Your classic car represents years of passion and investment. Whether you’re restoring a 1967 Chevelle or maintaining a pristine 1955 Thunderbird, standard auto insurance falls short of protecting what makes your vehicle special.

At Tower Insurance Associates, Inc., we understand that CA classic car insurance requires a different approach than everyday coverage. This guide walks you through the specialized protection options available to California collectors.

What Qualifies Your California Restoration as Classic Car Coverage

Age and Condition Requirements

California vehicles manufactured after 1922 can qualify for historic license plates, but insurance eligibility works differently than registration rules. Most insurers set the minimum age at 25 years old, though some carriers accept vehicles as recent as 20 years old depending on their underwriting standards. The vehicle’s condition matters more than its age-insurers expect the car to be in good working order and worth significantly more than the average used car.

When Your Restoration Project Qualifies

A 1967 Chevelle that will eventually be worth $45,000 once complete qualifies for classic coverage. A 1955 Thunderbird still running on original parts and valued at $30,000 absolutely qualifies. What disqualifies a vehicle is using it as your daily driver. Insurers require that you own another vehicle for regular transportation and use the classic car primarily for exhibitions, automotive events, and occasional pleasure drives. This usage restriction is why classic coverage costs less than standard auto insurance-you avoid commute traffic and parking lot damage.

