Your restored classic car represents years of work and investment. Yet many owners discover their standard auto insurance leaves them dangerously underprotected.

A CA classic car policy is built specifically for vehicles like yours, with coverage options that standard policies simply don’t offer. Here at Tower Insurance Associates, Inc., we help classic car owners understand their protection options and find the right fit for their prized rides.

What California Actually Requires for Classic Car Coverage

California treats classic cars differently from daily drivers, and your insurance must reflect that reality. State law requires all vehicles to carry liability coverage, but the minimum limits-$15,000 for bodily injury per person and $5,000 for property damage-were designed for standard vehicles, not restored rides worth tens of thousands or more. Standard auto policies treat your classic car as a depreciating asset, which means they calculate payouts based on actual cash value after a total loss. If your 1967 Chevelle restoration cost $85,000 but the insurer determines its current market value at $65,000, that’s what you’ll receive minus your deductible. This approach ignores the sweat equity, specialized labor, and premium parts you’ve invested into your project.

Why Your Daily Driver Policy Won’t Cut It

Standard auto policies impose annual mileage limits of 12,000 to 15,000 miles and expect regular commuting. They also apply depreciation calculations that penalize older vehicles, even meticulously restored ones. Your classic car policy, by contrast, recognizes that you drive to shows, club meets, and weekend cruises-not sit in traffic. Many owners discover their regular insurer denied claims because the vehicle was used outside normal parameters or because the payout didn’t reflect restoration costs. Standard policies exclude coverage for custom parts, upgraded engines, or modern safety additions you may have installed. California’s mild year-round climate means collectors drive frequently, making flexible mileage plans essential. A dedicated classic car policy accounts for this usage pattern and protects modifications that standard coverage ignores.

