Cyberattacks on small businesses have increased 300% over the past three years, making cyber liability coverage no longer optional. At Tower Insurance Associates, Inc., we help local firms understand what protection actually costs and what coverage gaps could drain your budget.

Getting business cyber liability quotes from multiple insurers reveals dramatic differences in price and protection. This guide walks you through comparing quotes side-by-side so you pick the policy that matches your real business needs.

Why Cyberattacks Now Threaten Your Bottom Line

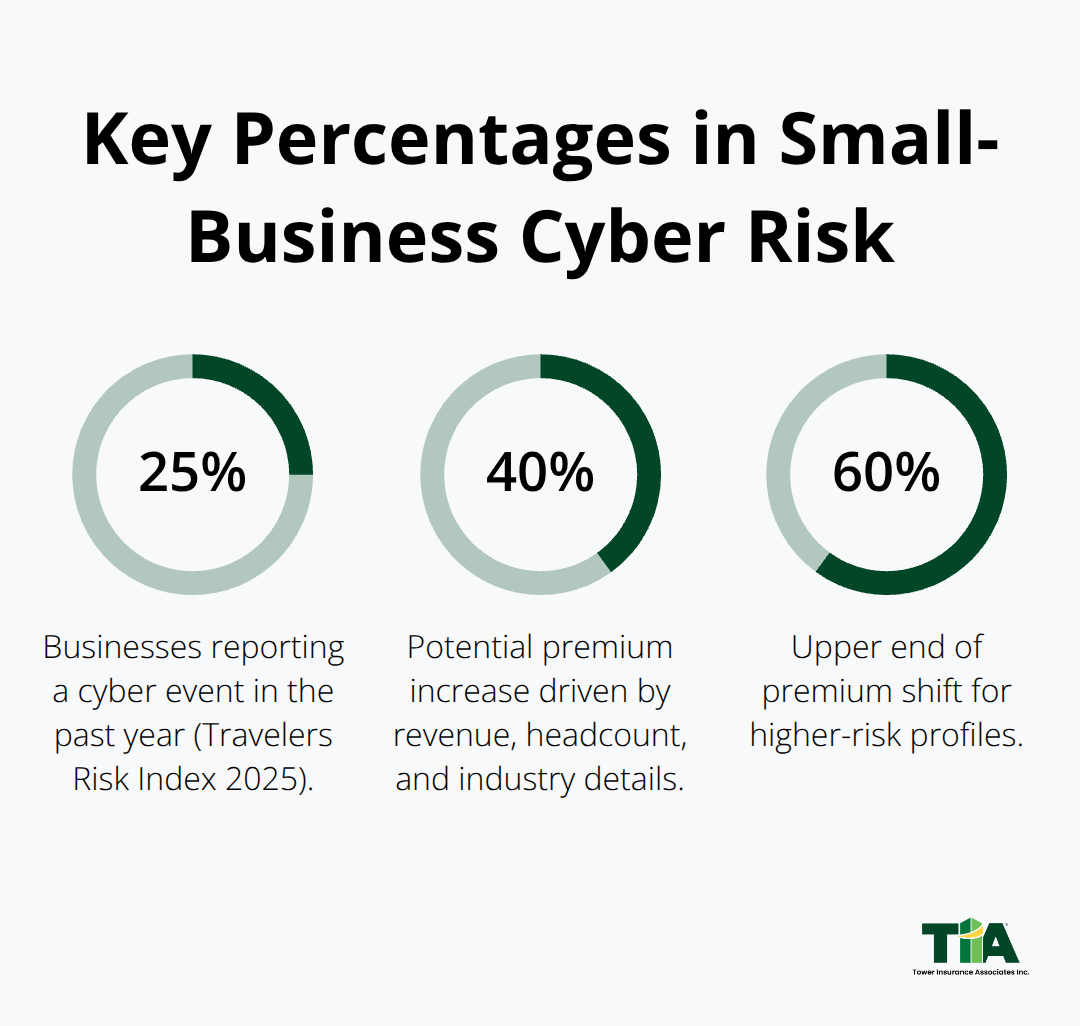

Small businesses face a stark reality: cyberattacks targeting firms with fewer than 250 employees jumped 300% over the past three years, according to industry data tracking breach frequency. Ransomware attacks alone cost small firms an average of $200,000 per incident when you factor in downtime, recovery, and ransom payments. A single data breach affecting customer information triggers notification costs, forensic investigations, and credit monitoring obligations that pile up fast. Regulatory fines add another layer of financial exposure. If your business handles payment card data, you face PCI compliance requirements. If you store health information, HIPAA violations carry penalties starting at $100 per record. Many small-business owners assume cyber incidents happen to other companies, but the data tells a different story: 25% of surveyed businesses reported experiencing a data breach or cyber event in the past year, according to the Travelers Risk Index 2025. That statistic includes retailers, restaurants, contractors, real estate agents, and consultants-the very industries that operate on thin margins and cannot absorb six-figure recovery costs.

