One mistake in your professional work can cost thousands in legal fees and settlements. At Tower Insurance Associates, Inc., we see how quickly a single error derails careers and damages reputations.

E&O insurance in Culver City protects you when clients claim you failed to deliver the standard of care they expected. Whether you’re an architect, doctor, lawyer, or consultant, this coverage is your financial safety net.

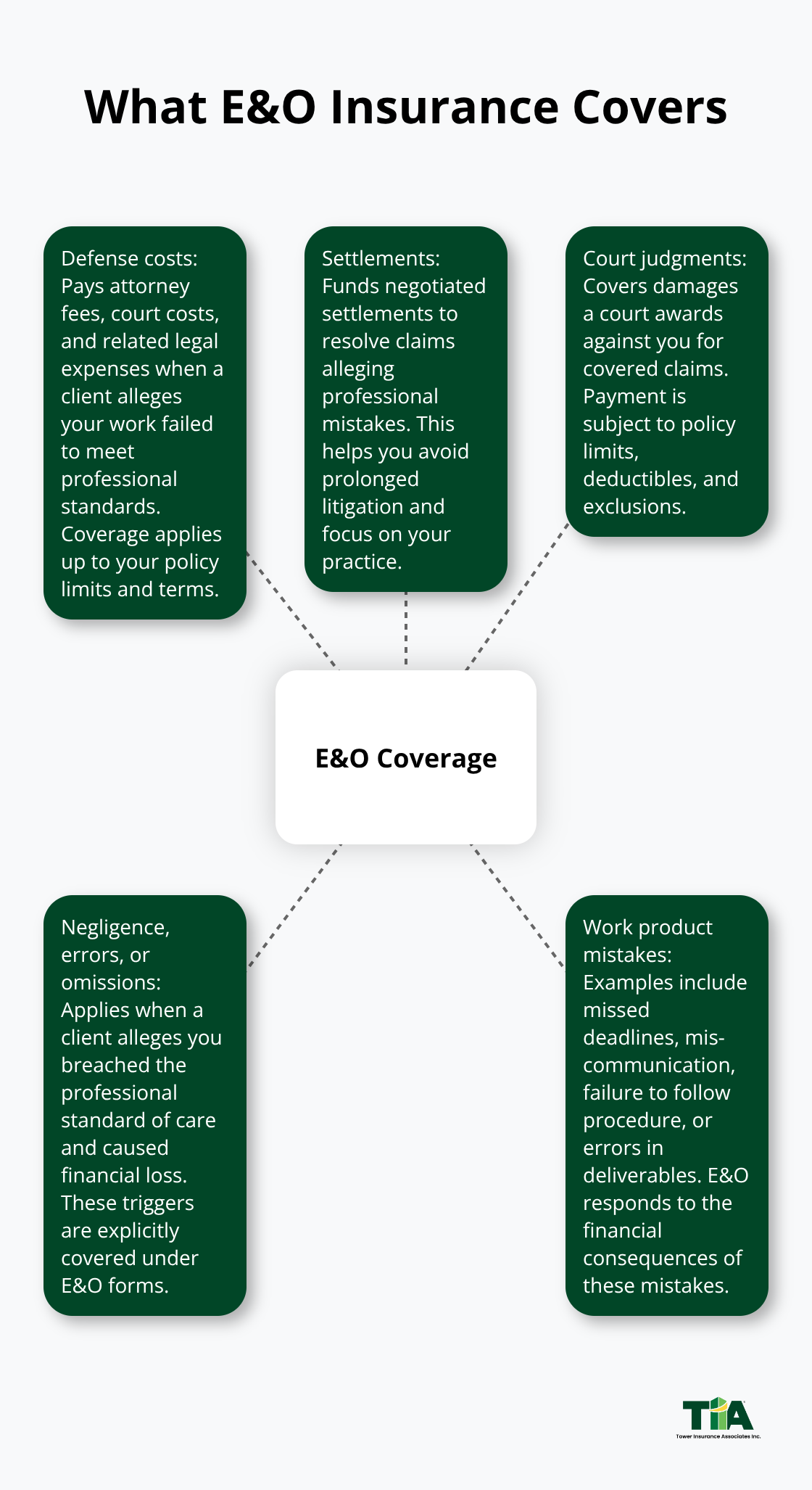

What E&O Insurance Actually Covers

Errors and Omissions insurance pays for the costs that follow when a client claims you failed to meet professional standards in your work. The National Association of Insurance Commissioners notes that E&O covers defense costs, settlements, and court judgments arising from allegations of negligence, errors, or omissions in your professional services. When a client sues and claims financial loss because of your mistake-a missed deadline, miscommunication, failure to follow procedure, or error in your work product-E&O steps in to cover your legal defense and any damages awarded.

