Founding a startup means wearing multiple hats, but one hat you can’t afford to lose is legal protection. Directors and officers face real personal liability when decisions go wrong, from employment disputes to regulatory missteps.

At Tower Insurance Associates, Inc., we’ve seen how quickly legal defense costs can cripple an early-stage company. D&O for startups isn’t a luxury-it’s a practical shield that protects your personal assets and keeps your business running when claims hit.

Why Your Startup Needs D&O Protection

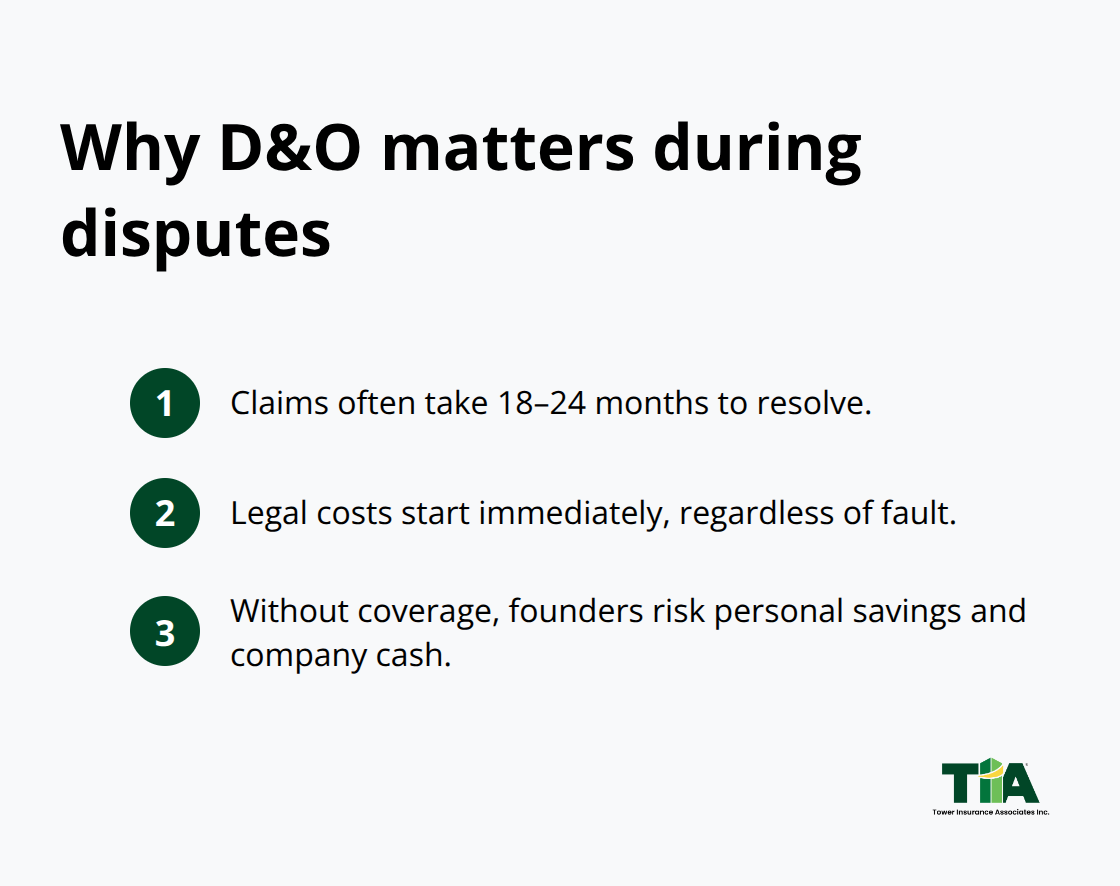

Founders often assume legal problems happen to other companies, not theirs. The reality is harsher. A single employment dispute, investor allegation, or regulatory inquiry costs significant defense fees, regardless of whether you win or lose. Without D&O coverage, you pay these costs from personal savings or force your startup to drain cash reserves during the most critical growth phase. You face impossible choices: settle a meritless claim to avoid bankruptcy or fight it and risk personal financial ruin. The average startup D&O claim takes 18 to 24 months to resolve, meaning defense costs accumulate while your business struggles. Being named in a lawsuit doesn’t mean you did anything wrong-it means you’re liable for legal costs immediately, before any verdict is reached.