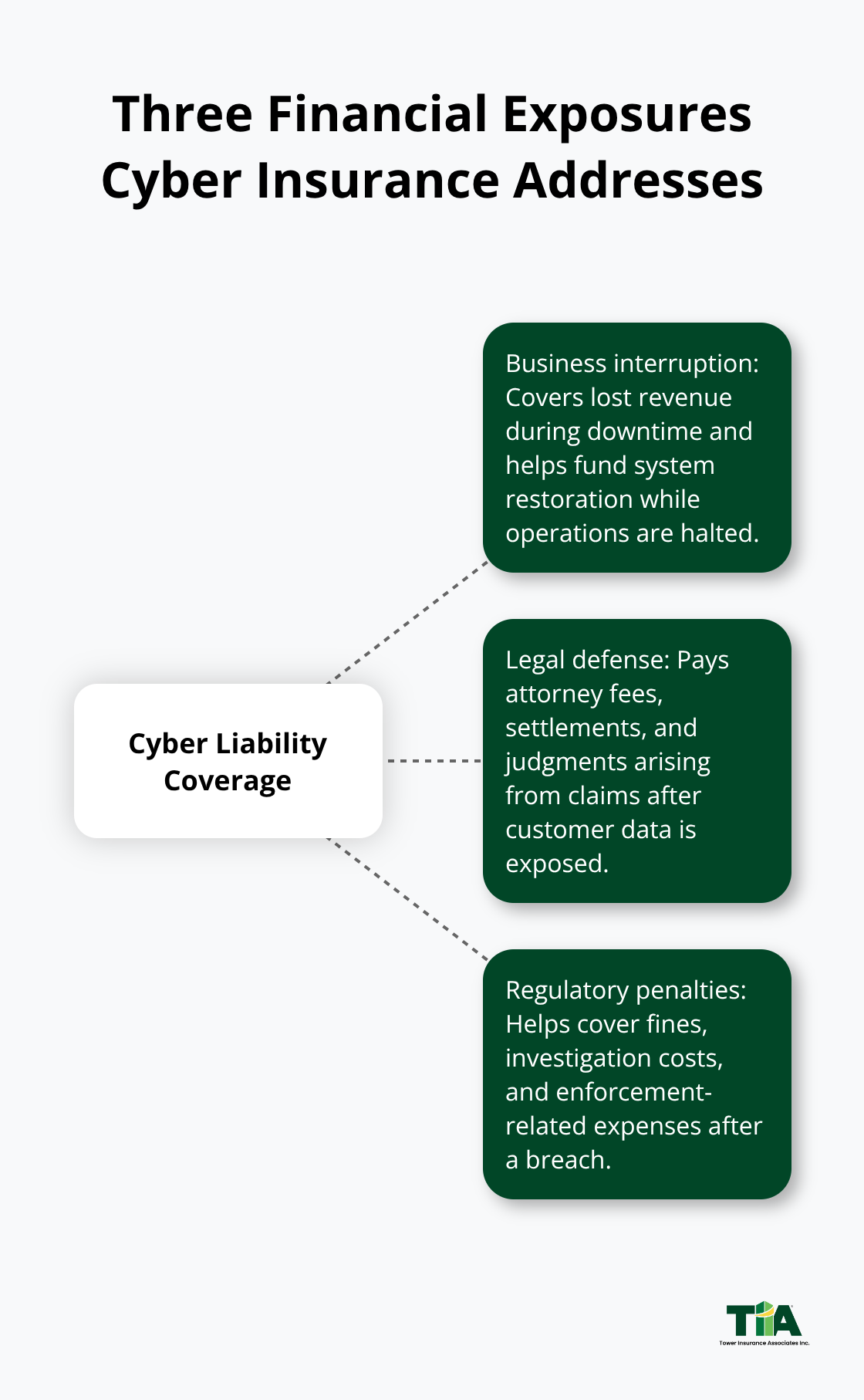

Business Interruption Costs Exceed Most Expectations

When ransomware locks your systems, your business stops generating revenue immediately. A healthcare provider hit by ransomware loses patient appointment fees. A contractor cannot access project files or billing software. A salon cannot process bookings. The average cost of downtime runs $5,600 per minute for small firms, meaning even a four-hour outage costs over $1.3 million in lost productivity and customer service disruption. Cyber liability insurance covers business interruption losses directly, reimbursing lost revenue while your IT team restores systems. Without this coverage, you absorb the full financial hit while competitors serve your customers.

Legal Defense Costs Mount Quickly After a Breach

Legal defense costs compound the damage further. If a breach exposes customer data, affected clients often file lawsuits claiming negligence or failure to protect personal information. Legal fees to defend these claims reach $50,000 to $150,000 before settlement or judgment. Third-party cyber liability coverage pays these defense costs, settlements, and court-ordered damages, protecting your business from bankruptcy-level exposure.

Regulatory Fines Create Unexpected Financial Penalties

State and federal regulations increasingly require proof of reasonable cybersecurity measures and breach notification within specific timeframes. California’s Consumer Privacy Act and similar state laws impose mandatory notification costs on businesses that experience breaches. If regulators determine your firm failed to maintain adequate security controls, fines follow. Some industries face stricter requirements than others. Healthcare providers must comply with HIPAA. Financial services firms answer to data-protection rules set by the Federal Trade Commission. Real estate agents holding client financial documents face state-level privacy regulations. Non-compliance is not a technical issue-it is a legal and financial liability that cyber insurance addresses directly. Coverage for regulatory fines and penalties helps absorb costs from investigations and enforcement actions, reducing the financial penalty your business faces when regulators examine your incident response. Understanding these three financial exposures-business interruption, legal defense, and regulatory penalties-shapes what coverage limits and deductibles actually matter when you compare quotes from different insurers.