How Claims-Made Coverage Works

The coverage operates on a claims-made basis, meaning it protects claims filed during your policy period, as long as the work occurred after your retroactive date. This distinction matters because if you switch insurers without tail coverage, you lose protection for work done under your old policy even if a claim arrives years later. A tail policy (also called extended reporting period coverage) extends your protection after you leave a carrier, covering claims that arrive after your policy ends for work you completed while insured. Without it, you face a coverage gap that can expose you to significant financial risk.

Why E&O Differs from General Liability

General Liability covers bodily injury and property damage. If a client trips in your office and breaks an arm, or your equipment damages their property, GL responds. E&O protects against financial losses from your professional mistakes. A lawyer who misses a filing deadline, a consultant who provides faulty advice, or an architect whose design flaw costs a client money-these situations demand E&O, not GL. Many professionals wrongly assume GL covers their work errors and discover the gap only after a claim arrives. Some policies bundle both coverages, but they work independently; you need both to avoid exposure.

Real Limits Matter for Your Practice

Coverage limits should reflect your annual revenue, the number of clients you serve, and the potential cost of defending a claim. A sole practitioner consultant might carry $1 million in coverage, while a firm with dozens of clients should consider $2 million or higher. Defense costs can exceed $100,000 quickly in professional liability litigation, and that amount comes from your policy limits unless your form includes a separate defense cost provision outside the limit. Check whether your policy covers defense costs within or outside your limits-this detail determines how much actual coverage remains for settlements. The U.S. Small Business Administration recommends that you review your coverage annually because your risk profile changes as your practice grows or your service mix shifts.

What Happens When You File a Claim

When a claim arrives, you must notify your insurer promptly and preserve all records related to the matter. Do not admit fault before consulting with counsel, as your words can affect the claim outcome. Your insurer will assign a defense attorney and manage the legal process while you focus on your business. The speed and quality of your insurer’s claims handling directly impact your stress level and your ability to move forward. This is where working with an independent agent who represents multiple top-rated carriers becomes valuable-you gain access to insurers known for responsive claims service and fair settlements in your industry.

Who Needs E&O Insurance in Culver City

Professionals Who Face Real Client Claims

Professionals in Culver City who provide services, advice, or specialized work face real exposure to client claims. The U.S. Small Business Administration identifies architects, engineers, consultants, medical professionals, real estate agents, brokers, and legal professionals as occupations that absolutely require E&O coverage. These roles share a common risk: clients depend on your expertise, and any gap between what they expected and what you delivered can trigger a lawsuit. A design flaw costs money. A missed deadline in a legal matter costs money. A diagnostic error costs money. In each case, the client claims financial loss from your professional mistake, and without E&O, you pay defense costs and damages from personal funds or business reserves. This is not theoretical risk. The National Association of Insurance Commissioners reports that professional liability claims are filed regularly across these sectors, and defense costs alone can reach six figures before a settlement is even discussed.

Why Architects and Engineers Need Coverage

Architects and engineers face particular exposure because their work directly impacts construction budgets and project timelines. A specification error or design miscalculation triggers change orders worth thousands or delays a project for months, and clients will demand compensation. Your clients hire you for technical precision, and they hold you accountable when calculations or specifications fall short of industry standards. The financial stakes are high because construction projects involve multiple parties and contractual obligations that flow through your work product.

How Consultants and Advisors Face Claims

Consultants in business, technology, marketing, and management advisory roles operate similarly-clients hire them for strategic guidance, and a flawed recommendation or missed deadline becomes grounds for a claim. Your advice shapes business decisions, and clients expect that guidance to meet professional standards. When a strategy fails or a deadline slips, clients often pursue recovery through litigation, claiming they relied on your expertise and suffered financial loss as a result.