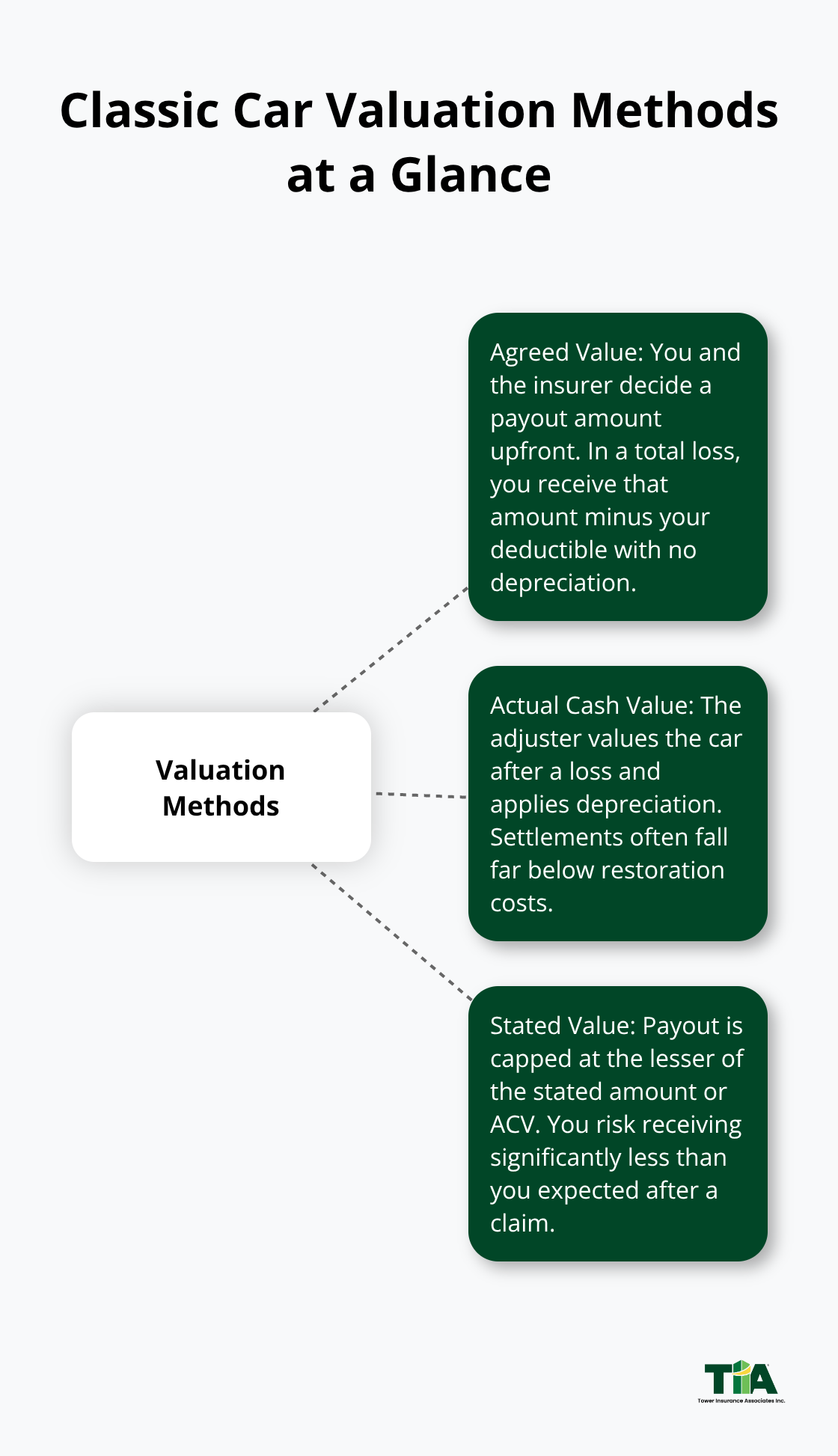

The Protection Gap in Agreed Value

Agreed value coverage separates a proper classic car policy from inadequate standard coverage. With agreed value, you and your insurer establish a specific payout amount before a loss occurs, which eliminates post-loss disputes. If your restored 1975 Porsche 911 is insured for an agreed value of $120,000 and totaled, you receive exactly that amount minus your deductible-no negotiation, no depreciation applied. Standard policies use actual cash value, meaning an adjuster determines what your car is worth after the accident happens, often resulting in settlements far below restoration costs. This difference matters enormously in California’s collector car market, where restored vehicles frequently command prices reflecting labor and materials invested. The Hagerty Price Guide tracks these values, and many California classics appreciate or hold value better than standard vehicles. Agreed value protects your investment from the insurer’s post-loss valuation games and gives you certainty about your coverage limits before anything goes wrong.

Custom Parts and Modifications Need Real Protection

Standard policies treat aftermarket upgrades as liabilities rather than assets. If you installed a modern fuel injection system, upgraded brakes, or custom upholstery, standard coverage either excludes these items or applies depreciation that undervalues your work. A classic car policy recognizes that these modifications increase your vehicle’s worth and functionality. You need coverage that accounts for the full scope of your restoration, including parts you’ve sourced, labor you’ve paid for, and improvements you’ve made. This protection extends to spare parts stored in your garage or workshop (often called TreasureGuard or similar benefits by specialty insurers), which standard policies typically ignore. When you select a classic car policy, verify that it covers your specific modifications and that the agreed value reflects these upgrades.

Moving Forward with the Right Coverage

Understanding California’s requirements reveals why standard auto insurance fails classic car owners. The gap between what state minimums require and what your restoration actually needs is substantial. Your next step involves evaluating your vehicle’s true restoration value and comparing policies that offer agreed value protection tailored to your specific ride.

What Your Restoration Actually Costs to Protect

Agreed value coverage fixes your payout at a predetermined amount, which means you and your insurer decide upfront what your restored classic is worth. If your 1972 Datsun 240Z restoration cost $78,000 and you secure an agreed value policy at that amount, a total loss pays exactly $78,000 minus your deductible-no haggling, no adjuster deciding your car is worth less. Actual cash value operates differently: the insurer calculates what your car is worth today, accounting for depreciation, which often leaves you thousands short of your restoration investment. This gap widens with older vehicles because standard depreciation tables assume wear and neglect, not meticulous restoration work. Hagerty Price Guide documents that California classics frequently appreciate or hold value better than standard vehicles, yet actual cash value ignores this market reality. Stated value sits between these two approaches but carries a critical flaw: your payout is limited to the lesser of your stated value or the actual cash value determined after a loss, meaning you could receive far less than you negotiated. For a $95,000 restoration insured with stated value at $95,000, if the adjuster values the car at $70,000, you receive $70,000. This is why agreed value matters-it eliminates that post-loss valuation dispute entirely.

Protecting Every Upgrade You’ve Made

Custom parts and modifications represent the bulk of your restoration costs, yet standard policies either exclude them or depreciate them aggressively. If you installed a modern fuel injection system, upgraded suspension, custom interior, or performance engine modifications, these additions need explicit coverage under your agreed value. TreasureGuard benefits, offered by specialty insurers, extend protection to spare parts stored in your garage or workshop-a coverage gap that standard auto policies ignore completely. When you compare policies, confirm that modifications appear on your declaration page and that the agreed value reflects their cost. Documentation proves critical here: keep receipts, invoices, and photos of restoration work so the insurer understands exactly what you’ve invested. Many policies require an appraisal before you bind coverage, which is actually your advantage because a professional appraiser accounts for quality labor, sourced parts, and upgrades that standard valuation methods miss.