What Makes One Cyber Liability Quote Better Than Another

First-Party vs. Third-Party Coverage: The Foundation of Comparison

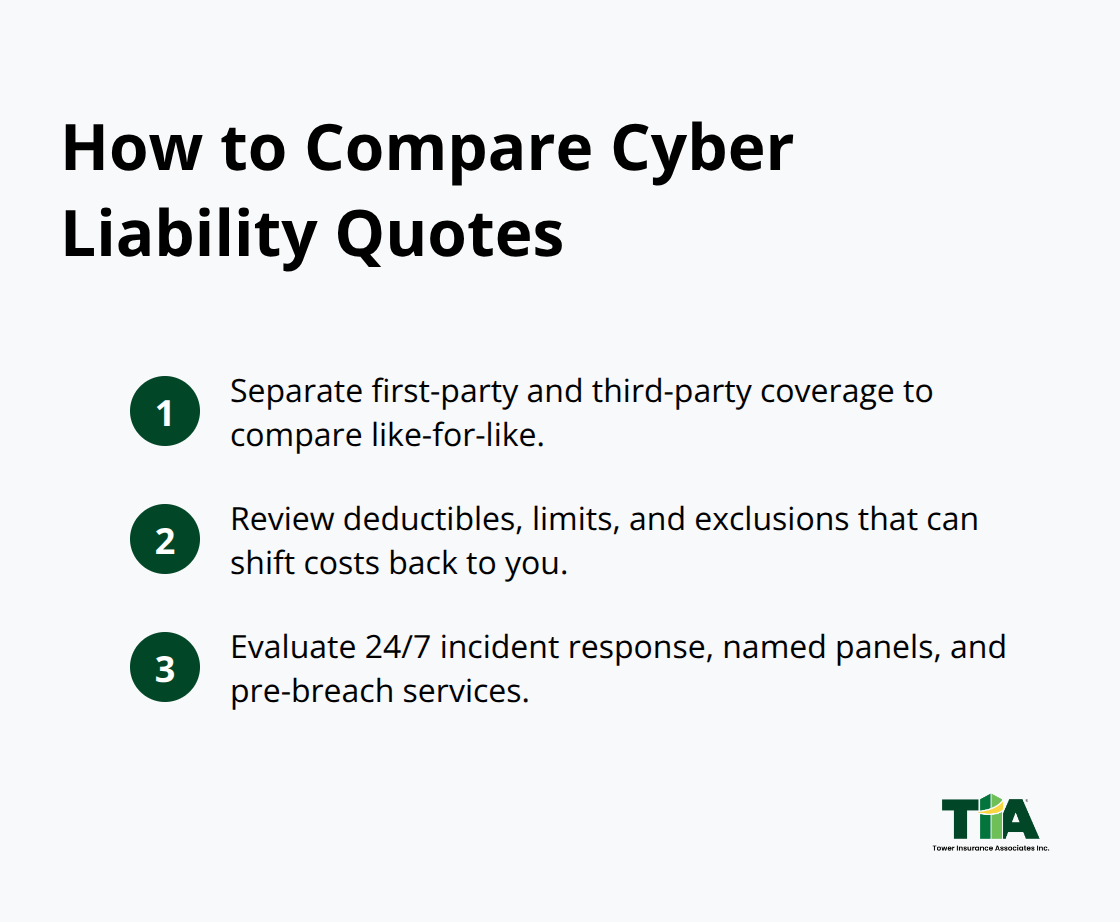

Comparing cyber liability quotes requires you to look beyond the premium number. Two policies priced identically can deliver vastly different protection because coverage scope, deductible structure, and exclusion language vary dramatically across carriers. When you request quotes from multiple insurers, demand that each quote itemize first-party coverage separately from third-party coverage so you can compare apples to apples.

First-party coverage reimburses your incident response costs: forensic investigations to determine how the breach happened, customer notification expenses, credit monitoring services you provide to affected clients, business interruption losses while systems are down, and data recovery or reconstruction costs. Third-party coverage protects you against lawsuits and regulatory action: legal defense fees if a client sues for negligence, settlements and court judgments, regulatory fines from data protection law violations, and reputation management or crisis PR services.

Deductibles and Limits: Where Hidden Costs Hide

A $5,000 deductible on a $1 million policy sounds reasonable until you realize your forensic investigation alone costs $15,000 to $25,000, meaning you absorb that gap before coverage kicks in. Major carriers offering cyber liability insurance specialize in small-to-mid-market cyber with capacity up to $10 million and earned recognition for underwriting discipline, making them a practical benchmark for comparing limits and deductible structures against larger carriers.