Medical and Healthcare Provider Exposure

Medical professionals and healthcare providers operate in a high-claims environment where even minor documentation errors or communication breakdowns lead to patient disputes and litigation. The healthcare sector generates frequent claims because patient expectations are explicit and regulatory requirements are strict. A missed note in a patient file or a miscommunication about treatment options can escalate into a formal complaint and lawsuit.

Real Estate and Legal Professional Risks

Real estate professionals handle large sums and complex transactions, making them targets for claims about misrepresentation, failure to disclose material facts, or procedural errors. Lawyers and legal professionals face the highest frequency of claims because law practice involves strict procedural deadlines and client expectations are explicit. A missed statute of limitations deadline is indefensible and costly. If you work in any of these fields in Culver City, E&O is not optional-it is the baseline protection your clients expect and your business requires.

Finding the Right Coverage for Your Practice

As your practice grows and your client base expands, your coverage needs shift. The limits and policy terms that protected you as a solo practitioner may leave you exposed once you add staff or take on larger projects. This is where working with an independent agent becomes valuable-someone who represents multiple top-rated carriers can identify the coverage limits and policy terms that match your actual risk exposure and client contract requirements.

How to Choose the Right E&O Policy for Your Business

Match Coverage Limits to Your Actual Risk

Your industry determines what E&O policy actually protects you. An architect’s $2 million limit may prove insufficient for a firm designing commercial buildings, while a solo marketing consultant might operate safely at $1 million. Match coverage limits to your annual revenue, the complexity of your engagements, and what your client contracts demand. Start by reviewing three to five client agreements to identify their insurance requirements-many specify minimum limits you must carry, and failing to meet these contractual obligations can void your business relationship or trigger breach claims.

Next, calculate your potential exposure by asking what the most expensive mistake would cost. If a design error delays a $5 million construction project by one month, your exposure could reach $200,000 or more in client damages claims. Defense costs alone typically run $100,000 to $300,000 before settlement, so your limit must cover both defense and potential judgments.

Deductibles Shape Your Out-of-Pocket Costs

Your deductible also shapes the economics of your coverage. A higher deductible ($10,000 or $25,000) reduces premiums but means you absorb those costs before coverage activates. A lower deductible ($2,500 or $5,000) costs more in premiums but limits your out-of-pocket exposure when claims arrive. Try choosing based on your cash reserves and risk tolerance-practices with strong reserves can absorb higher deductibles, while those with tighter cash flow should minimize them.

