One mistake in your professional practice can cost you thousands-or millions-in legal fees and damages. California professional liability insurance protects your business when clients claim you failed to deliver the service they paid for.

At Tower Insurance Associates, Inc., we help California professionals understand their coverage options and find policies that actually match their risks. This guide walks you through everything you need to know.

What Professional Liability Insurance Actually Covers

Professional liability insurance in California protects you when a client claims you made an error, gave bad advice, or failed to complete work as promised. Professional liability insurance covers a consultant or contractor for claims arising from the rendering or failure to render professional services. A single mistake-a missed deadline, an overlooked contract detail, or incorrect guidance-can trigger a lawsuit that costs tens of thousands of dollars just to defend, regardless of whether you’re found liable.

Coverage That Protects Your Practice

California courts hold professionals accountable for negligence, misrepresentation, and omissions. In 2025, California’s insurance landscape shifted with new legislation addressing underinsurance and insurer stability, meaning clients now scrutinize whether their service providers carry adequate coverage. Some clients require proof of professional liability insurance before signing contracts, making this protection not just a safety net but a business necessity in competitive markets.

Industries With the Highest Exposure

Consultants, technology professionals, real estate agents, accountants, designers, and IT specialists face the highest exposure. Real estate agents omit important property details. IT professionals give incorrect cybersecurity advice. Designers fail to follow agreed specifications.

Each scenario triggers client claims that professional liability insurance covers.

