Nonprofit board members face real legal and financial exposure that many organizations overlook. D&O liability for nonprofits protects your directors and officers from personal liability when they’re sued for decisions made in their official capacity.

At Tower Insurance Associates, Inc., we’ve seen how the right coverage can be the difference between a manageable situation and a crisis that threatens your mission. This guide walks you through what you need to know to protect your board and organization.

What D&O Liability Actually Covers for Nonprofit Leaders

D&O liability insurance protects nonprofit directors and officers from personal financial exposure when they face lawsuits for actions taken in their governance roles. The coverage pays for defense costs, settlements, and judgments-expenses that can easily reach significant amounts. Without this coverage, board members risk depleting personal savings to cover legal fees, even when they acted in good faith. The policy covers claims alleging errors in judgment, breach of fiduciary duty, misleading statements, or misuse of funds or authority. Defense costs often represent the largest expense in D&O claims, and many states’ charitable immunity laws fail to shield these expenses-meaning personal assets remain exposed regardless of whether the organization ultimately pays damages.

Why Nonprofit Claims Occur at Higher Rates

Nonprofits face lawsuits at roughly twice the rate of public or private companies, according to Travelers. Claims originate from vendors, donors, employees, competitors, and government regulators-creating multiple exposure points board members cannot fully control. Employment practices allegations account for a significant portion of D&O claim dollars, making hiring, firing, and workplace policy decisions primary risk areas. Governance decisions on program oversight, fundraising, budgeting, and major complaints also trigger litigation. A single employment practices claim can cost substantial amounts in defense alone before any settlement or judgment. The nonprofit sector includes roughly 1.5 million registered organizations managing significant annual revenue, creating substantial aggregate liability exposure.

The Three Fiduciary Duties That Expose Board Members

Board members carry three core fiduciary duties: care, loyalty, and obedience. The duty of care requires directors to act with ordinary, reasonable judgment and in the organization’s best interests-a standard that protects leaders when they prepare thoroughly, deliberate thoughtfully, and document decisions. The duty of loyalty demands undivided allegiance and full disclosure of conflicts of interest; violating this duty through self-dealing or usurping organizational opportunities creates direct personal liability. The duty of obedience requires adherence to bylaws, policies, and applicable laws. Willful ignorance or intentional wrongdoing cannot be shielded by insurance or indemnification. State attorneys general can enforce these duties against individual board members, and enforcement actions expose personal assets.

How Claims Challenge Good-Faith Decisions

D&O insurance becomes essential because even good-faith decisions can be challenged in court, forcing expensive legal defense regardless of eventual outcome. Many board members lack formal governance training and may not understand their fiduciary duties, increasing claim likelihood. A director who votes on a hiring decision, approves a major contract, or oversees program operations can face personal liability if a plaintiff alleges the decision breached a fiduciary duty. The cost to defend such a claim-whether the board member ultimately prevails or not-falls on personal finances without D&O coverage. Courts examine whether directors prepared adequately, considered available information, and acted in the organization’s interest, not their own. This scrutiny means that poor judgment alone may not trigger liability, but inadequate preparation or conflicts of interest can expose personal assets to significant risk.

Understanding what D&O liability covers is the first step toward protecting your board. The next section examines the specific financial and reputational risks nonprofits face when coverage is inadequate or absent.

