One missed deadline. One procedural error. One overlooked conflict of interest-and your law firm faces a claim that could cost hundreds of thousands of dollars. Lawyers professional liability insurance protects you when things go wrong, but most attorneys don’t fully understand what their coverage actually includes.

At Tower Insurance Associates, Inc., we’ve seen too many legal professionals operate with gaps in their protection. Standard business policies won’t cut it for law practices, and the wrong policy type can leave you exposed when you need coverage most.

What Lawyers Professional Liability Insurance Actually Covers

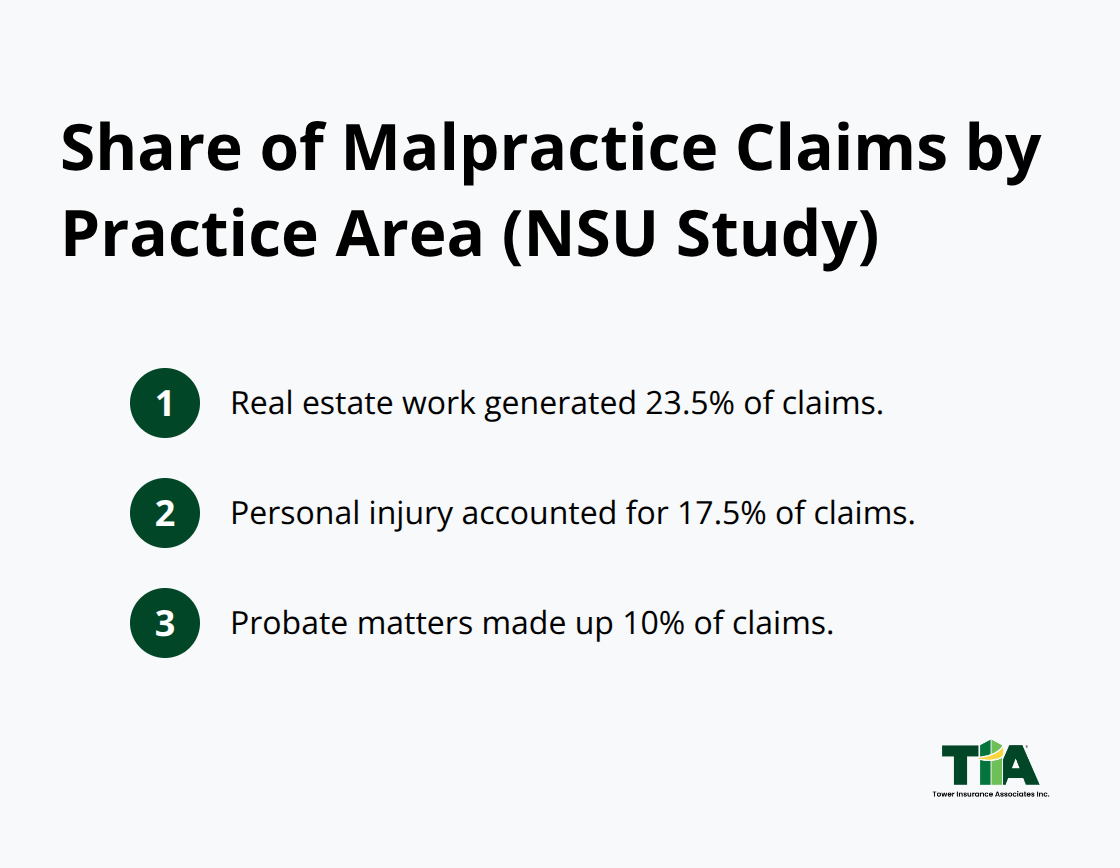

Professional liability insurance for lawyers protects against financial losses when clients claim you made an error, missed a deadline, gave negligent advice, or failed to act on their behalf. This coverage pays for defense costs, settlements, and judgments-not bodily injury or property damage, which fall under general liability. The distinction matters enormously. A standard commercial general liability policy covers if someone trips in your office and breaks a leg. It does not cover if you miss a statute of limitations, draft a contract incorrectly, or overlook a conflict of interest. According to the NSU study analyzing 4,533 malpractice claims from 100 Florida insurers over 44 years, the average payout per claim reached $154,139, with insurers paying out on 70.1% of claims. Real estate work generated 23.5% of those claims, personal injury 17.5%, and probate 10%.

The most common errors cited were missed statute of limitations or deadline errors at 8.6%, lack of diligence at 8.4%, and negligent drafting at 7.6%. These aren’t rare edge cases-they’re the daily risk of legal practice.

