Your classic car deserves protection that standard auto policies simply don’t provide. At Tower Insurance Associates, Inc., we know that classic auto insurance in California requires a different approach than coverage for everyday vehicles.

This guide walks you through the specific protections your classic car needs, how to avoid costly coverage gaps, and strategies for getting the best rates in California.

Why Standard Auto Insurance Fails Classic Car Owners

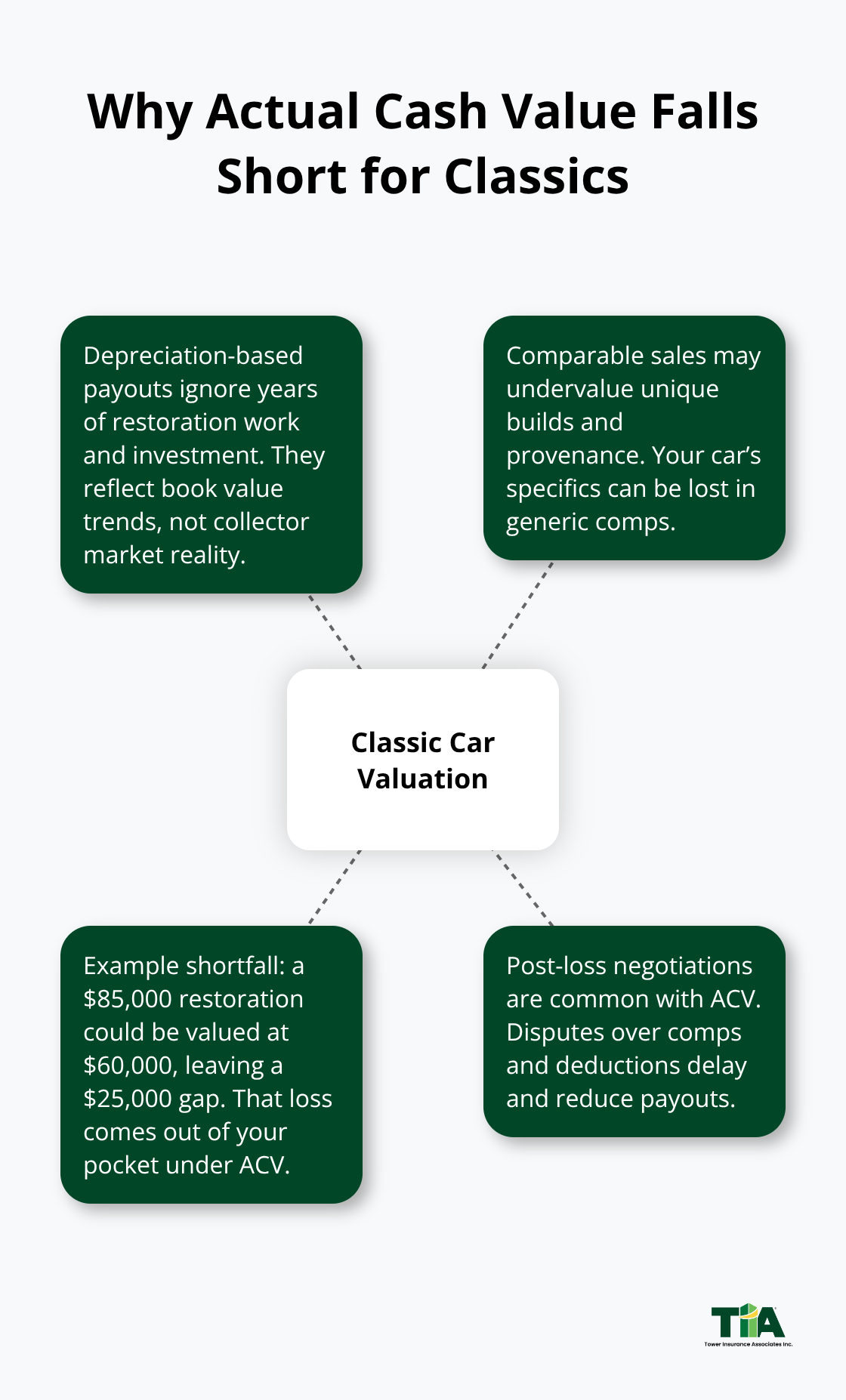

The Actual Cash Value Problem

Standard auto insurance policies are built for vehicles that lose value every year and get driven daily. Your classic car operates in a completely different world. A typical auto policy calculates payouts using Actual Cash Value, which means an insurer determines what your car was worth at the time of loss using depreciation and adjusted comparable data. For a 1967 Chevrolet Corvette that you restored over five years and invested $85,000 into, this approach creates a massive problem. The adjuster might value it at $60,000 based on comparable sales, leaving you $25,000 short.

Mileage Limits That Don’t Match Reality

Standard policies impose mileage limits designed for commuter vehicles-often 12,000 to 15,000 miles annually-which conflicts with classic car ownership. If you drive your restored 1957 Ford to three car shows across California, attend a charity parade, and make occasional weekend cruises, you could easily hit 5,000 miles in a season. Exceed the mileage cap and your coverage vanishes entirely when you need it most.

How Agreed Value Coverage Protects Your Investment

Agreed Value coverage solves this problem directly. You and your insurer establish the car’s value upfront, and that amount is locked in. If your classic car is totaled or stolen, you receive the agreed-upon value minus your deductible-no negotiation, no adjuster debate, no depreciation haircuts. American Collectors Insurance, a specialist in this space, uses this approach and reports that agreed value removes post-loss disputes entirely.