Real Risks Nonprofits Face Without Adequate Coverage

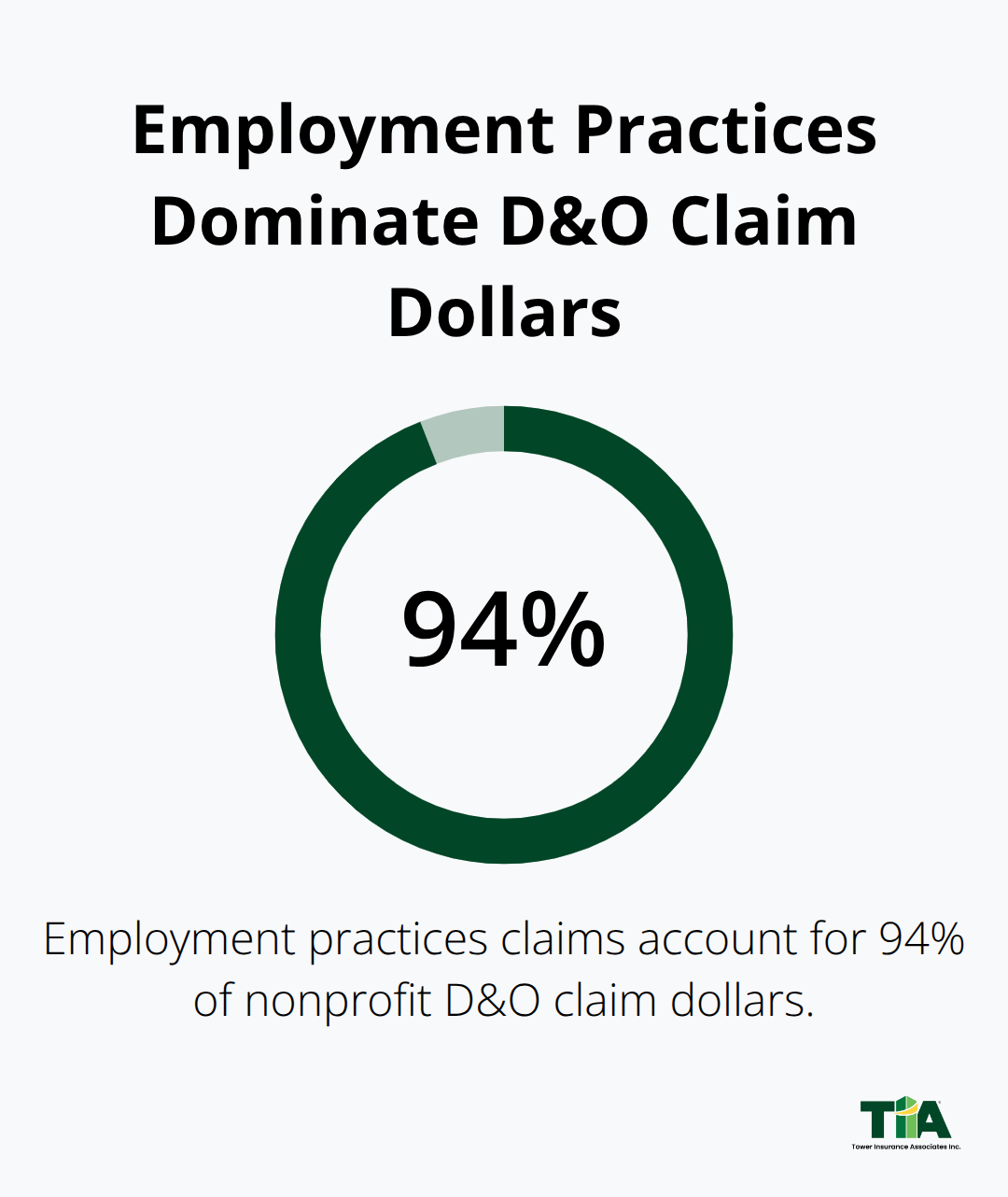

Employment practices claims represent the largest financial threat to nonprofit boards, accounting for roughly 94% of D&O claim dollars across the sector. A single wrongful termination allegation, discrimination claim, or harassment lawsuit can cost $85,000 to $300,000 in defense expenses alone before any settlement or judgment materializes. Without D&O coverage, these defense costs come directly from the nonprofit’s operating budget or board members’ personal finances.

