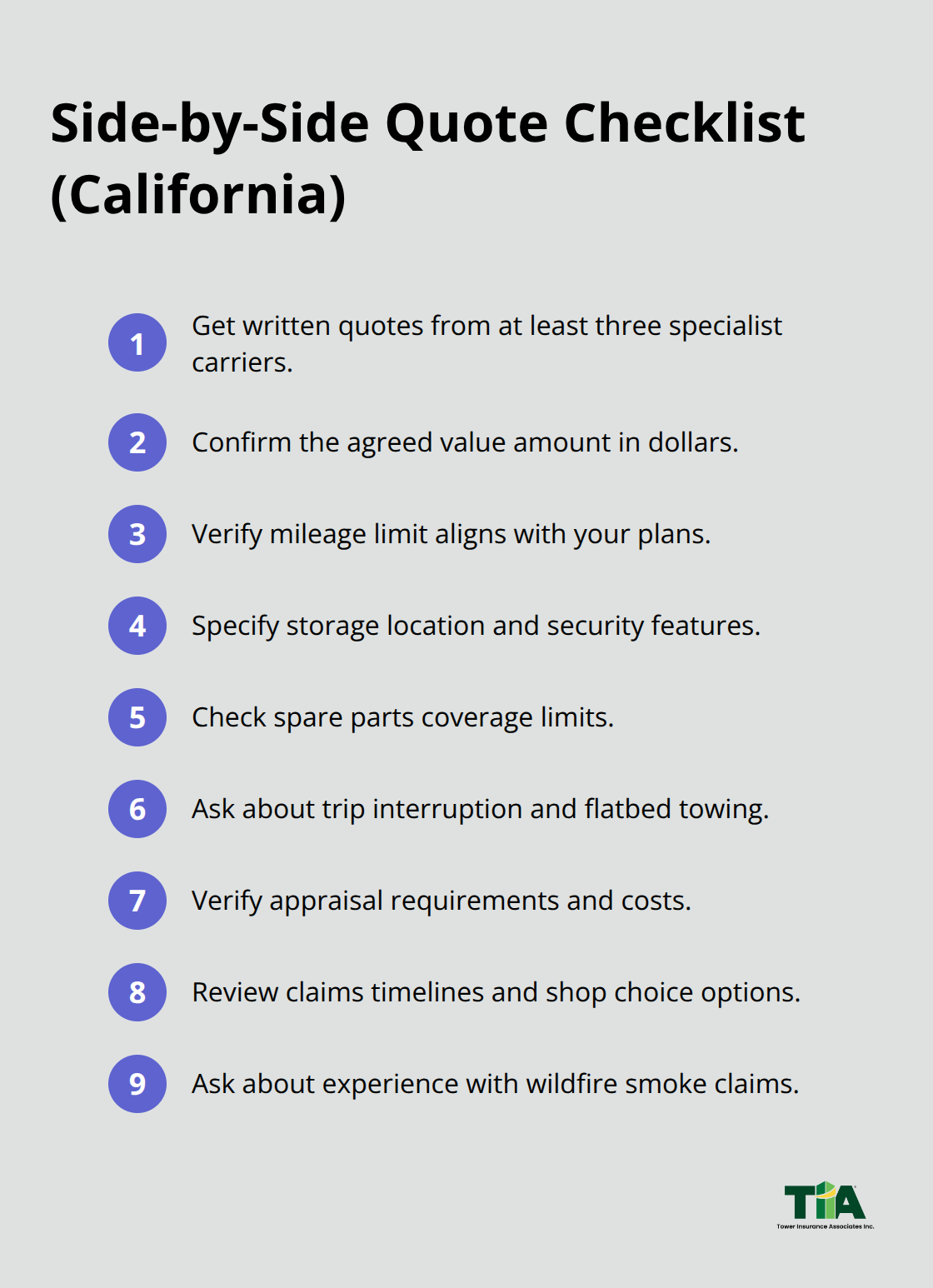

Compare Quotes and Coverage Side by Side

Get quotes from at least three carriers before deciding. Don’t just compare premium prices-compare what each policy actually covers. One insurer might charge $400 annually for agreed value with spare parts coverage, while another charges $350 but excludes spare parts entirely. The cheaper quote only matters if it includes the protections you need.

Request written quotes that specify your agreed value amount, mileage limit, storage location, and coverage limits so you can make direct comparisons. California’s car clubs provide invaluable resources here; members at local shows can tell you which insurers actually pay claims quickly versus which ones create headaches. Ask specifically whether your potential insurer has experience with wildfire smoke damage claims, since California collectors face this risk regularly and need carriers who understand the nuances of proving damage from ash and smoke exposure rather than direct fire.

Investigate Claims Handling Before You Need It

Claims handling separates excellent insurers from mediocre ones, yet most collectors only discover this difference after a loss occurs. Before purchasing a policy, contact the California Department of Insurance and search for complaint records against any carrier you’re considering-this public database reveals patterns of claim denials, delayed payments, and disputes over agreed value amounts.

Call your potential insurer’s claims department directly and ask how they handle total loss claims for classic cars. Do they require multiple appraisals or just one? Can you choose your own repair shop or does the insurer mandate their preferred vendor? How long does the claims process typically take from initial report to payment? Carriers who answer these questions transparently and demonstrate familiarity with classic car claims are your best bets.

Final Thoughts

Selecting the right California classic car insurance policy requires you to balance three critical factors: the coverage type that matches your vehicle’s actual value, the usage restrictions that align with how you drive, and the insurer’s genuine expertise in handling classic car claims. Agreed value coverage protects your restoration investment far better than standard actual cash value policies, but only if you work with a carrier that understands why your vintage vehicle’s worth isn’t determined by depreciation tables. Your storage setup and annual mileage directly affect your premium, so you must be honest about both when requesting quotes.

Working with a local California agent transforms the insurance process from frustrating to straightforward. An independent agency like Tower Insurance Associates, Inc. represents multiple top-rated carriers while providing personalized guidance tailored to your specific vehicle and usage patterns. Rather than forcing you into a generic product, local agents match you with specialist carriers offering the exact endorsements and coverage limits you need, and they advocate for you during claims to resolve disputes quickly.

Gather documentation of your vehicle’s value including restoration receipts, professional appraisals, and photos, then contact multiple insurers or work with an independent agent to request quotes specifying your agreed value amount, mileage limit, and storage location. Compare not just premiums but actual coverage details, and speak with other collectors at local car clubs about their experiences with each carrier. Your classic car represents years of investment and passion-it deserves protection from an insurer who genuinely understands its value.