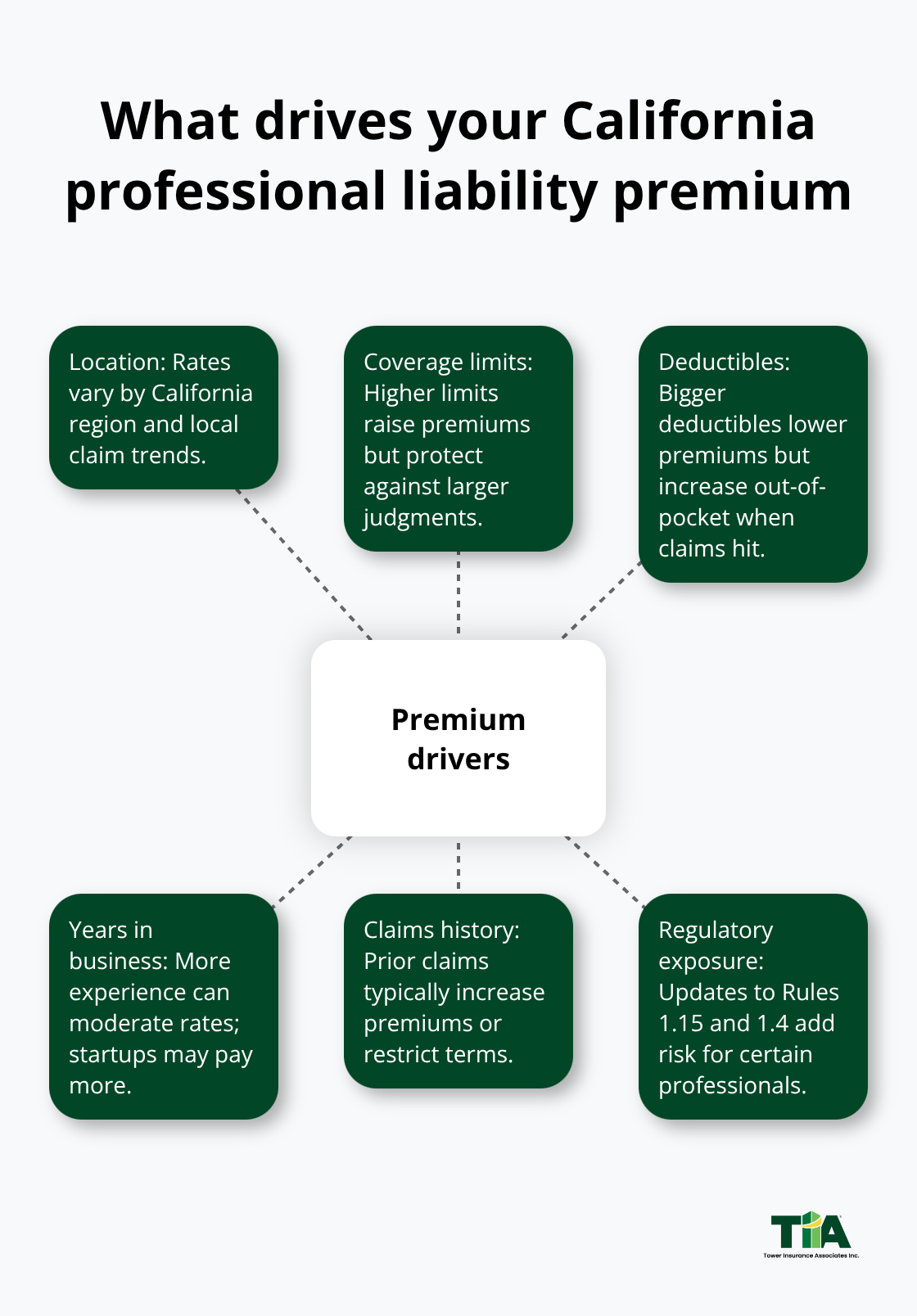

How Premiums Reflect Your Risk Profile

Location, coverage limits, deductibles, years in business, and claims history all influence your premium costs. Higher coverage limits increase premiums, so you’ll balance protection with affordability based on your actual risk exposure. California’s evolving professional responsibility rules-particularly updates to trust accounting (Rule 1.15, effective January 1, 2023) and communication standards (Rule 1.4)-create additional liability exposure for professionals who handle client funds or manage complex client relationships.

Regulatory Compliance and Insurance

The State Bar of California enforces professional standards strictly, and violations can lead to discipline that affects both your license and your insurability. Aligning your coverage limits with your specific industry risks and client requirements prevents you from becoming underinsured or overpaying for unnecessary protection. Understanding what your policy actually covers-and what gaps remain-determines whether you’re truly protected when a claim arrives.

Types of Professional Liability Coverage for California Professionals

Professional liability insurance comes in distinct forms, each designed for different professional services and risk exposures. Errors and Omissions (E&O) insurance covers consultants, technology professionals, real estate agents, accountants, and designers when clients claim negligence, misrepresentation, or service failures. Real estate agents frequently face claims over omitted property details, while IT professionals encounter disputes about cybersecurity guidance and system implementations. E&O premiums vary significantly based on your location in California, coverage limits you select, your deductible choice, years your business has operated, and your prior claims history.

Errors and Omissions Insurance Protects Your Core Services

Higher limits cost more but protect against larger judgments. You can customize quotes online to see exact pricing for different limit combinations. Medical malpractice insurance applies exclusively to physicians, surgeons, nurses, and other healthcare providers whose mistakes cause patient harm or injury. Directors and Officers (D&O) liability covers board members and executives when shareholders or third parties allege mismanagement, breach of fiduciary duty, or wrongful decisions. This coverage matters increasingly in California as governance standards tighten and shareholder activism grows.

Cyber Liability Addresses Data Security Risks

Cyber liability insurance protects professionals who handle sensitive client data-accountants managing financial records, consultants storing proprietary information, real estate professionals collecting personal information during transactions. California’s evolving data security requirements and the State Bar’s emphasis on technology competence (reinforced through Rule 1.4 communication updates effective January 1, 2023) make cyber coverage essential for any professional managing digital client information.

Match Coverage to Your Actual Exposures

Your industry determines which coverage types you genuinely need. Consultants typically require E&O only, while accountants need both E&O and cyber liability because they access client financial data and tax documents. Real estate professionals must prioritize E&O but should also consider cyber coverage if they collect buyer financial information online. Many professionals purchase blanket coverage without assessing their specific risk profile. Instead, evaluate what claims could realistically arise from your services, what clients require contractually, and what regulatory bodies expect.

California’s 2025 insurance legislation addressing underinsurance means clients now scrutinize whether service providers carry adequate limits. Some clients demand proof of coverage before signing contracts, making your policy limits a competitive factor. Higher limits increase premiums, but underinsurance creates exposure that insurance won’t cover. Your insurer’s ability to defend you matters as much as the coverage itself. California courts hold insurers accountable through the duty to defend doctrine, as emphasized in recent cases like Bartel v. Chicago Title Insurance Company (2025). This means your insurer must investigate coverage possibilities thoroughly and cannot bypass defense obligations through disputes over whether your conduct falls within policy language.