Mileage Plans That Match Your Driving

Limited mileage discounts reward you for driving your classic car the way it’s actually used: to shows, club meets, and weekend cruises, not daily commuting. California’s mild year-round climate supports frequent collector driving, and insurers recognize this with flexible annual mileage allowances. Standard auto policies assume 12,000 to 15,000 miles annually, but classic car owners typically drive 2,500 to 5,000 miles per year. Policies tailored for collectors offer mileage tiers-often 1,000, 2,500, 5,000, or 7,500 miles annually-with premiums that drop as your mileage limit decreases. If you drive to monthly car club meetings and attend four regional shows annually, a 5,000-mile plan likely covers your usage while cutting your premium compared to standard coverage. Some policies also include coverage for driving to sanctioned events, shows, and club activities, plus storage during off-season months when your car sits idle. Verify whether your policy covers trip interruption or emergency towing if you break down en route to an event, because these additions protect your restoration during the times you’re actually using it.

Coverage That Reflects Your Investment

The real protection gap emerges when you compare what standard policies pay versus what your restoration actually cost. An agreed value policy closes that gap by locking in a payout amount that reflects your true investment, not depreciation tables designed for ordinary vehicles. Your next step involves documenting your restoration costs and selecting a policy structure that protects every dollar you’ve invested in your classic car.

Securing the Right Policy for Your Restoration

Document Your Restoration Investment

Start by collecting documentation of your restoration costs, which forms the foundation for an accurate agreed value. Receipts from parts suppliers, invoices from mechanics and specialty shops, photographs of the restoration process, and professional appraisals all serve as proof that your 1985 Porsche 944 restoration genuinely cost $62,000, not the $40,000 an adjuster might estimate from online listings.

This documentation isn’t bureaucratic overhead-it’s your evidence that your investment reflects quality work and sourced components. When you request quotes, contact specialty insurers who focus on classic cars rather than standard auto carriers. American Collectors Insurance, Hagerty, and Grundy specialize in agreed value coverage and understand that California classics often appreciate or hold steady rather than depreciate like ordinary vehicles. Request quotes that specify the valuation method: agreed value, actual cash value, or stated value. The difference between these approaches can mean thousands of dollars in a claim. For a $75,000 restoration, an agreed value policy pays exactly that amount after a total loss, while actual cash value might pay $55,000 based on depreciation tables that ignore your quality work.

Compare Coverage Details Across Policies

When comparing quotes, verify that each policy explicitly covers your modifications and includes the mileage allowance that matches your driving. If you attend monthly car club meets and drive to four regional shows annually, a 5,000-mile annual limit likely fits your needs while reducing your premium compared to policies designed for higher mileage. Ask whether the policy covers trip interruption, emergency towing, and spare parts storage-these additions protect you during the times you’re actually using your restoration. Confirm that the insurer’s claims process handles total losses promptly; contact their claims department directly and ask how long settlement typically takes. Request references from other California classic car owners if possible, or check independent review sites for real policyholder experiences.

Select an Agent Who Understands Your Restoration

The agent you select matters enormously because they’ll advocate for you during claims and help you adjust coverage as your restoration value changes. Choose an agent or agency with demonstrable experience handling classic car claims, not someone treating your restoration like a standard vehicle. An independent agency represents multiple carriers and can match your specific vehicle, driving patterns, and restoration investment to the right vintage car policy. Your restoration represents a significant investment, and your policy should reflect that reality with clear agreed value language, explicit modification coverage, and mileage flexibility that matches how you actually drive. Verify that the agent explains how each policy’s valuation method protects your investment and can answer specific questions about how modifications affect your agreed value.

Final Thoughts

Your restored classic car deserves protection that matches its true value, not depreciation formulas designed for ordinary vehicles. A CA classic car policy closes the gap between what standard coverage offers and what your restoration actually needs. Agreed value protection locks in your payout upfront, custom parts coverage accounts for every upgrade you’ve made, and flexible mileage plans reward you for driving the way collectors actually drive.

We at Tower Insurance Associates, Inc. understand that your classic car represents years of work and financial commitment. Contact Tower Insurance Associates, Inc. to discuss your coverage options and compare quotes from specialty carriers that understand how modifications affect your agreed value. Our team handles the details that matter: verifying modification coverage, confirming agreed value language, and ensuring your mileage allowance matches your driving patterns.

Gather your restoration documentation-receipts, invoices, appraisals, and restoration photos-and reach out to us today. Your restoration is too valuable to leave unprotected by standard auto insurance, and we’ll help you secure the right coverage for your investment.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.