Agreed Value Coverage Protects Your Investment

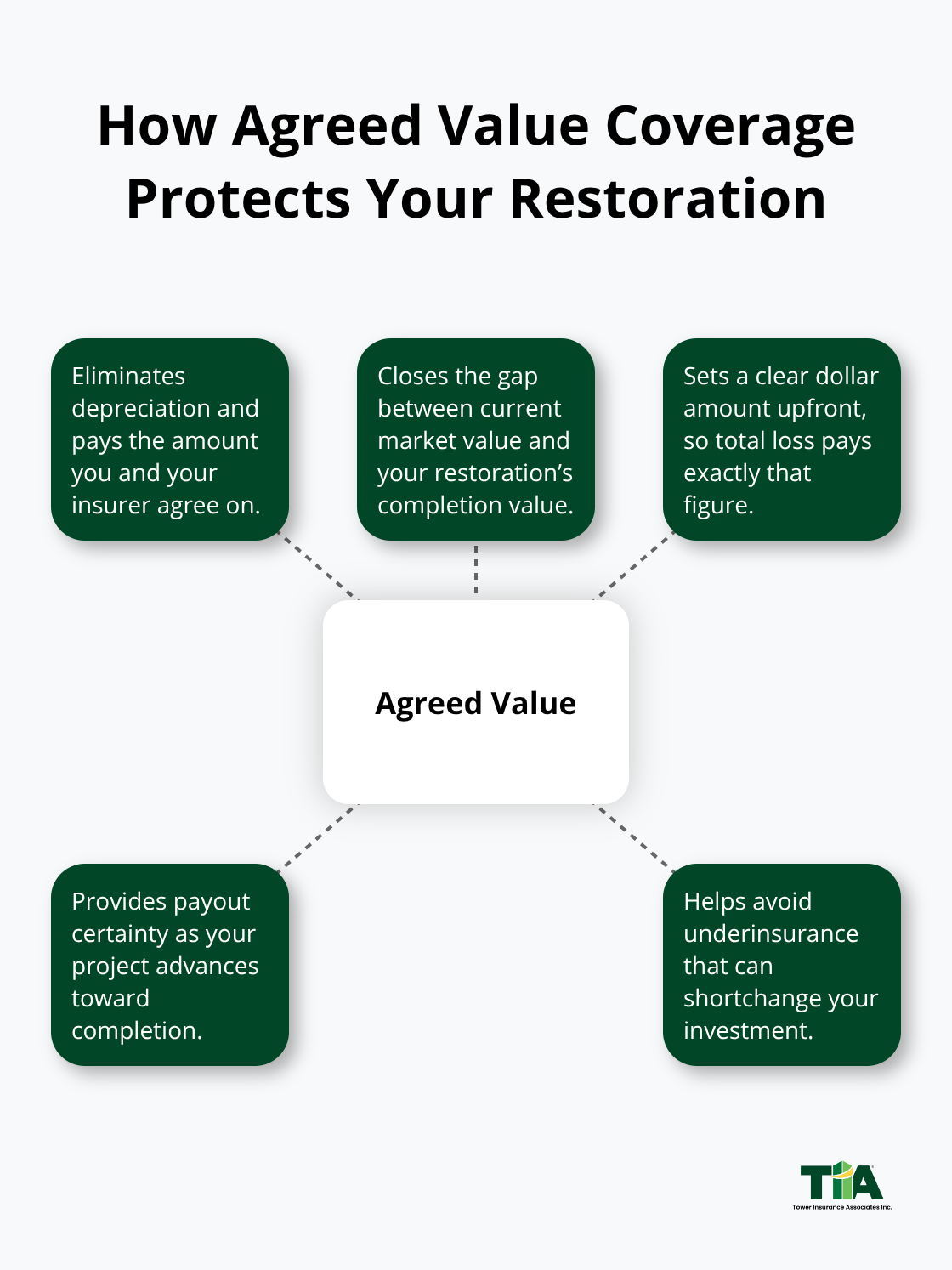

Standard auto policies pay current market value when a claim occurs, which creates a massive problem for restoration projects. If your Chevelle is worth $8,000 today but will be worth $45,000 when restoration finishes, standard coverage leaves you massively underinsured. Agreed value coverage sets a specific dollar amount that the insurer will pay if total loss occurs. This approach protects your actual investment rather than what the market says the car is worth at claim time.

