Los Angeles businesses face a rising tide of cyber threats that can cripple operations and drain resources. Data breaches hit harder in California due to strict regulatory requirements and costly notification laws.

At Tower Insurance Associates, Inc., we know that Los Angeles cyber insurance isn’t optional anymore-it’s a business necessity. This guide walks you through what coverage you need and how to find the right protection for your company.

Why Your Los Angeles Business Is a Target

California’s regulatory environment makes data breaches exponentially more expensive than in other states. When a breach affects 500 or more California residents, your company must submit a sample breach notification to the California Attorney General through their online reporting system. You also face mandatory notification requirements under California Civil Code sections 1798.82 and 1798.29, which means notification costs, credit monitoring services, and public relations expenses become non-negotiable line items in your budget. These aren’t theoretical expenses-they’re real costs that hit immediately after a breach, before you’ve even assessed the full damage to your operations.

The Numbers Behind California Breaches

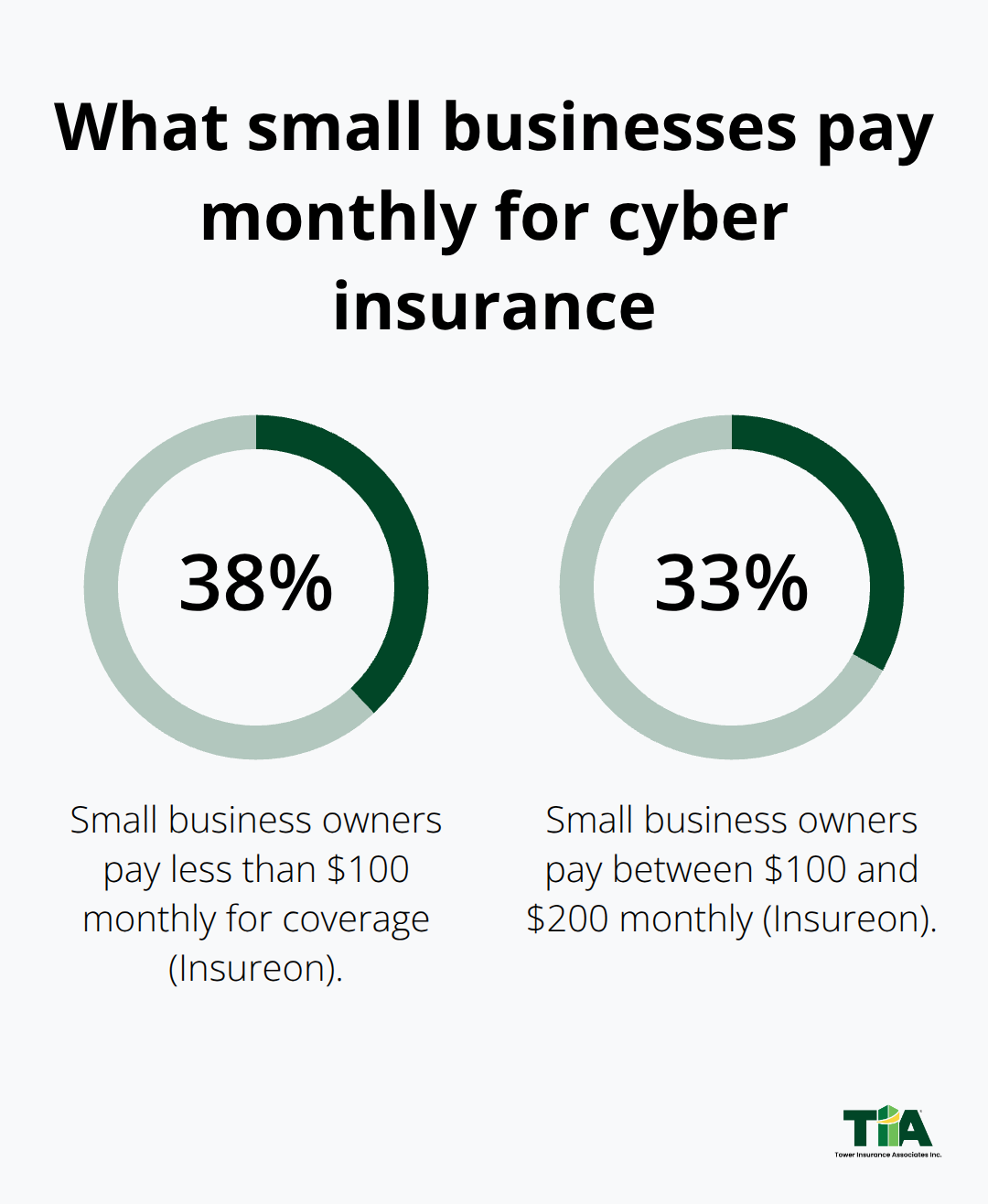

Small businesses pay an average of $1,609 annually for cyber insurance, with premiums ranging from $400 to over $8,000 depending on coverage limits and business risk factors. However, the cost of a breach itself dwarfs insurance premiums. A single breach notification campaign, forensic investigation, and credit monitoring service for affected customers can easily exceed $50,000. According to Insureon’s small business data, 38 percent of small business owners pay less than $100 monthly for coverage, while 33 percent pay between $100 and $200 monthly. The math is straightforward: spending $1,600 annually on cyber insurance is far cheaper than absorbing breach response costs that can reach six figures.

About 98 percent of cyber insurance claims come from small and midsized businesses, which tells you that your company size doesn’t protect you from cyber risk-it actually increases your vulnerability because attackers know smaller organizations typically have fewer security resources.

What Makes Los Angeles Particularly Vulnerable

The Los Angeles region faces heightened cyber risk due to geopolitical conflicts and major events including the 2026 FIFA World Cup and the 2028 Olympic Games. These events attract both legitimate digital traffic and malicious actors who exploit infrastructure vulnerabilities. Local governments and critical infrastructure providers have formed the Regional Cyber Collaborative to share real-time threat intelligence across six counties, using their Threat Intelligence Sharing Platform to distribute actionable alerts about ransomware, phishing, and DDoS attacks targeting the region.

Your business operates in an environment where coordinated threat intelligence flows between public sector partners, yet most private companies remain isolated from this critical information. This intelligence gap means you operate without knowledge of active threats specifically targeting Los Angeles businesses in your industry sector.