How Claims-Made Policies Work

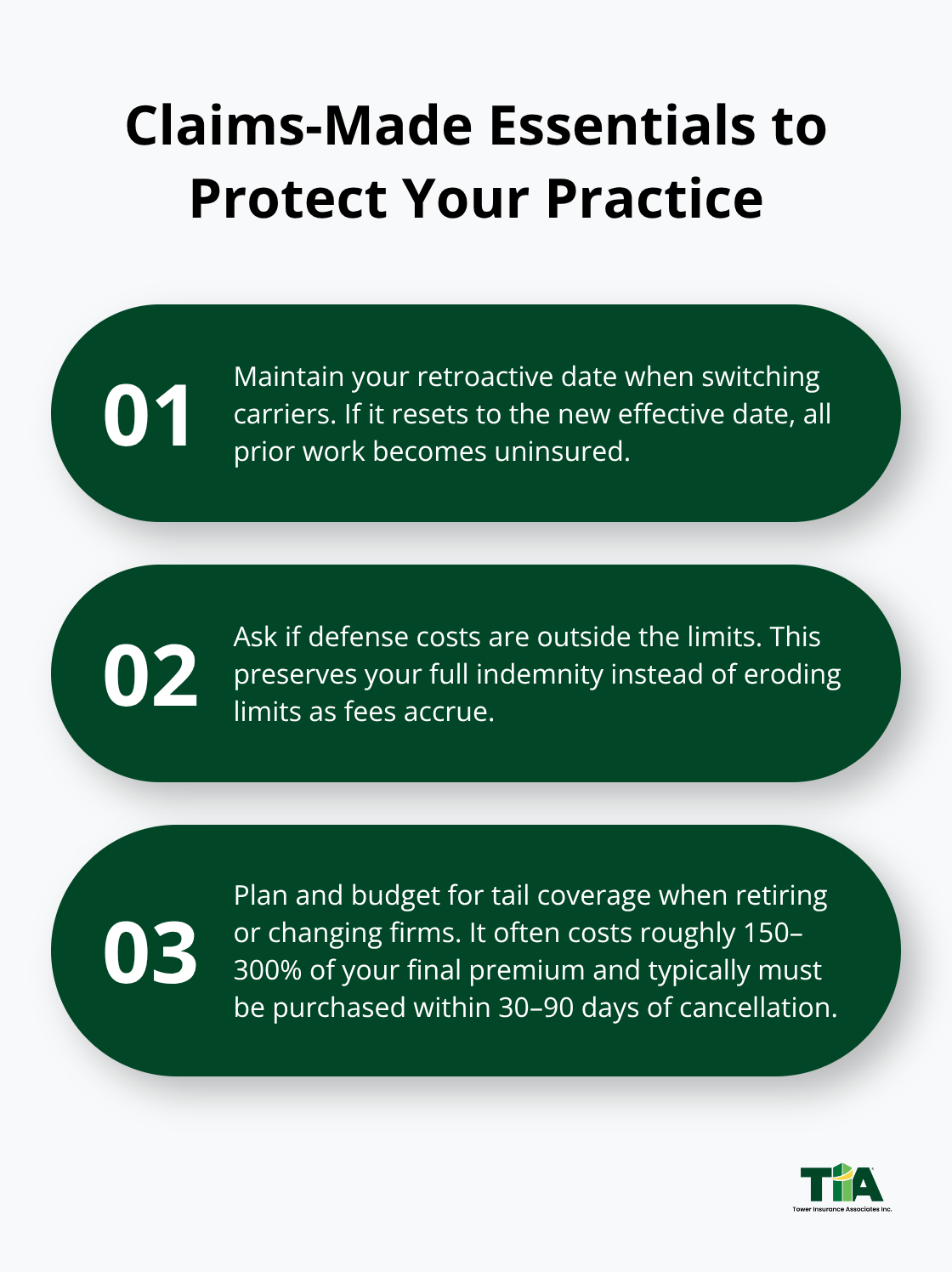

Professional liability for lawyers operates almost exclusively as claims-made coverage, not occurrence-based. This means the policy must be active when a claim is reported, not when the error occurred. If you switch carriers or retire without tail coverage, claims from prior work go uninsured. A lawyer with 22 years of experience on average faces this exposure, and the NSU data showed that lawyers paid an average out-of-pocket deductible of $11,757, though 24% paid nothing. The policy’s retroactive date marks the earliest date for covered work; losing this date when changing insurers creates a gap. Defense costs typically come from your policy limit, eroding the amount available for settlement or judgment. Some carriers offer defense costs outside the limit, which preserves your full indemnity. You must ask this question directly when comparing policies because the difference can mean the gap between protecting your firm and facing personal liability.