Flexible Mileage Plans for Active Collectors

Mileage-based policies for classics reflect reality. Instead of a rigid annual limit, flexible plans let you choose usage tiers that match your actual driving patterns. Whether you drive 2,000 miles yearly to select shows or 8,000 miles for active restoration work, you pay for what you actually use. Comprehensive coverage under a classic policy protects your vehicle even during storage or display at events-something standard policies often exclude.

Moving Forward with the Right Coverage

The gap between standard auto insurance and classic car protection is substantial. Agreed value protection and usage flexibility tailored to classic car ownership prevent you from forcing your prized vehicle into a standard auto insurance box designed for depreciating daily drivers. Understanding what coverage types actually exist is the next step in securing the right policy for your collection.

Types of Classic Car Coverage You Need

Comprehensive and Collision Protection Form Your Foundation

Comprehensive and collision coverage form the foundation of any serious classic car policy, but how they work differs significantly from standard auto insurance. Comprehensive coverage protects against theft, vandalism, weather damage, and other non-collision events-critical for a vehicle you store between shows or keep in a garage. Collision coverage handles damage from accidents, including single-vehicle incidents like hitting a pothole or rolling into a ditch during a restoration drive. The distinction matters because classic cars face unique risks standard policies overlook. Your 1957 Ford parked in a climate-controlled garage faces different threats than a daily commuter, and your coverage should reflect that reality.