How Coverage Addresses Your Regional Risk

Cyber insurance policies tailored to Los Angeles businesses cover the specific costs that California law imposes on you. Coverage for data breach response and notification costs protects your cash flow when regulatory requirements force you to act fast. Protection against ransomware and business interruption keeps your operations running when attackers strike. Legal defense and liability coverage shields you from lawsuits that follow a breach (these costs often exceed the breach itself).

The right policy limits and deductibles matter more in Los Angeles than in other regions because your regulatory obligations are steeper. Working with local agents who understand California’s breach notification framework and your industry’s specific vulnerabilities helps you avoid coverage gaps that could leave you exposed.

What Does Cyber Insurance Actually Cover

First-Party, Second-Party, and Third-Party Costs

When a breach happens, your company faces three distinct cost categories that most business owners underestimate. First-party costs include your own incident response, forensic investigation, customer notification, credit monitoring services, and public relations expenses. Second-party costs involve legal defense when clients or partners sue you for failing to protect their data. Third-party costs cover your liability when you’re held responsible for damages to others. Cyber insurance covers all three cost categories, but only if you understand what each policy limit actually protects.

Understanding Deductibles and Policy Limits

According to Insureon’s data on small business coverage, the average deductible sits around $2,500, meaning you’ll pay that amount out of pocket before your policy kicks in. Higher deductibles reduce your monthly premium but require more cash reserves when crisis hits. The per-occurrence and aggregate limits typically range from $1 million to $5 million, but Los Angeles businesses handling sensitive customer data or processing payment cards need to evaluate whether these limits match your actual exposure. If a breach affects 500 or more California residents, your notification costs alone can exceed $50,000 before you’ve even addressed the forensic investigation or credit monitoring obligations. Your policy should explicitly cover these regulatory-mandated expenses, not leave them as gray areas that might spark coverage disputes when you need the money most.

Ransomware and Business Interruption Protection

Ransomware and business interruption coverage addresses the operational damage that exceeds notification costs. When attackers lock your systems, you lose revenue while your team sits idle and your operations grind to a halt. Cyber policies covering business interruption reimburse lost income and extra expenses incurred during the outage, which means your company can survive the days or weeks needed to restore systems and recover data. This coverage becomes essential for Los Angeles service providers, e-commerce businesses, and any operation where downtime directly kills revenue.