Ask each insurer whether they cover known-vulnerability exclusions or fail-to-maintain-security language that could deny claims if regulators later determine your security posture was inadequate. This exclusion matters because it shifts financial risk back to you in scenarios where outdated software or unpatched systems contributed to the breach.

Business Size, Industry, and Premium Drivers

Your business size and data volume drive premium costs significantly. A ten-person consulting firm handling client financial documents pays roughly $129 per month or $1,552 per year according to small-business cyber insurance averages, while a 50-person retail operation processing hundreds of customer transactions daily faces higher premiums because the attack surface and potential loss severity increase proportionally.

Industry matters equally: healthcare providers paying for HIPAA compliance face steeper premiums than construction contractors because the regulatory fines for healthcare data breaches start at $100 per compromised record. Major carriers dominate the small-business cyber market, but market size does not equal the best fit for your specific risk.

Incident Response Infrastructure and Pre-Breach Services

Request that quotes include information about each carrier’s 24/7 breach response infrastructure and whether they maintain named forensic and legal panels or use ad-hoc vendors. Leading insurers launched dedicated incident response programs specifically to provide 24/7 expert guidance during active incidents, while others offer a dedicated cyber center with a breach response hotline. This infrastructure difference directly impacts your out-of-pocket costs and recovery timeline when an incident occurs.