Personal Assets Are Always at Risk

Your incorporation documents don’t protect you from D&O claims. Investors suing over alleged revenue misrepresentation, employees claiming wrongful termination based on board decisions, or regulators investigating governance failures will target you personally as a director or officer. A Wells Notice from the SEC triggers defense-cost obligations that your company may refuse to cover if it views the claim as your personal liability. Side A coverage-the individual protection component of a D&O policy-shields your personal assets when the company can’t or won’t indemnify you. This protection matters most during funding rounds. Institutional investors expect D&O coverage before closing capital, and many term sheets explicitly require it. Without it, your lead investor walks away, and your Series A closes late or not at all.

Institutional Capital Creates Board Complexity

Once you raise institutional capital, your risk profile changes overnight. You now have fiduciary duties to investors, independent directors with their own legal exposure, and contractual obligations that reference governance standards. A venture capital firm investing $2 million demands D&O coverage with limits matching your funding level-typically $1 million to $2 million for early-stage rounds. If you’ve added independent directors to your board, those individuals won’t accept a seat without confirmation that D&O coverage protects them. Recruiting experienced talent to your board becomes nearly impossible if you can’t offer this protection. The underwriting process itself forces discipline: insurers ask tough questions about your cap table, option grants, financial projections, and governance practices. This scrutiny often surfaces risks you hadn’t considered, making D&O a governance improvement tool as much as a risk transfer mechanism.

Why Coverage Gaps Lead to Funding Delays

Investors conduct due diligence on your insurance stack before closing any round. They verify that your D&O policy covers the board members they’re adding, that Side A protection exists for individuals, and that coverage limits align with your valuation and capital raised. A missing or inadequate D&O policy can halt a term sheet for weeks while you scramble to secure coverage. Underwriters need time to evaluate your governance structure, so waiting until the last minute creates unnecessary friction. Companies that secure D&O early-even before formal board expansion-avoid these delays and signal to investors that you take governance seriously.

What Claims Actually Hit Startup Leadership

Employment Disputes Cost More Than You Expect

Startup founders often picture D&O claims as abstract legal risks, but the claims that land in real inboxes are specific and expensive. Employment disputes top the list. When you terminate an employee or restructure your team, that person’s lawyer files a wrongful termination claim alleging the board made discriminatory decisions or violated company policy. The defense costs start immediately-your insurer advances legal fees while the claim moves through discovery and depositions.