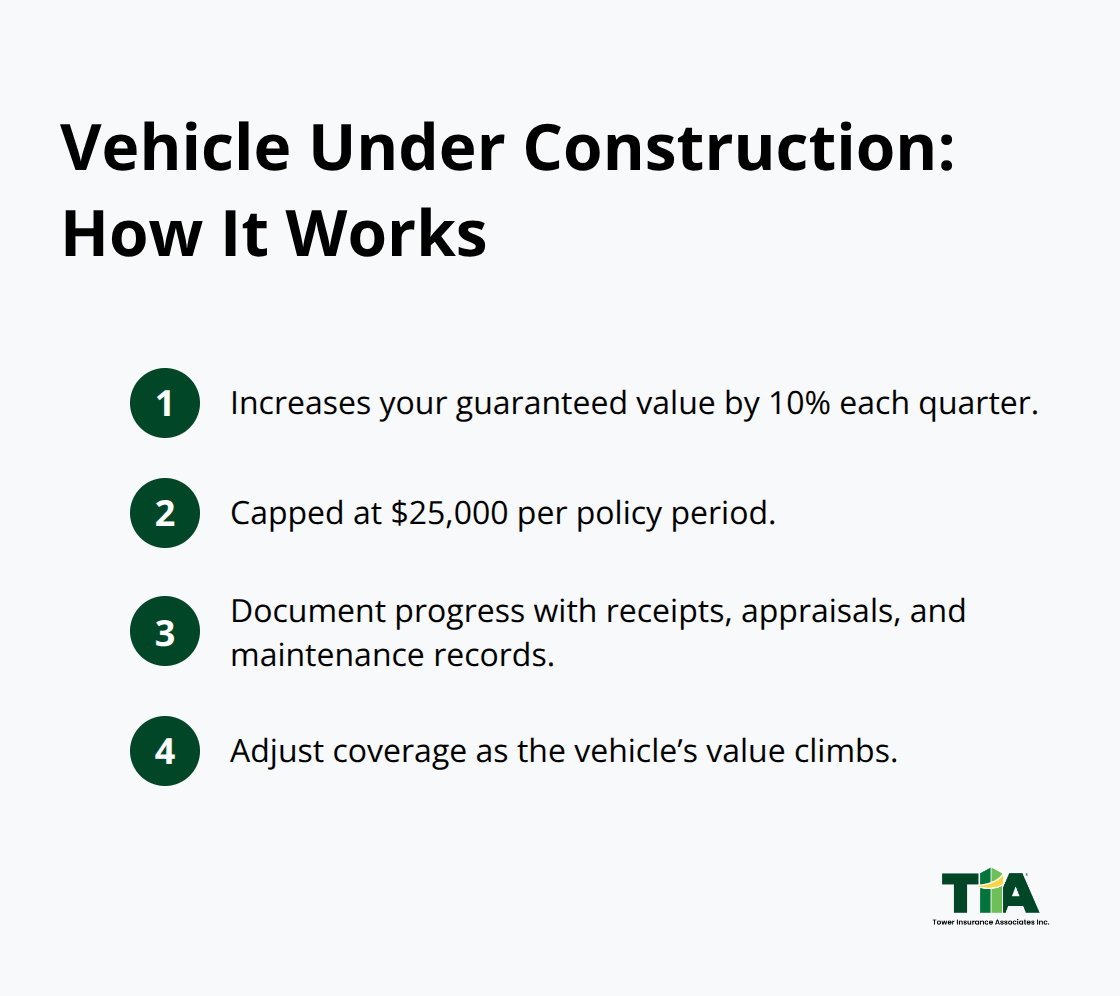

Hagerty’s Vehicle Under Construction coverage increases the guaranteed value by 10 percent each quarter, capped at $25,000 per policy period, which directly addresses how restoration projects gain value incrementally. You document the restoration with receipts, appraisals, and maintenance records, then adjust your coverage as the vehicle’s value climbs.

Additional Protections for Stored and Displayed Vehicles

Comprehensive coverage under classic insurance applies when the car sits in storage or displays at shows-standard policies don’t cover parked vehicles the same way. Roadside assistance comes standard with most classic policies, which matters when you travel to a concours event three hours away or need a tow after a test drive reveals a mechanical issue. These features address the specific needs of collectors who store vehicles between events and exhibitions.

Protecting Your Restoration Investment With Proper Coverage

Agreed Value Coverage Closes the Underinsurance Gap

Agreed value coverage separates classic car insurance from standard policies in one fundamental way: it eliminates depreciation and pays what you and your insurer agree the vehicle is worth, not what the market says it’s worth on the day of loss. When you restore a 1967 Chevelle that started at $8,000 but reaches $45,000 upon completion, standard coverage creates a dangerous gap. The insurer pays current market value, leaving you thousands short of your actual investment. With agreed value, you and your insurer set a specific dollar amount upfront-say $35,000 as your Chevelle nears completion-and that’s exactly what you receive if total loss occurs.

Hagerty’s Vehicle Under Construction coverage takes this further by increasing your guaranteed value 10 percent quarterly, capped at $25,000 per policy period. Your coverage grows alongside your restoration progress. You support this value with documentation: restoration receipts, professional appraisals, and maintenance records that prove the car’s increasing worth. This approach eliminates the underinsurance problem that catches many restoration owners off guard.