Most judgments ultimately fall to the organization itself, but defense expenses often fall outside coverage or deplete organizational reserves meant for mission work. Employment practices claims frequently involve multiple defendants-the nonprofit, the executive director, and individual board members-multiplying legal fees across the organization. A nonprofit that skips D&O insurance to save premium costs typically faces exponentially higher expenses when litigation arrives. Donors and funders scrutinize how organizations spend money, and diverting operating funds to legal defense signals poor governance and mission misalignment, eroding stakeholder confidence before any verdict is reached.

Defense Costs Hit Hardest When Coverage Lapses

Defense costs represent the most predictable and devastating expense in D&O claims. Many state charitable immunity laws explicitly fail to protect against defense expenses, leaving personal assets exposed even when the nonprofit ultimately prevails in court. A board member defending against allegations of breach of fiduciary duty or misuse of authority faces legal bills that accumulate regardless of the claim’s merit. Without insurance, that board member must hire personal counsel, creating a conflict with the nonprofit’s defense strategy and doubling legal costs. Reputational damage compounds the financial exposure. Claims alleging mismanagement, governance failures, or improper fund use spread quickly through donor networks and community channels. Foundations and major donors withdraw support when litigation becomes public, and grant-making organizations scrutinize governance after claims surface. Recovery from reputational damage takes years and requires substantial investment in communications, governance reforms, and relationship rebuilding.

Reputation Damage Extends Beyond Legal Bills

The combination of legal expenses and mission disruption transforms a single claim into an existential threat for organizations without adequate coverage. Nonprofits without D&O insurance often struggle to attract experienced board members. Qualified candidates increasingly demand to understand liability protection before accepting board positions. A nonprofit that cannot offer D&O coverage signals financial weakness and governance risk, deterring the very leaders the organization needs. This creates a cycle where weaker governance attracts more claims, which drives up insurance costs or forces the organization to operate uninsured. The Volunteer Protection Act offers limited immunity to volunteers but provides no defense cost coverage and excludes directors and officers in most circumstances. Relying solely on this federal law leaves substantial personal exposure unaddressed.

Why Board Recruitment Suffers Without Protection

Organizations that invest in D&O insurance demonstrate commitment to protecting leaders and mission stability, making board recruitment measurably easier and strengthening governance quality over time. The financial and reputational consequences of uninsured claims create pressure that extends far beyond the courtroom. When a nonprofit faces litigation without coverage, the organization must choose between depleting reserves for legal defense or forcing board members to shoulder personal financial risk. Either path weakens the organization’s ability to pursue its mission and signals to potential donors and partners that governance is unstable. The next section examines how to select D&O coverage that actually matches your nonprofit’s risk profile and protects both your board and your organization’s future.

Matching Coverage to Your Nonprofit’s Real Risk Profile

Selecting D&O coverage requires moving beyond generic nonprofit packages and building a policy around your organization’s specific exposure. Most nonprofits make the mistake of choosing coverage based solely on cost or accepting whatever their current broker recommends without scrutiny. This approach leaves critical gaps that become painfully obvious only when a claim arrives.

Identify Your Organization’s Highest-Risk Activities

Start with identifying which activities create the highest litigation risk in your organization. If your nonprofit has grown to 10 or more staff members, employment practices liability deserves substantial coverage limits. If your organization manages federal grants or government contracts, misuse allegations carry severe penalties and personal liability exposure for leadership. Program oversight decisions in youth services, healthcare, or community development organizations face heightened scrutiny from regulators and affected parties. Fundraising activities create donor disputes and restricted fund misallocation claims. Your organization’s size matters far less than the specific activities and decision-making authority your board exercises.

A small environmental nonprofit with aggressive advocacy campaigns faces different risks than a food bank managing volunteer operations. An independent agent who works regularly with nonprofits can help you map these exposures and avoid underinsuring areas where claims are most likely. Working with generalist commercial brokers often results in one-size-fits-all policies that leave dangerous blind spots. We recommend nonprofits demand a risk assessment conversation before purchasing any policy. This conversation should address your board structure, governance practices, program activities, staffing levels, fundraising methods, and any current or past disputes.