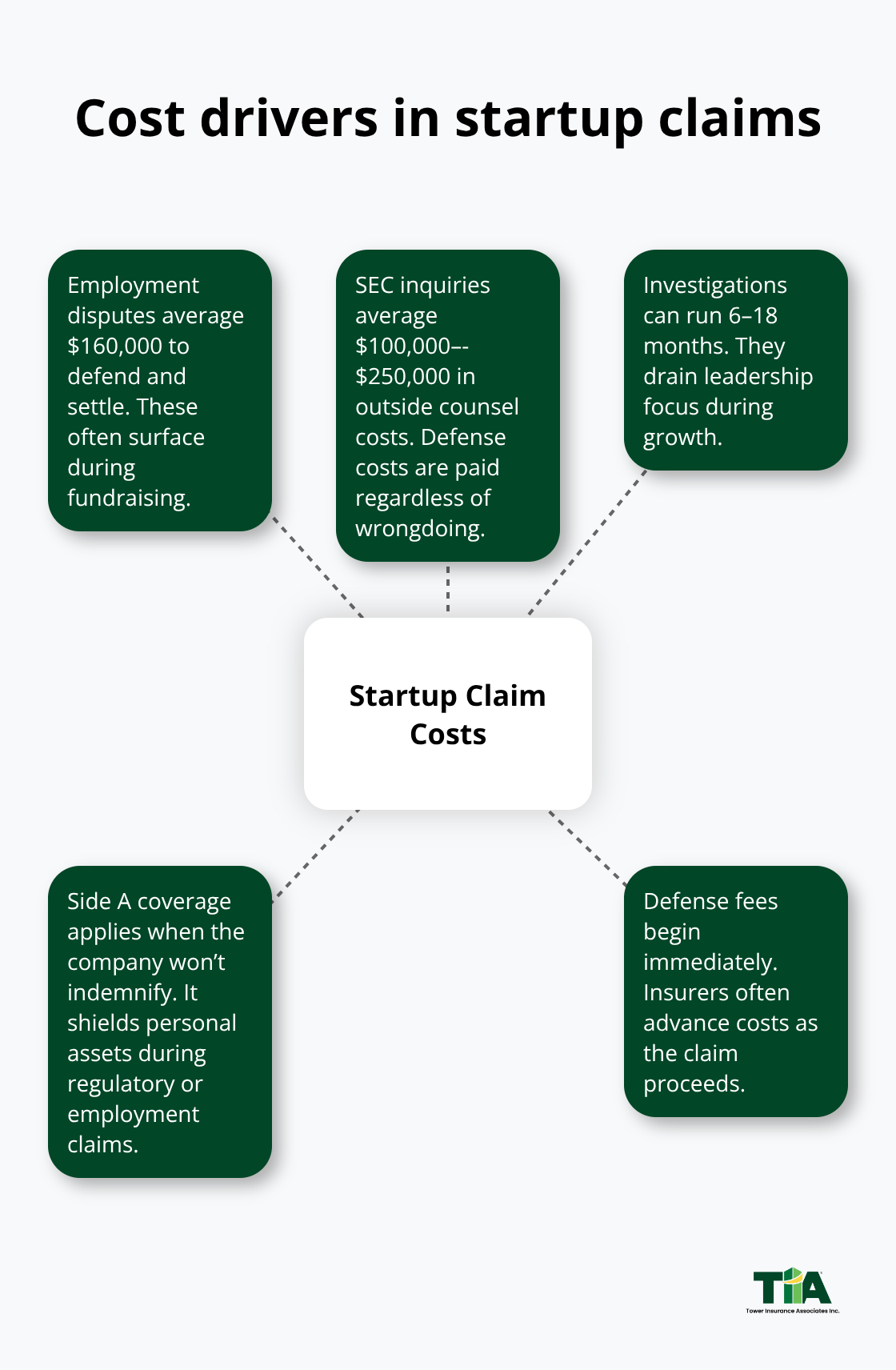

Employment disputes cost an average of $160,000 to defend and settle, according to employment law data. What makes this worse is timing: these claims often surface during funding rounds when your legal budget is already stretched. A Series A investor conducting due diligence discovers a pending employment claim and demands proof that D&O coverage exists. If you lack Side A protection, individual directors face personal liability if the company refuses indemnification because it views the claim as a governance failure rather than a personnel matter.

Fiduciary Duty Allegations Strike Fast and Hard

Breach of fiduciary duty allegations hit harder and faster than employment claims. An investor claims you misrepresented revenue projections during fundraising, or a co-founder alleges the board diluted their equity unfairly without proper authorization. These claims don’t require proof of intentional fraud-they require only that a director’s decision fell short of reasonable business judgment.

A Wells Notice from the SEC investigating governance practices or financial disclosure triggers immediate defense-cost obligations. Your company may decline to cover your legal defense if it believes the SEC investigation involves your personal conduct rather than company policy. Side A coverage protects you when indemnification disappears. Regulatory investigations are expensive: SEC inquiries average $100,000 to $250,000 in outside counsel costs for early-stage companies, with defense costs paid regardless of whether wrongdoing occurred.

The investigation itself can consume six to eighteen months, draining management attention during critical growth phases.

Compliance Failures Create Personal Director Liability

Compliance violations create a third category of claims that founders underestimate. As your startup grows, you accumulate contractual obligations that reference governance standards. Enterprise customers demand SOC 2 compliance or specific data-protection practices. Venture contracts require board independence or audit committee oversight. If your governance structure falls short and a customer sues, alleging breach of contract because you lacked promised governance controls, the claim names individual directors.

Regulatory pressure in industries like fintech or health-tech amplifies this exposure. A compliance failure that costs your company a customer contract also creates personal liability for the directors who approved the business decision. D&O coverage responds to these claims by covering defense costs and settlements when directors are sued for governance decisions that fell short of industry standards.

Why These Claims Derail Fundraising

The key insight is that these three claim categories-employment, fiduciary duty, and regulatory-aren’t theoretical. They’re the actual claims that shut down fundraising, distract leadership, and drain company cash. A pending employment dispute or regulatory inquiry signals to investors that your governance structure may have gaps. Institutional investors conduct deep due diligence on your insurance stack and any outstanding claims before closing capital. They want confirmation that D&O coverage protects the board members they’re adding and that Side A protection exists for individuals. Understanding what claims actually hit startup leadership helps you recognize why securing D&O coverage before your board expands or your first institutional capital closes prevents these claims from becoming personal financial emergencies. The next step is knowing how to evaluate the right policy for your specific stage and risk profile.