Why General Liability Falls Short

Standard business policies exclude professional services entirely. Insurers know legal work creates financial risk that general liability does not cover. The American Bar Association notes that higher-risk practice areas include securities, intellectual property, trusts and estates, personal injury, and loan modifications. If your firm handles any of these, a general liability policy provides zero protection for client claims. Even firms handling lower-risk areas face exposure. The NSU study found that sole practitioners represented 50.5% of claims, meaning one-person shops carry significant risk.

A general liability policy will not cover missed deadlines, inadequate research, conflicts of interest, or mismanagement of client funds. It also will not cover regulatory investigations or disciplinary proceedings that can follow a malpractice claim. You need professional liability coverage designed for legal services, with limits aligned to your case complexity and revenue. Most firms carry $1 million in limits, but that amount often proves insufficient for defense costs alone in complex matters.

The gaps in standard coverage become apparent only when a claim arrives. Your next step involves understanding which specific claims threaten your practice most and how your current policy responds to them.

Common Claims That Drain Your Firm’s Resources

Missed Deadlines: The Most Expensive Error

Missed statute of limitations deadlines represent the single largest claim driver in legal malpractice. According to the NSU study of 4,533 Florida malpractice claims spanning 44 years, deadline errors accounted for 8.6% of all claims, making them the most common error type alongside lack of diligence at 8.4%. These aren’t abstract risks. A real estate closing that slips past a contract deadline costs your client thousands in damages. A personal injury case where you miss the statute of limitations window eliminates the entire claim. Your policy covers this, but only if you have adequate limits and understand how defense costs consume your coverage.

Many attorneys assume their $1 million policy provides robust protection, yet a single complex matter with expert witnesses, depositions, and discovery can exhaust half that limit before trial. The financial pressure mounts quickly. Your E&O policy pays for counsel, expert witnesses, and court costs as the claim progresses. Once those defense expenses hit $500,000, your remaining $500,000 must cover any settlement or judgment. A modest settlement of $300,000 leaves you with only $200,000 in coverage for future claims that year. This reality forces many firms to carry higher limits or face uninsured exposure.

Drafting Errors and Professional Mistakes

Negligent drafting represented 7.6% of claims in the NSU data, often involving contract language gaps, boilerplate errors, or failure to include necessary provisions. A single word omitted from a trust document or a misplaced clause in a commercial lease creates liability that your general liability policy explicitly excludes. Your E&O policy covers the defense and damages, but the financial and reputational cost remains substantial. Clients who discover errors months or years later pursue claims that force you to defend work product from years past.

These errors compound when they affect multiple clients or transactions. A template error that appears in five contracts creates five separate claims. The NSU study found that lawyers with approximately 22 years of experience still faced malpractice exposure, indicating that experience alone does not prevent drafting mistakes. Systematic review processes, checklists, and quality control reduce these errors far more effectively than relying on individual attorney diligence.

Inadequate Research and Securities Exposure

When you give advice based on incomplete research or outdated case law, clients suffer financial loss and pursue claims against you. The American Bar Association identifies securities, intellectual property, and trusts and estates as the highest-risk practice areas partly because the research demands are intense and the cost of error is enormous. A securities advice mistake can cost a client six figures. An IP filing error may result in loss of trademark rights worth millions to a business. Your E&O policy covers this exposure, but only if your coverage limits align with the potential damages.

These high-value claims require higher policy limits than standard $1 million coverage provides. Firms handling securities work or complex IP matters should carry $2 million to $5 million in limits to match their actual exposure. The cost of higher limits pales against the cost of defending a $500,000 claim with only $1 million in total coverage.

Conflicts of Interest: The Hidden Exposure

Conflicts of interest claims operate differently from other malpractice claims. These arise when you represent two parties with opposing interests or fail to disclose a relationship that creates a conflict. The American Bar Association identifies them as a persistent threat. Conflicts claims often involve ethical violations alongside malpractice, meaning both your E&O policy and your bar association face scrutiny. Defense costs spike because counsel must address both the malpractice claim and the ethics complaint simultaneously.