Evaluate Carrier Strength and Claims Support

When choosing a carrier, verify their claims support structure, their track record in California courts, and whether they offer legal defense before coverage determination. Stability and claims experience matter when you actually need to file a claim. The next step involves understanding how to select the right policy limits and deductibles for your specific situation.

How to Choose the Right Professional Liability Policy

Calculate Your True Exposure, Not Industry Averages

Start with your actual exposure, not industry averages or what competitors claim to carry. Calculate the maximum financial damage a single claim could inflict on your business. If you’re a consultant managing a six-month project worth $500,000 and a client sues for total project failure plus consequential damages, your exposure could exceed $1 million. If you’re a real estate agent handling properties in the $2–5 million range, a lawsuit over an omitted disclosure could trigger claims matching the property value. Your coverage limit should reflect this realistic worst-case scenario, not a generic industry standard.

California’s underinsurance crisis demonstrates that inadequate limits leave you personally liable for claims that exceed your policy. Review your client contracts to identify what coverage limits clients specifically require before engagement. Many commercial clients now demand proof of $1–2 million in professional liability coverage as a contract condition.

Balance Your Deductible Against Premium Costs

Your deductible strategy matters equally to your coverage limits. A higher deductible ($10,000 or $25,000) reduces your premium but increases out-of-pocket costs when a claim arrives. California’s competitive professional services market means clients view your coverage level as a quality indicator. Underinsured professionals lose contracts to better-protected competitors, so your policy limits directly affect your ability to win business.

Lower deductibles cost more upfront but protect your cash flow when claims occur. Try selecting a deductible that matches your business’s financial capacity to absorb losses without operational disruption. Your premium reflects both the deductible level and your coverage limits, so test multiple combinations to find the right balance for your situation.