Do not accept vague language about incident response services. Demand specifics: which forensic firms does the carrier use, what are response time guarantees, and how does the carrier coordinate with your IT team during the crisis. Carriers offering pre-breach risk assessments or security training add value that reduces your expected losses and sometimes justifies higher premiums because they prevent incidents rather than simply paying for them afterward. Compare the timeline and ease of the quoting process itself as an indicator of carrier responsiveness-some insurers require extensive questionnaires and take weeks to respond, while others provide preliminary quotes within 24 hours. Your timeline for purchasing coverage matters, and a carrier that moves quickly while thoroughly underwriting your risk signals operational efficiency that extends into claims handling and shapes your experience long after you purchase the policy.

Getting Accurate Quotes from Insurers

Document Your Data Exposure and Business Operations

Requesting cyber liability quotes requires specificity about your business operations, not vague generalizations. Insurers cannot price your risk accurately without concrete details about your data exposure, employee count, annual revenue, and the systems you operate. Start by documenting exactly what customer information you collect and store: names and email addresses require less protection than payment card data or health records, which trigger stricter regulatory requirements and higher premiums. Next, list your critical business systems and how many people access them daily. A ten-person consulting firm where everyone works from secure offices presents lower risk than a retail operation with 50 staff members, multiple locations, and public Wi-Fi networks. Insurance underwriters also need to know whether you process payments directly or use third-party processors, because payment card handling adds complexity and cost.

Provide Complete Business Information to Insurers

When you contact insurers for quotes, provide your annual revenue, the number of employees, and your industry classification. This information alone can shift your premium by 40 to 60 percent because a healthcare provider handling patient data faces vastly different underwriting than a construction contractor managing project schedules. Industry drives premium variation more than most business owners expect.

Healthcare providers pay significantly higher rates because HIPAA violations can result in substantial penalties, creating enormous tail risk for insurers. Financial services firms face similar scrutiny. Retailers and restaurants typically fall into mid-range pricing. Construction contractors and real estate agents occupy lower risk tiers, though real estate agents storing client financial documents sometimes face steeper rates depending on data volume.

Request Multiple Quotes Simultaneously

Request quotes from at least three carriers simultaneously so you can compare first-party and third-party coverage side-by-side without outdated information skewing comparisons. Some insurers respond within 24 hours with preliminary quotes; others require extensive questionnaires and take two weeks. This response speed matters because it reveals operational efficiency that extends into claims handling when you actually need support during an incident. Carriers that move quickly typically maintain streamlined underwriting processes and faster claim resolution.

Evaluate Incident Response Capabilities and Pre-Breach Services

Do not accept quotes without asking each insurer about their incident response capabilities, forensic panel partnerships, and whether they offer pre-breach security assessments or training. These services sometimes justify higher premiums because they prevent incidents rather than simply paying for recovery afterward. The timeline for receiving multiple quotes typically ranges from three to ten business days once you submit complete information, though some carriers offer same-day preliminary quotes if you complete their online assessment tools accurately. At Tower Insurance Associates, Inc., we represent multiple top-rated carriers and help local firms compare coverage options side-by-side to find tailored protection at competitive pricing.

Final Thoughts

Cyber liability coverage protects your business from three financial exposures that force closure: business interruption losses when systems go down, legal defense costs after a data breach, and regulatory fines from non-compliance. When you compare business cyber liability quotes from multiple carriers, focus on first-party coverage that reimburses your incident response costs and third-party coverage that defends you against lawsuits and regulatory action. Deductibles and exclusions matter more than the premium price alone because a low-cost policy with high deductibles or known-vulnerability exclusions leaves you exposed when incidents occur.

Your industry, business size, and data volume determine what coverage limits and deductible structures actually protect your operation. A healthcare provider handling patient records needs different coverage than a construction contractor managing project files. Request quotes from at least three carriers simultaneously so you can compare incident response capabilities, forensic panel partnerships, and pre-breach services without outdated information skewing your decision.

Carriers offering 24/7 breach response infrastructure and security assessments add real value that prevents incidents rather than simply paying for recovery afterward. Working with a local insurance agent who represents multiple top-rated carriers accelerates the quoting process and ensures you understand what each policy actually covers. Contact Tower Insurance Associates, Inc. to request business cyber liability quotes from carriers that match your specific risk profile and budget.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.