Sizing Coverage to Match Your Funding Stage and Risk

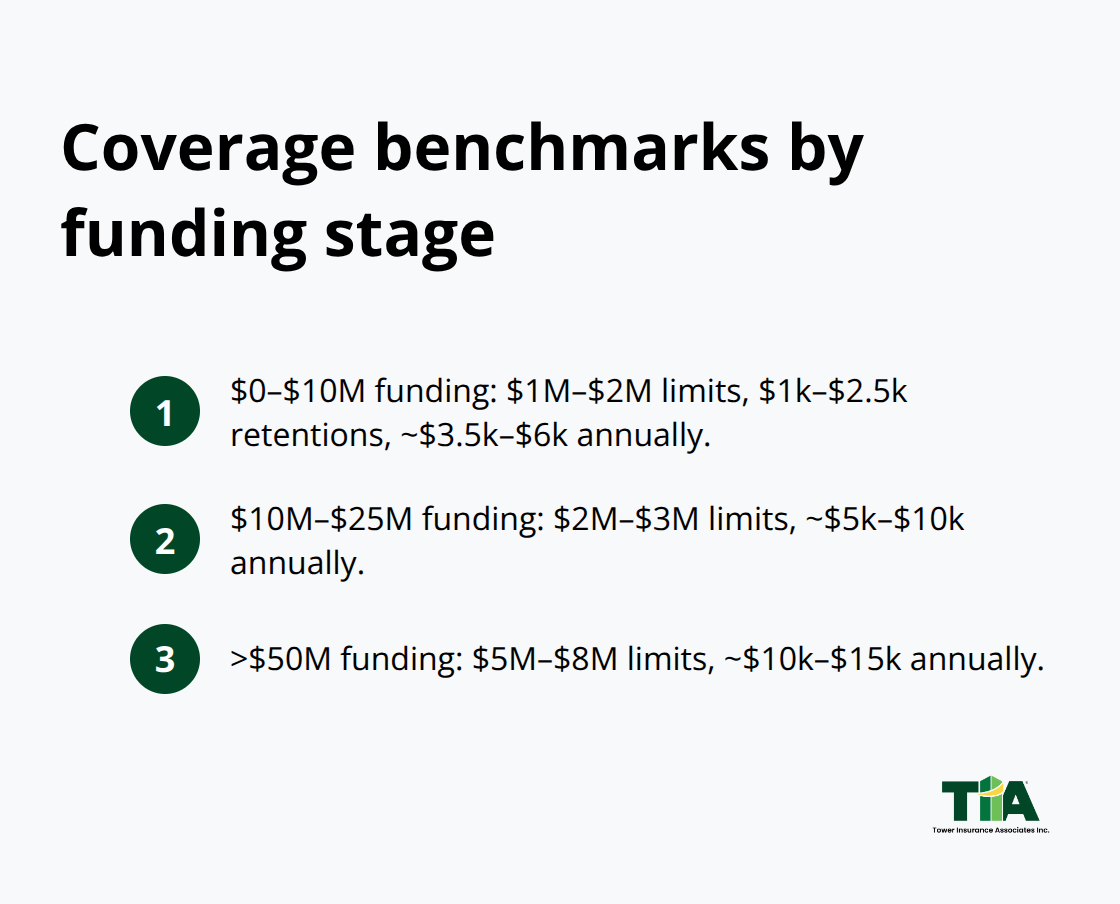

Choosing a D&O policy starts with a hard truth: there is no one-size-fits-all limit. Your coverage needs depend directly on how much capital you’ve raised, how many independent directors sit on your board, and what contractual obligations you’ve signed. Embroker’s startup pricing data shows clear correlation between funding level and appropriate limits. Companies with zero to ten million dollars in funding typically need one to two million dollars in coverage with retentions between one thousand and two thousand five hundred dollars, costing three thousand five hundred to six thousand dollars annually. Companies funded between ten and twenty-five million dollars should carry two to three million in limits with retentions of two to three million, paying five thousand to ten thousand dollars per year. Companies above fifty million in funding need five to eight million in limits with retentions matching or exceeding the lower end of that range, paying ten thousand to fifteen thousand dollars annually. These aren’t recommendations-they’re what institutional investors actually require before closing capital.