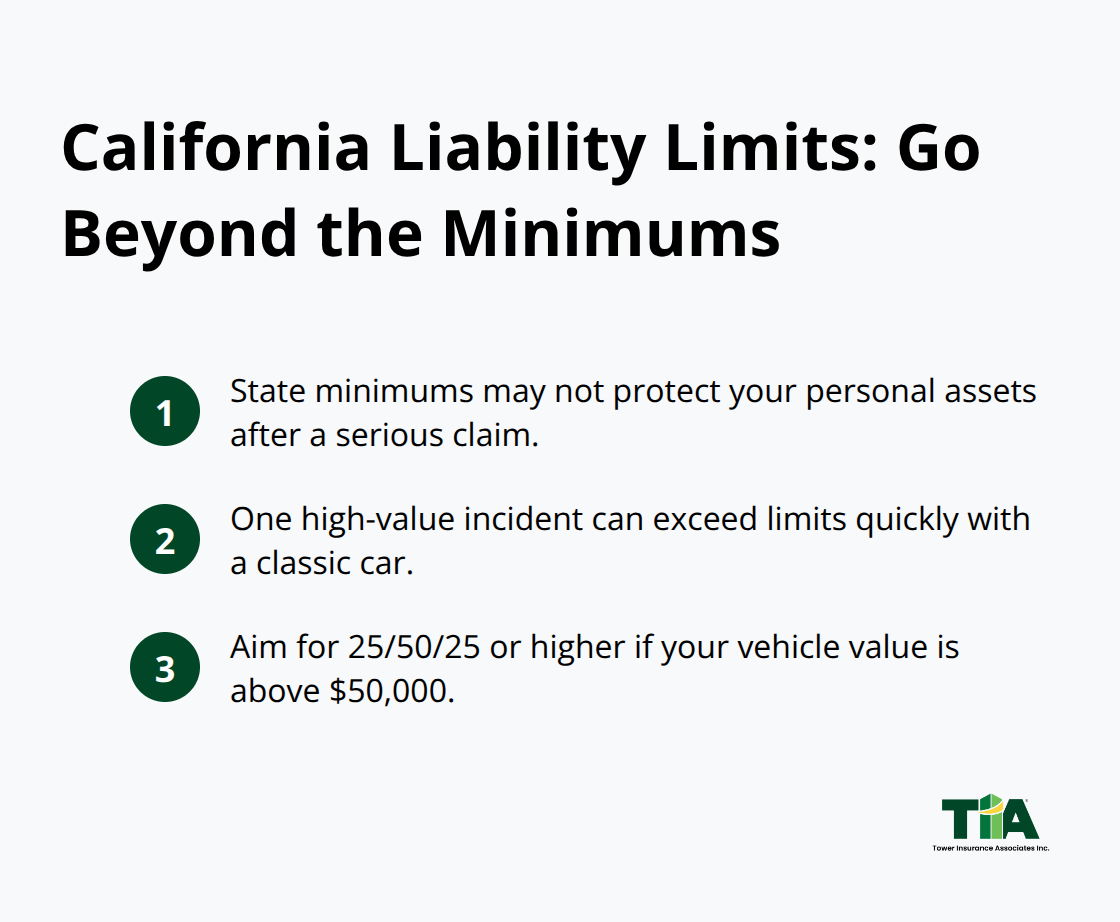

California’s Liability Requirements and Why You Should Exceed Them

California requires liability coverage of at least $30,000 for injury or death to one person, $60,000 for injury or death to more than one person, and $15,000 for property damage for all registered vehicles, but classic car owners should exceed these minimums substantially. If you cause an accident and your classic car damages someone else’s vehicle or property, the state minimum won’t protect your personal assets if the claim exceeds coverage limits. A single incident involving a high-value classic car can generate claims far beyond the state floor-try 25/50/25 or higher if your vehicle is valued above 50,000 dollars.

Uninsured and Underinsured Motorist Protection Shields Your Investment

Uninsured and underinsured motorist protection shields you when the other driver lacks adequate coverage or disappears. California law requires this coverage at the same limits as your liability, but again, classic car owners should increase these limits. If an uninsured driver hits your classic car at a car show and causes significant damage, your uninsured motorist collision coverage pays for repairs up to your policy limit, protecting you from absorbing losses caused by someone else’s negligence.

Building a Coverage Strategy That Works

Select comprehensive and collision coverage with deductibles you can comfortably afford (500 dollars or 1,000 dollars is standard), establish liability limits at 25/50/25 or higher, and confirm your uninsured and underinsured motorist protection matches those liability limits. Request that your agent explicitly show you the policy language confirming these coverage types and their limits before you finalize any classic car insurance. Some carriers bundle these protections into a classic car package with agreed value and mileage flexibility already included, making administration simpler. Others require you to specify each component separately, creating opportunities for gaps if you’re not deliberate. Tower Insurance Associates, Inc., an independent agency in Culver City representing multiple top-rated carriers, works to match policies to your specific vehicle and driving patterns.