Legal Defense and Tech E&O Coverage

Legal defense coverage pays for attorneys when lawsuits follow a breach, protecting you from costs that often rival or exceed the breach response itself. Tech E&O (errors and omissions) coverage bundled with cyber policies addresses claims that you failed to implement adequate security measures, a growing source of litigation.

Lowering Your Premiums Through Risk Management

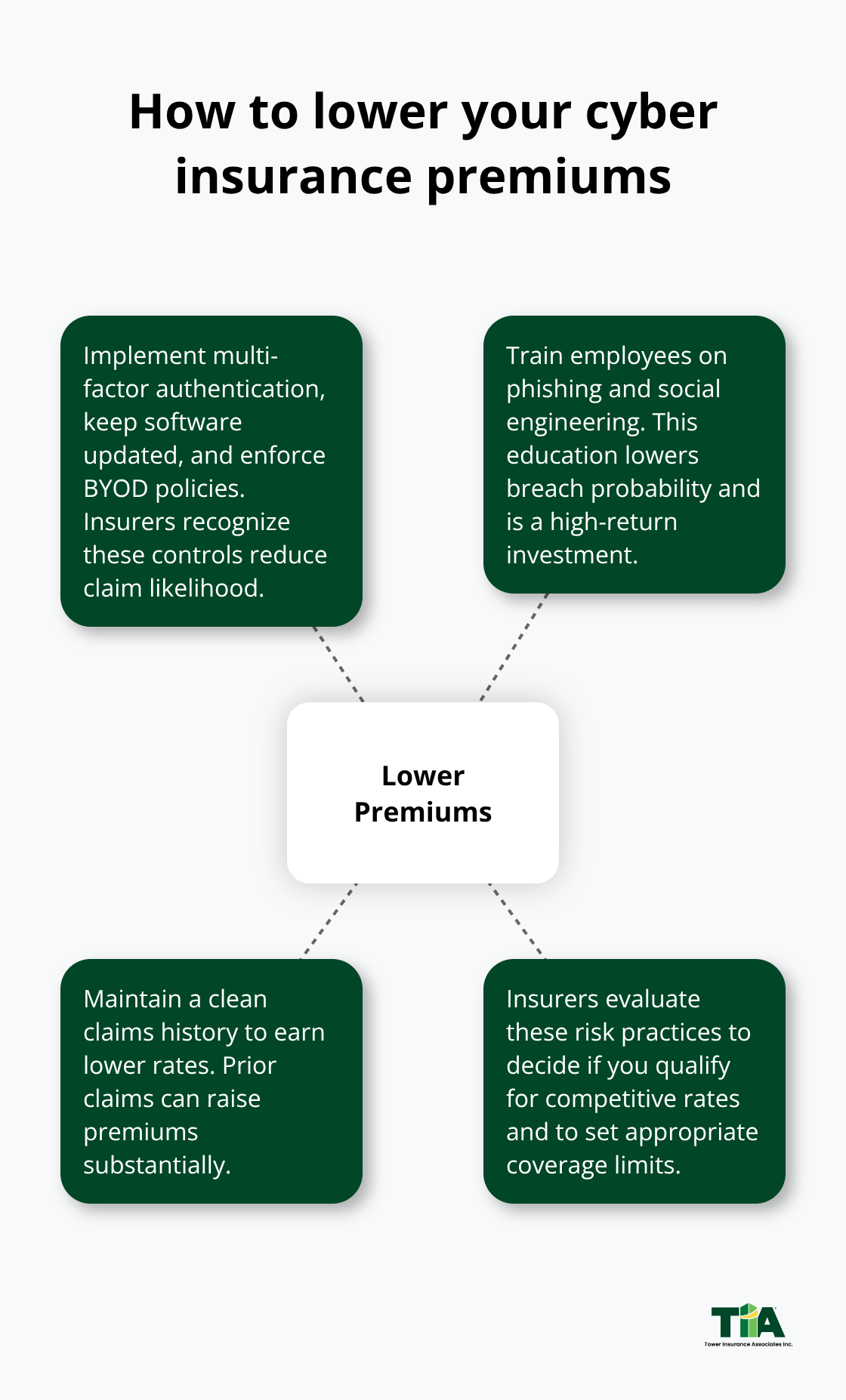

Investing in basic security measures like multi-factor authentication, regular software updates, and formal BYOD policies can lower your premiums significantly because insurers recognize these reduce claim likelihood. Employee training on phishing and social engineering attacks reduces your breach probability even more, making it one of the highest-return risk management investments you can make.