Your engagement letters should clearly identify conflicts checks and client consent, yet many solo practitioners and small firms skip this step. The cost of implementing a conflicts management system-whether through practice management software or manual tracking-runs far below the cost of defending a conflicts claim. Firms handling complex corporate work or IP matters face higher conflict exposure and should carry higher limits accordingly. The next section examines how your policy structure determines whether you have adequate protection when these claims arrive.

What Policy Type Actually Protects Your Practice

Claims-Made Policies and the Retroactive Date Trap

Claims-made policies dominate the legal malpractice market for a reason: they cost less upfront and insurers manage them more easily. But this policy structure creates a trap that catches most attorneys off guard. Your policy only covers claims reported while the policy is active, not when the error occurred. Miss a deadline in 2024, get sued in 2026, and if you’ve switched carriers or let coverage lapse, that claim sits completely uninsured. The American Bar Association and National Association of Insurance Commissioners both warn that lawyers must maintain their retroactive date when changing policies to avoid exactly this gap. If your retroactive date resets to your new policy’s effective date, all prior work becomes uninsured. This reality forces you to either stay with your current carrier indefinitely or pay for tail coverage when you leave.

Your retroactive date marks the earliest date for covered work. Losing this date when changing insurers creates a coverage gap that no amount of new insurance can fix. An independent insurance agency like Tower Insurance Associates, Inc. can help you navigate this transition and preserve your retroactive date with a new carrier, protecting work from years past.

Occurrence-Based Policies: A Rare Alternative

Occurrence-based policies cover incidents during the policy period regardless of when the claim arrives, eliminating the timing problem entirely. They cost more initially but offer genuine peace of mind if you plan to retire or change firms. Most lawyers don’t have this choice because occurrence policies for legal services are increasingly rare in today’s market. The higher upfront cost and longer tail of liability make these policies unattractive to insurers, so few carriers offer them for law practices. If your firm can locate an occurrence-based policy, the extra premium may prove worthwhile for the simplicity and protection it provides.

Cyber Liability: The Excluded Exposure

Cyber liability represents the fastest-growing exposure for law firms and most standard E&O policies exclude it entirely. When ransomware hits your systems, client data breaches, or your files get encrypted, your malpractice policy won’t pay for notification costs, regulatory fines, or breach response. According to the Insurance Information Institute, data privacy risk is rising sharply for law practices handling sensitive client information. A single breach can cost $50,000 to $500,000 in notification, credit monitoring, and regulatory penalties before any malpractice claim even exists. You need a standalone cyber liability policy or an endorsement to your E&O that covers data breach response, network security liability, and privacy violations. This isn’t optional for firms using cloud storage or handling IP, real estate transactions, or estate planning work.

Tail Coverage: Planning for Retirement or Firm Changes

Tail coverage requires immediate attention if you’re planning retirement or selling your practice. This extended reporting period lets you report claims after your policy ends, typically for three to five years. Without it, a claim filed against you after retirement sits completely uninsured. The cost of tail coverage runs roughly 150 to 300 percent of your final annual premium, a substantial expense that catches many lawyers by surprise.

Budget for this cost years in advance if you plan to exit practice, and confirm your carrier’s tail provisions in writing before you need them. Most policies require you to purchase tail coverage within 30 to 90 days of policy cancellation, so waiting until retirement month means paying whatever price your carrier quotes with no negotiation room.

Final Thoughts

Choosing the right lawyers professional liability insurance starts with honest assessment of your practice. Define every service you offer, identify your highest-risk practice areas, and calculate realistic case values based on your client base. A real estate firm handling $2 million transactions needs different limits than a solo practitioner handling simple wills, and most firms carrying $1 million in limits discover too late that defense costs alone consume half that amount in complex matters.

Reducing claims requires systematic risk controls that cost far less than defending a single malpractice case. Implement strong engagement letters that clearly define scope, fees, and conflicts checks, use practice management software to track deadlines and flag statute of limitations dates automatically, and conduct regular audits of trust accounting and client fund management since mishandling client money generates some of the costliest claims. These controls won’t eliminate claims entirely, but they reduce frequency and severity substantially.

Working with an experienced insurance advisor transforms your E&O program from a compliance checkbox into genuine protection. An independent agency like Tower Insurance Associates, Inc. represents multiple carriers and can compare policy terms, exclusions, and pricing across options you wouldn’t find alone, help you navigate claims-made policy transitions, and add cyber liability endorsements that standard policies exclude. Visit Tower Insurance Associates, Inc. to discuss your professional liability insurance needs and ensure your coverage matches your actual risk.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.