The coverage you select now determines what happens when an accident or loss occurs. Your next decision involves the practical steps that lock in the best rates for your classic car-documentation, appraisals, and the right agent relationship all play critical roles in what you ultimately pay.

How to Get the Best Classic Car Insurance Rates in California

Documentation and Appraisal Requirements

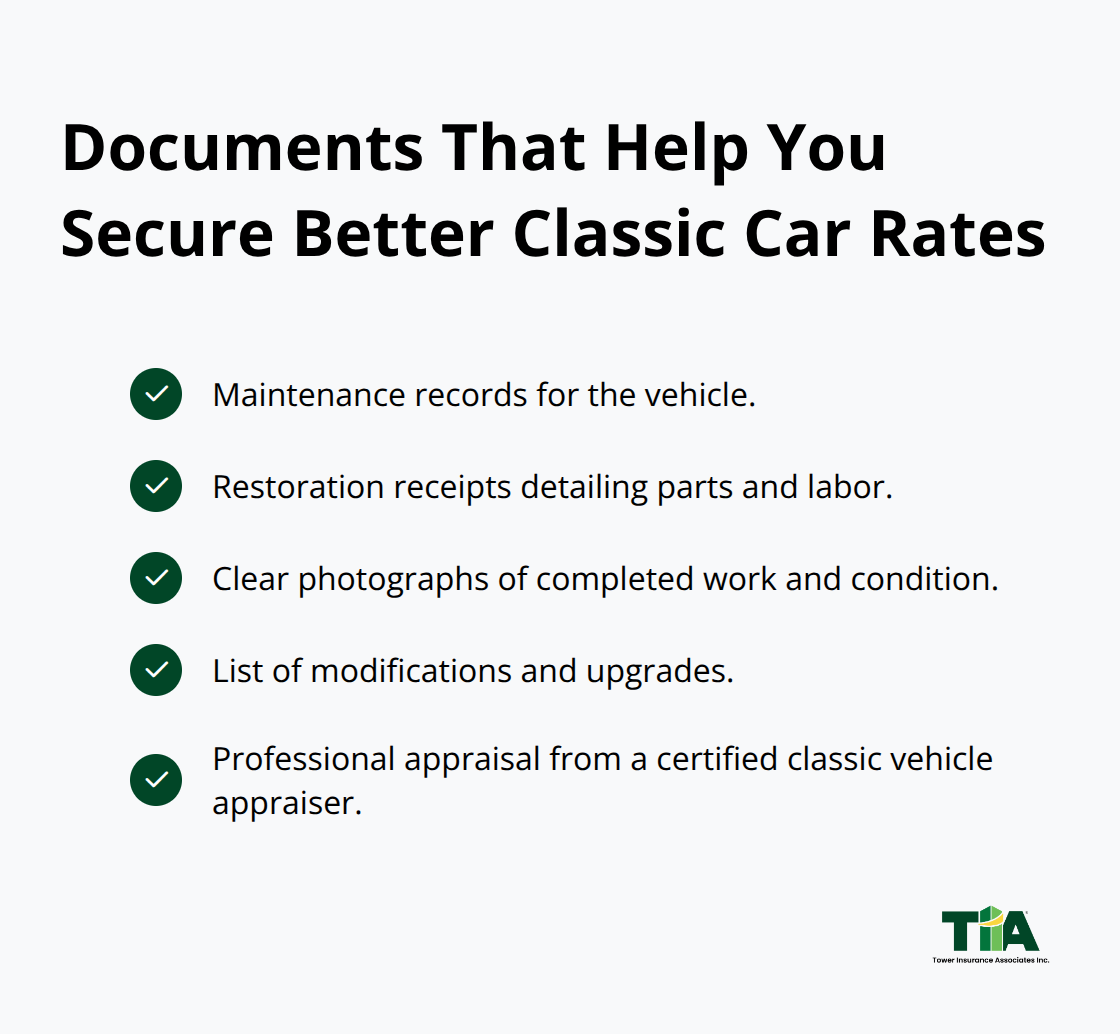

The foundation of competitive classic car insurance rates in California rests on accurate documentation that proves your vehicle’s value and condition. Insurers price policies based on risk, and a well-documented classic car reduces uncertainty about what payout should occur in the event of a claim. Professional appraisals carry weight because they establish an independent, defensible valuation that both you and your insurer can reference.