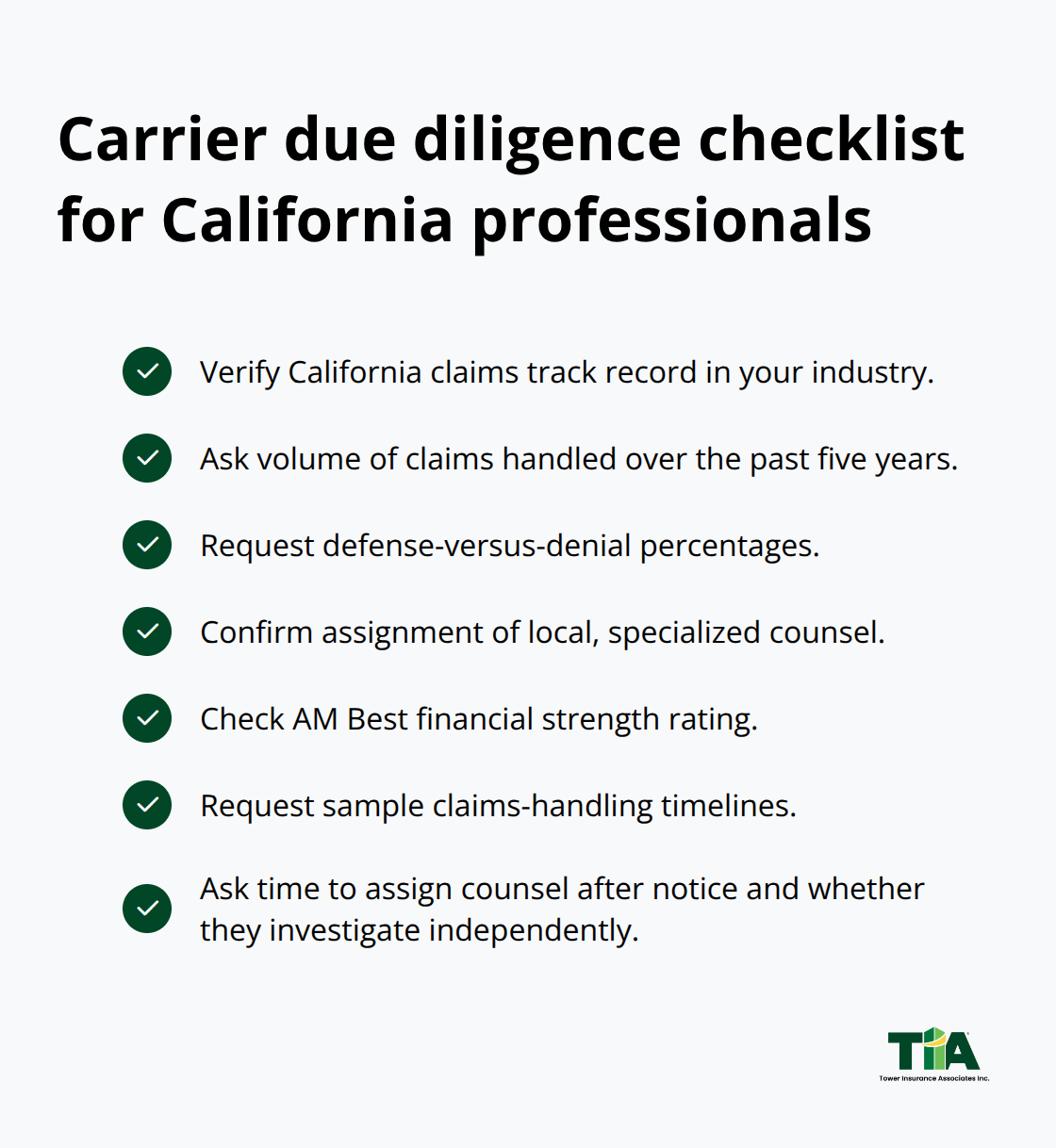

Verify Carrier Stability and Claims Performance

California courts have shifted expectations around insurer obligations. Recent decisions reinforce that your insurer must defend you thoroughly and cannot avoid coverage through procedural disputes. This means you need a carrier with strong California experience, not a national insurer treating your claim as a routine file.

Verify your potential insurer’s claims handling track record in California specifically. Ask prospective carriers how many professional liability claims they’ve handled in your industry over the past five years, what percentage they defend versus deny, and whether they assign local counsel familiar with California professional liability law. An insurer’s financial ratings matter too-check AM Best ratings to confirm they can actually pay large settlements.

Request sample claims handling timelines before purchase. How long does the carrier take to assign counsel after notice? Do they conduct independent investigations or rely on your account of events? Carriers that move slowly on initial investigation create exposure because delay can prejudice your defense. Your premium cost should reflect not just coverage limits but the quality of claims support behind those limits.

Assess Local Expertise and Defense Capabilities

Your insurer’s ability to defend you matters as much as the coverage itself. California courts hold insurers accountable through the duty to defend doctrine, emphasizing that your insurer must investigate coverage possibilities thoroughly and cannot bypass defense obligations through disputes over policy language.

Work with carriers that understand California’s unique professional liability landscape. Ask whether they maintain relationships with local defense counsel who specialize in your industry. An insurer familiar with California’s evolving professional responsibility rules will defend more effectively than one applying generic national standards. Local expertise translates directly into better outcomes when disputes arise over coverage interpretation.

Final Thoughts

Professional liability insurance protects your practice, satisfies client demands, and keeps you competitive in California’s demanding professional services market. A single claim costs tens of thousands in legal defense alone, and California courts hold both professionals and insurers to strict accountability standards. Your coverage limits must match your actual exposure, not industry averages, while your deductible should reflect what your business can absorb without operational disruption.

The 2025 legislation addressing underinsurance shifted the landscape permanently-clients now scrutinize whether service providers carry adequate coverage before signing contracts. This means your California professional liability policy directly affects your ability to win business and maintain client relationships. Your insurer’s ability to navigate California’s evolving professional responsibility rules (trust accounting standards, communication requirements, and technology competence expectations) matters as much as the coverage itself.

We at Tower Insurance Associates, Inc. help California professionals cut through this complexity by customizing quotes to reflect your specific business, industry, and risk profile. Contact Tower Insurance Associates to discuss your professional liability needs with advisers who understand your industry and your market.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.