Set Coverage Limits and Deductibles That Match Your Exposure

Coverage limits and deductibles require careful calibration rather than guesswork. Most nonprofits with annual budgets under $5 million should carry minimum limits of $1 million per claim and $2 million aggregate, though organizations managing federal funds or serving vulnerable populations often need $2 million per claim and $3 million aggregate to adequately protect against serious allegations. Deductibles of $10,000 to $25,000 work well for most nonprofits because they reduce premiums while remaining manageable if a claim requires out-of-pocket payment. Higher deductibles sound attractive until your organization faces a real claim and discovers the cash flow impact of paying $50,000 or more before insurance responds.

Defense costs represent the largest expense in most claims, and your policy language must specify whether defense costs reduce your policy limits or sit outside them. This distinction dramatically affects your actual protection. A $1 million policy with defense costs inside the limit may provide only $600,000 for settlements and judgments after defense expenses consume $400,000. The same $1 million policy with defense costs outside the limit protects your full $1 million for settlement and judgment while the insurer pays defense costs separately. Most nonprofit D&O policies include defense costs inside the limit, which means you must understand this trade-off when selecting coverage amounts. Ask your broker explicitly whether defense costs are inside or outside limits before committing to any policy.

Understand Policy Exclusions and Coverage Gaps

Policy exclusions matter intensely because they determine what claims actually receive coverage. Standard exclusions eliminate coverage for intentional wrongdoing, fraud, bodily injury, property damage, and contractual liability. Some policies exclude employment practices claims unless you add them as a separate endorsement, which defeats the purpose of purchasing D&O coverage at all. Others exclude claims arising from violations of securities laws or pension regulations. Your broker should walk you through every exclusion and explain how it affects your organization. If your nonprofit operates in multiple states, verify that the policy covers directors and officers in all states where your organization operates, because some carriers limit coverage to specific states.

Partner with Agents Who Understand Nonprofit Operations

The right agent makes the difference between adequate coverage and expensive gaps. Nonprofit-focused independent agents understand governance structures, fiduciary duty nuances, and common claim patterns in your sector far better than commercial brokers who spend most of their time insuring for-profit companies. These agents can explain why a museum faces different D&O risks than a homeless services organization and help you avoid purchasing coverage that excludes your primary exposures. They also maintain relationships with insurers willing to write nonprofit business and can negotiate better rates and terms based on your governance quality.

Agents who know nonprofits also help you document risk controls that lower premiums over time. Strong governance practices, clear conflict-of-interest policies, annual director training, and robust financial oversight signal reduced risk to underwriters and often result in rate reductions after you demonstrate sustained good governance practices.

Final Thoughts

D&O liability for nonprofits represents a real financial and reputational threat that demands immediate attention rather than postponement until a claim arrives. Board members who understand their fiduciary duties and operate within strong governance frameworks reduce claim likelihood substantially, yet even the most careful leaders face lawsuits that require expensive legal defense. The right D&O coverage protects both your organization’s mission and the personal assets of the directors and officers who volunteer their time to lead.

Start by reviewing your current D&O policy with fresh eyes and examining what defense costs your coverage includes, which exclusions apply to your organization, and whether your limits match your actual exposure. Schedule a conversation with an independent agent who works regularly with nonprofits and understands the specific risks your organization faces (your agent should walk you through a risk assessment tailored to your board structure, programs, and decision-making authority rather than applying generic nonprofit benchmarks). If your nonprofit manages federal grants, serves vulnerable populations, or employs more than a handful of staff, your current limits may expose your board to unacceptable personal risk.

Beyond insurance, invest in governance practices that prevent claims from arising in the first place-annual board orientation covering fiduciary duties, conflict-of-interest procedures, and employment law basics signals to underwriters that your organization takes risk seriously and often results in lower premiums over time. At Tower Insurance Associates, Inc., we work with nonprofits to build D&O coverage that actually matches their risk profile and protects what matters most.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.