Compare Quotes Across Multiple Carriers

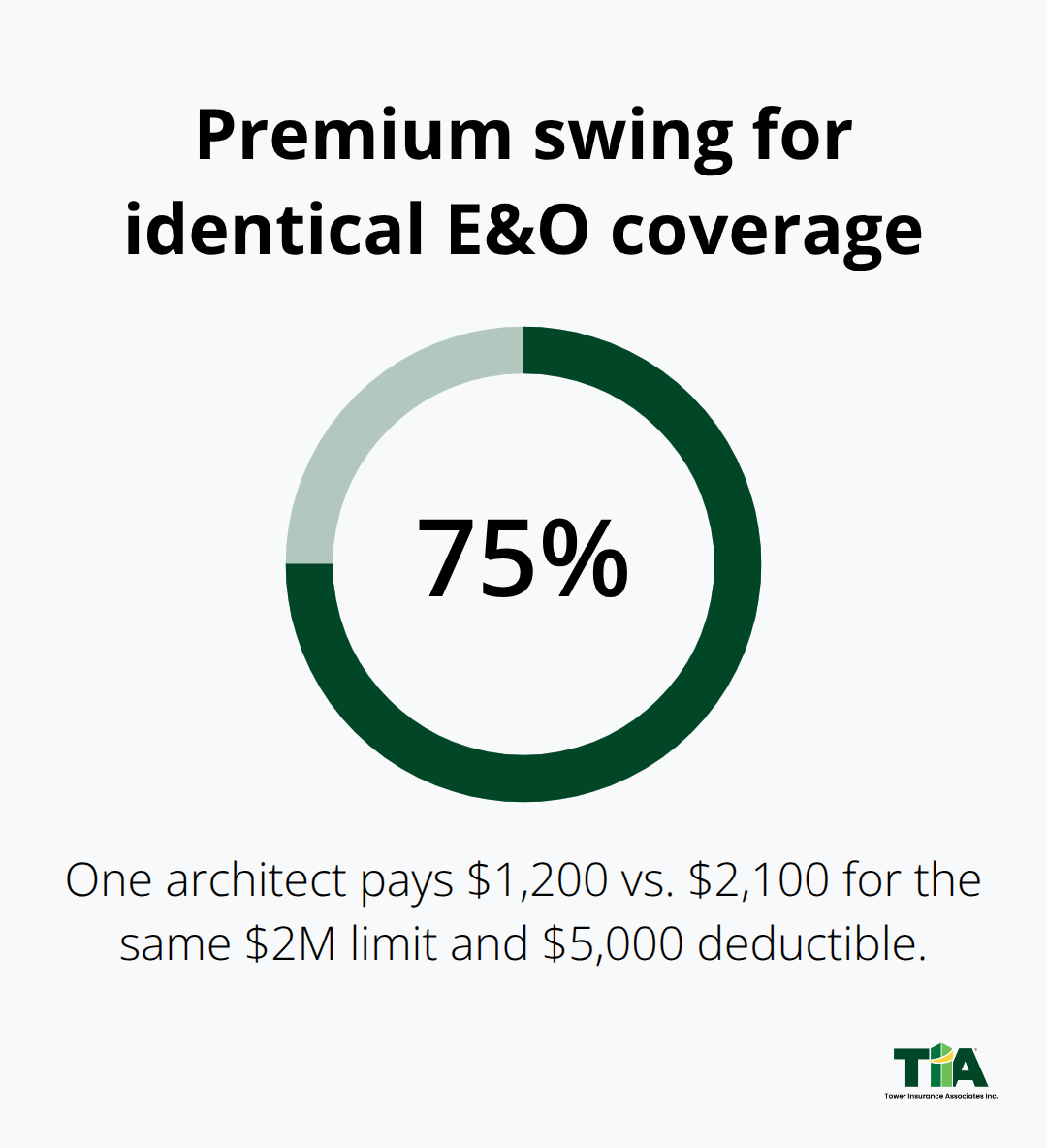

Comparing quotes across multiple carriers reveals substantial premium differences for identical coverage. One architect in Culver City might pay $1,200 annually for $2 million in limits with a $5,000 deductible from one carrier and $2,100 from another, a 75% premium swing for the same protection. This is why working with an independent agent who represents multiple top-rated insurers matters-they access pricing from carriers you cannot reach directly and identify which companies offer the best terms for your specific profession and claims history.

Request quotes from at least three carriers and compare not just price but also claims handling reputation, exclusions that might affect your work, and whether defense costs are paid inside or outside your policy limits. Ask each carrier how they handle your specific profession-some insurers specialize in architects and engineers, others focus on consultants or healthcare providers, and their pricing and coverage terms reflect that specialization. A carrier with deep expertise in your field typically offers better coverage terms and claims support than a generalist insurer.

Leverage Local Agent Expertise

An independent agent in Culver City who represents multiple carriers can access competitive quotes and specialized expertise without you shopping multiple agencies yourself. Tower Insurance Associates, Inc., an independent agency in business since 1961, represents multiple top-rated carriers and can compare options tailored to your practice. Contact Tower at 310-837-6101 to explore coverage that matches your profession and risk profile.

Final Thoughts

E&O insurance protects your professional reputation and finances when client claims arrive. Without it, a single mistake drains your business reserves and damages years of work. The coverage pays defense costs and settlements so you can focus on your practice instead of litigation.

Choosing the right policy requires matching coverage limits to your actual exposure, understanding how deductibles affect your cash flow, and comparing quotes across multiple carriers. Your client contracts often specify minimum limits you must carry, and meeting those requirements protects both your business relationships and your ability to win new work. A $1 million limit may suffice for a solo consultant, but a firm with larger projects and more clients needs higher protection (the cost difference between carriers for identical coverage can exceed 50 percent).

We at Tower Insurance Associates, Inc. represent multiple top-rated carriers and can tailor E&O insurance Culver City to your specific needs. Contact Tower Insurance Associates, Inc. at 310-837-6101 to discuss your coverage and receive competitive quotes. Your professional practice deserves protection that matches your actual exposure.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.