A Series A investor conducting due diligence will reject a policy with insufficient limits because it signals you underestimated your governance exposure.

Match Limits to Actual Risk, Not Premium Cost

The mistake most founders make is selecting limits based on premium cost rather than actual risk. A one million dollar limit saves three thousand dollars annually but becomes catastrophic when a regulatory investigation costs one hundred fifty thousand dollars in defense fees alone. Your policy must cover the full cost of defending against employment disputes, fiduciary duty allegations, and regulatory inquiries, plus settlement reserves. That means your limit must exceed your lead investor’s expectations, not match them. Institutional investors expect coverage that protects the board members they’re adding and reflects your company’s valuation and governance complexity. Underfunding your limit creates a false economy: you save money on premiums but expose yourself to personal liability when claims exceed your policy ceiling.

Retention Levels Determine Your Out-of-Pocket Exposure

The retention, or deductible, is where most founders face unexpected costs. A low premium with a high retention means you pay thousands in defense costs before coverage activates. Conversely, a high premium with a low or zero retention on Side A coverage means individual directors face zero out-of-pocket exposure when personal liability claims surface. Zero retention on Side A protects individual directors when employment disputes or regulatory inquiries arrive. Side B and Side C typically carry retentions of twenty-five thousand to fifty thousand dollars, which your company pays when indemnifying directors or defending entity-level claims. This structure matters operationally: when a Wells Notice arrives, your individual directors need immediate legal representation without worrying about who pays the first twenty-five thousand dollars in fees. That friction disappears with zero Side A retention. For companies between seed and Series A, a retention structure of zero on Side A and twenty-five thousand on Side B and Side C provides adequate protection without inflating premiums. As you scale beyond Series A, you may negotiate higher retentions in exchange for broader coverage or lower premiums, but only if your balance sheet can absorb fifty thousand dollar retentions without operational disruption. Zero Side A retention adds roughly one thousand to two thousand dollars annually to your premium but eliminates personal liability exposure for individual directors during the claims process.

Carrier Track Record with Startups Predicts Claims Handling Speed

Not all D&O carriers treat startup claims equally. Some carriers specialize in mature companies and treat startup claims as statistical anomalies, delaying defense-cost advancement and creating friction during underwriting. Others have built underwriting processes specifically for early-stage companies and understand that founders need same-day binding during funding rounds and fast claims support when disputes surface. The difference is material. A carrier accustomed to public-company D&O claims will ask for extensive governance documentation, board minutes, and financial projections before issuing a quote. A startup-focused carrier recognizes that pre-Series A companies often lack formal board documentation and adjusts underwriting accordingly. When evaluating carriers, ask directly: how many startup D&O claims have you closed in the past twelve months, and what was the average time from claim notice to first defense-cost advancement? Carriers with strong startup track records answer this in minutes. Carriers uncomfortable with early-stage risk will deflect or quote long timelines. A carrier that closed fifteen startup claims last year and advanced defense costs within five business days on average is materially different from one that handles three startup claims annually and takes three weeks to advance costs. This distinction becomes critical when you’re managing an SEC Wells Notice or defending an employment dispute during a fundraising process. Speed of claims handling should weight equally with premium cost in your decision.

Final Thoughts

D&O for startups protects your personal assets when employment disputes, investor allegations, or regulatory inquiries surface. Without coverage, a single claim drains your personal savings and derails your company’s growth during critical fundraising windows. The disputes we’ve outlined-wrongful termination, breach of fiduciary duty, and compliance failures-hit founder desks as real legal bills, not hypothetical risks, and they cost money to defend regardless of merit.

Your coverage needs shift as your startup scales from seed to Series B. Institutional investors won’t close capital without adequate D&O protection, and independent directors won’t join your board without confirmation that coverage protects them personally. This means your policy must evolve alongside your funding rounds and board expansion, with limits and retention structures that match your actual governance exposure rather than your budget constraints.

The carrier you select matters as much as the limits you choose. A startup-focused carrier with a track record of fast claims handling will advance defense costs quickly when disputes surface, while a carrier accustomed to mature companies creates friction during underwriting and delays when you need speed most. At Tower Insurance Associates, Inc., we represent multiple top-rated carriers and work with you to match your coverage to your specific stage and risk profile-contact us today to discuss how D&O protection fits into your broader insurance strategy.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.