A clean claims history yields lower rates, while prior claims can raise premiums substantially, so preventing incidents pays dividends in future pricing. These risk management practices form the foundation that insurers evaluate when determining whether your Los Angeles business qualifies for competitive rates and what coverage limits make sense for your operation.

Finding the Right Cyber Insurance Partner in Los Angeles

Your Regional Threat Environment Demands Local Expertise

Los Angeles businesses operate in a threat environment unlike anywhere else in the country. This means your cyber insurance provider must understand the specific threat landscape affecting your Los Angeles location and industry. Most national carriers treat cyber coverage as a commodity product with standardized policies that ignore regional context. They don’t monitor threat intelligence alerts flowing between LA County government agencies, they don’t track which industries face the highest ransomware targeting in Southern California, and they won’t customize your policy limits based on LA-specific regulatory costs.

Why California’s Regulatory Framework Changes Your Coverage Needs

You need a provider with local expertise who understands that California’s breach notification requirements impose costs that dwarf national averages. When you notify 500 or more California residents of a breach, you must submit sample notifications to the California Attorney General, which means your policy should explicitly cover these regulatory-mandated expenses rather than leaving them as gray areas that generate coverage disputes when you need money fast. A local agent can evaluate whether your industry faces heightened risk in the LA region-healthcare providers handling HIPAA-protected data face different exposure than retail businesses processing payment cards, yet both operate under California’s strict notification framework.

Your deductible choice matters more in Los Angeles than elsewhere because your regulatory obligations are steeper. If you choose a $2,500 deductible to lower premiums, you’ll need $2,500 in cash reserves available immediately when a breach occurs, because notification costs don’t wait for insurance approval. The right deductible balances your monthly budget against your cash reserves and your industry’s breach probability.

Evaluating Coverage Details That Matter in Los Angeles

When you evaluate quotes, demand clarity on what counts as a regulatory-mandated notification cost and whether your policy covers credit monitoring, forensic investigation, and public relations expenses separately or as one aggregate limit. Some policies cap notification costs at $25,000, which sounds adequate until you realize that notifying thousands of California residents costs far more. Your agent should model breach scenarios based on your actual customer base size and data volume, showing you what your out-of-pocket costs would be under different deductible and limit combinations. This concrete analysis beats theoretical coverage discussions every time.

Questions to Ask Your Potential Provider

Ask your potential provider whether they monitor threat intelligence specific to your industry and region, whether they offer loss control services to reduce your breach probability, and whether they’ll review your policy annually as your business grows or your data handling changes. A provider who treats cyber insurance as a one-time transaction rather than an ongoing risk management relationship will leave you exposed when your business evolves. Your agent should ask whether you process payment cards (triggering PCI compliance obligations), whether you store employee records or customer data, and whether your industry faces heightened targeting in the LA region. These details drive your coverage needs far more than generic industry categories.

Working with a local agent means discussing your actual data handling practices, your customer notification procedures, and your recovery timeline if ransomware hits. A provider who understands California’s regulatory environment can help you structure policy limits that match your exposure rather than leaving gaps that could force you to absorb costs personally.

Final Thoughts

Los Angeles cyber insurance protects your business from costs that California’s regulatory environment makes unavoidable. When a breach hits, notification requirements, forensic investigations, credit monitoring, and potential lawsuits create expenses that reach six figures fast. The $1,600 annual premium for basic coverage costs far less than absorbing even a single breach response out of pocket, and about 98 percent of cyber insurance claims come from small and midsized businesses like yours, proving that company size offers no protection against cyber risk.

We at Tower Insurance Associates, Inc. understand that Los Angeles businesses face specific threats tied to regional events, geopolitical tensions, and California’s strict data protection laws. Your coverage needs differ from a business in Texas or Florida because your regulatory obligations are steeper and your threat environment is distinct. A provider who monitors threat intelligence specific to your industry and region helps you structure policy limits that actually match your exposure rather than leaving dangerous gaps.

Your deductible choice, policy limits, and coverage details matter more in Los Angeles than anywhere else because your breach costs are higher. A local agent reviews your actual data handling practices, your customer notification procedures, and your recovery timeline if ransomware strikes. Contact Tower Insurance Associates, Inc. to discuss your Los Angeles cyber insurance needs and build protection that actually fits your operation.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.