Limited Mileage Policies Reward Low Usage

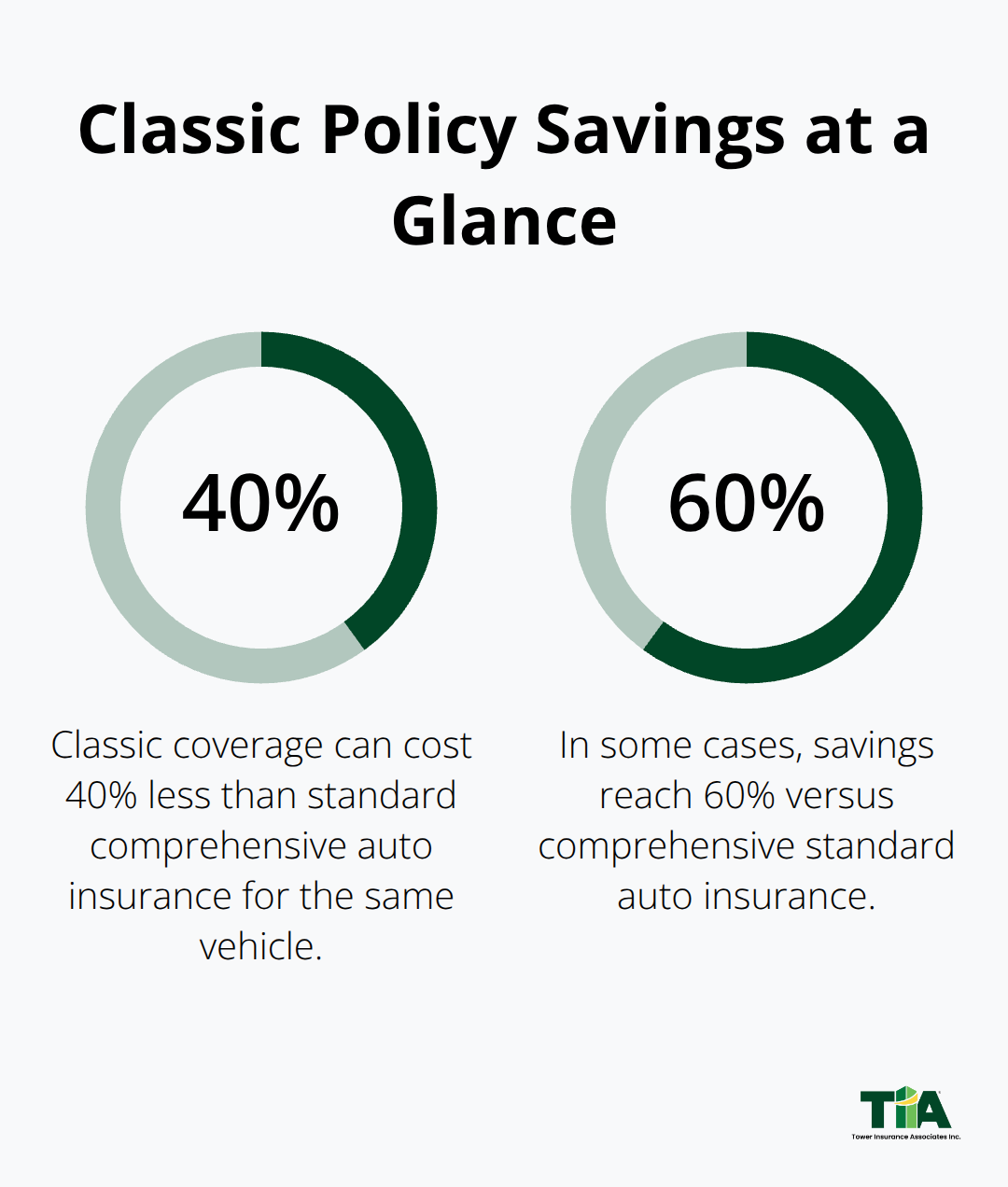

Classic car policies reward low usage with significantly lower premiums than standard auto insurance. Most carriers cap annual mileage at 2,500 to 5,000 miles, reflecting that your vehicle sits in storage between shows rather than commuting daily. This usage-based structure is why classic coverage often costs 40 to 60 percent less than comprehensive standard auto insurance for the same vehicle.

If you plan to drive your restoration to three concours events yearly plus occasional weekend cruises, you’ll stay well within these limits. Exceeding your mileage allowance triggers surcharges or policy cancellation, so track your odometer readings before renewal. Some insurers allow seasonal adjustments-higher limits during summer show season and lower limits during winter storage months-which gives flexibility without overpaying for unused coverage.

Comprehensive Coverage Protects Stored and Displayed Vehicles

Comprehensive coverage under classic policies protects your vehicle while stored or on display, covering theft, vandalism, weather damage, and animal damage regardless of whether the car is parked or driven. This matters because many restoration projects spend months in garages between work sessions. Roadside assistance comes standard with most classic policies, which helps when you travel to a concours event three hours away or need a tow after a test drive reveals a mechanical issue.