Obtain a written appraisal from a certified appraiser who specializes in classic vehicles-not a general automotive appraiser. The appraiser should document the vehicle’s condition, restoration quality, original specifications, and comparable sales data. This appraisal becomes your negotiating tool when locking in agreed value coverage.

Bring maintenance records, restoration receipts, photographs of work completed, and any documentation of modifications or upgrades. Insurers offering competitive rates reward organized owners because your records eliminate guesswork during underwriting. When you contact an insurer with a complete appraisal and supporting records, you accelerate the underwriting process and demonstrate that you take your vehicle seriously-a signal that reduces claims frequency in the insurer’s eyes.

Bundling and Multi-Policy Discounts

Bundling your classic car insurance with homeowners, life, or other policies held with the same carrier typically generates discounts depending on the carrier and number of policies combined. This is one of the most overlooked rate-reduction strategies because classic car owners often shop for collector coverage separately without considering what else they insure.

If you already have homeowners insurance with a major carrier, contact that same company to request a classic car quote bundled with your existing policies before shopping elsewhere. Some carriers offer loyalty discounts for customers who maintain multiple lines of coverage over several years, further lowering your effective premium. However, bundling only works if the carrier’s classic car rates are competitive to begin with. A discount on an overpriced policy still leaves you paying more than a specialized carrier’s standard rates.

Compare bundled quotes from your current homeowners insurer against quotes from carriers that specialize in classic vehicles before making a decision.

Finding an Agent Who Knows Classic Cars

The agent relationship determines whether you receive expert guidance or generic treatment. A classic car agent understands that your 1957 Ford is not a daily commuter and should not be priced or covered like one. During your initial conversation, ask the agent directly how many classic car policies they handle annually and whether they personally own or have owned a collector vehicle.

An agent without hands-on collector experience often lacks the knowledge to identify gaps or optimize your coverage. Ask them to explain the difference between agreed value and actual cash value, and listen for whether they can articulate why agreed value matters specifically for classics. Request that they walk you through policy language before you commit, showing you exactly where agreed value is stated and confirming that mileage limits match your actual usage patterns.

A knowledgeable agent catches details like whether comprehensive coverage applies to vehicles in storage or only while being driven-a critical distinction for seasonal classics. They should also know California’s specific regulations around historic plates and how those regulations affect your insurance eligibility. Schedule a phone or in-person conversation rather than relying on online quotes alone. The time you invest speaking with an actual agent often reveals rate reductions or coverage improvements that automated systems miss entirely.

Final Thoughts

Classic auto insurance in California protects your investment through agreed value coverage that locks in your car’s worth upfront, eliminating post-loss disputes and ensuring you receive full compensation if your vehicle is damaged or stolen. Flexible mileage plans accommodate your actual driving patterns, whether you attend monthly car shows or drive seasonally to restoration events. Comprehensive and collision protection tailored to classic vehicles covers risks that everyday auto policies overlook, and liability limits exceeding California’s minimums shield your personal assets from catastrophic claims.

A professional appraisal from a specialist establishes defensible valuation that insurers respect and use to set competitive rates, while bundling your classic car policy with homeowners or other coverage generates discounts that reduce your overall premium. Working with an agent who understands classic car ownership prevents coverage gaps and identifies rate reductions that automated online quotes miss entirely. That agent relationship matters more than shopping price alone because your 1957 Ford is not a daily commuter and should never be treated like one.

Contact Tower Insurance Associates, Inc. to discuss your classic car’s protection needs and receive a competitive quote tailored to your collection. We represent multiple top-rated carriers and specialize in matching personalized coverage to your specific vehicle and driving patterns. Our team provides claims advocacy when you need it most and understands California’s historic plate regulations and how they affect your eligibility and rates.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.