Collision Coverage for Active Restoration Work

Collision coverage applies to accidents during test drives or transport to events, and it’s essential if you actively use your restoration rather than keeping it purely static. The deductible you choose-typically $500 to $1,000-directly affects your premium. A higher deductible saves money if you’re confident in your driving habits and have adequate emergency funds, while a lower deductible makes sense if your restoration is a show vehicle you drive infrequently and want maximum protection per incident.

The coverage options available to you depend on your specific restoration timeline and usage plans. As you finalize which protections fit your project, coverage adjustments become important when your vehicle’s value increases during completion phases. The next step involves identifying an insurance provider who understands California’s unique requirements and can adjust your coverage as your restoration progresses.

Choosing an Insurance Partner Who Understands Your Restoration

Why Generic Insurers Fall Short for Restoration Projects

Finding the right classic car insurance provider means working with someone who grasps what your restoration actually costs and how its value evolves. Generic online insurers treat classic cars like any other vehicle-they plug numbers into automated systems and generate quotes without understanding that your 1967 Chevelle’s value depends entirely on completion status and restoration quality. You need an agency that recognizes the difference between an $8,000 project car and a $45,000 finished restoration, and adjusts your coverage accordingly.

Hagerty specializes in classic and antique vehicles and offers Vehicle Under Construction coverage specifically designed for active restoration projects. This focus on restoration-in-progress matters because most standard carriers simply cannot accommodate the incremental value growth that characterizes a multi-year project.

What to Ask Potential Insurance Providers

When evaluating providers, ask directly whether they offer agreed value coverage that increases automatically as your vehicle gains value. Request documentation of how they handle mid-project claims if something damages your restoration before completion. Ask whether they’ve handled claims for vehicles actively undergoing restoration, and request references from other California collectors whose projects resemble yours.

Clarify their claims process specifically-can you report damage via phone or must you use an app, how quickly do adjusters visit your location, and can they work with your preferred restoration shop or do they mandate their own vendors? These operational details determine whether a claim becomes a minor inconvenience or a months-long nightmare.

California-Specific Experience Matters

California-specific experience separates competent providers from those who fumble through state regulations and local requirements. Your insurance partner should understand that California’s historic license plate rules differ from coverage eligibility standards, and that storage facilities in Los Angeles face different theft and vandalism risks than those in rural areas. Tower Insurance Associates, Inc., an independent agency in Culver City serving the California market since 1961, represents multiple carriers and can match your specific restoration needs with appropriate coverage rather than forcing you into one-size-fits-all options.

Coverage Features That Support Active Restorations

The best providers offer seasonal mileage adjustments so you pay less during winter storage months and more during summer show season. They provide flexible coverage limits that grow as your restoration progresses, and roadside assistance that actually covers towing to events three hours away rather than just the nearest repair facility. These operational details determine whether your insurance partnership supports your restoration goals or simply creates administrative friction.

Final Thoughts

CA classic car insurance protects your restoration investment in ways standard policies simply cannot match. Agreed value coverage eliminates the underinsurance gap by paying what you and your insurer agree the vehicle is worth, not what depreciation tables suggest. Vehicle Under Construction coverage increases your guaranteed value quarterly, directly addressing how restorations gain value as you complete each phase of work.

Getting a quote starts with documenting your vehicle’s current condition and projected final value through restoration receipts, professional appraisals, and maintenance records. Contact an insurance provider who specializes in classic vehicles and understands California’s specific requirements rather than relying on generic online insurers that treat your restoration like any other car. An independent agency representing multiple carriers can match your restoration needs with appropriate coverage that adjusts as your vehicle’s value climbs.

Tower Insurance Associates, Inc. serves California collectors with personalized service from agents who understand the classic car market. Visit Tower Insurance Associates, Inc. to discuss your restoration project and receive coverage that evolves alongside your investment.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.