Los Angeles businesses face a rising tide of cyber attacks that threaten operations and finances. At Tower Insurance Associates, Inc., we’ve seen firsthand how quickly a breach can devastate a company without proper Los Angeles cyber coverage in place.

This guide walks you through the coverage options that matter most and how to select the right protection for your business.

Why Cyber Threats Are Escalating for Los Angeles Businesses

Ransomware and Data Breach Costs Hit Hard

Los Angeles has become a prime target for cyber attacks, and the numbers prove it. Ransomware attacks against California businesses increased substantially over the past three years, with attackers now targeting small and medium-sized enterprises specifically because they typically have fewer defenses than larger corporations. The average cost of a data breach nationwide reached $4.35 million according to the IBM Cost of a Data Breach Report 2023, but California businesses face even steeper bills due to CCPA and CPRA notification requirements. When a Los Angeles company suffers a breach, notification costs alone run $200 to $300 per record, forensic investigations consume $50,000 to $100,000 upfront, and legal defense costs pile on top of that. A mid-sized retail operation with 10,000 customer records could face $2 to $3 million in total breach expenses before any regulatory fines arrive.

Healthcare providers in Los Angeles encounter particularly aggressive targeting because patient data commands premium prices on the dark web, and HIPAA penalties for breaches can reach $1.5 million per violation category. Manufacturing firms, financial services companies, and professional services providers across LA face similar exposure because they all handle sensitive client information that regulators protect fiercely.

Weak Defenses Create Easy Entry Points

The vulnerabilities enabling these attacks are straightforward and preventable. Weak password practices remain the entry point for roughly 80 percent of breaches, yet most LA small businesses still allow employees to use simple passwords without multi-factor authentication. Unpatched software vulnerabilities sit on company networks for months because IT teams lack bandwidth for regular updates, leaving systems exposed to known exploits that attackers use routinely.

Phishing attacks succeed at alarming rates because employees receive minimal training on how to spot fraudulent emails mimicking banks, suppliers, or internal contacts. Social engineering fraud specifically tricks staff into wiring funds or revealing credentials without verification protocols in place. Insider threats from employees or contractors with excessive data access cause substantial losses when people mishandle information or depart with client lists.

Third-Party Risks Multiply Your Exposure

Third-party vendor risks compound the problem when service providers suffer breaches that create entry points into your network, yet most Los Angeles businesses lack contractual cybersecurity clauses requiring vendors to maintain basic protections. The reality is that these vulnerabilities cluster in small to medium-sized operations because they cannot afford dedicated security staff, yet they hold data equally attractive to attackers.

Understanding these specific threats matters because each one demands different coverage solutions. The next section outlines the cyber liability policies that address these gaps and protect your bottom line.

Coverage That Protects Your Bottom Line

First-Party and Third-Party Coverage Work Together

Cyber liability insurance splits into two distinct halves that work together to shield your Los Angeles business. First-party coverage reimburses your internal costs when a breach happens-forensic investigations, customer notification, regulatory compliance work, crisis management, and business interruption losses while systems recover. Third-party coverage addresses the liability you face when customers or regulators sue, covering legal defense, settlements, and regulatory fines that arise from the breach. Most LA businesses make a critical mistake by purchasing only one half, leaving massive gaps. A single incident triggers both types of exposure simultaneously, so you need both protections under one policy to avoid exhausting limits on the first claim and facing the second uninsured.

Sublimits Create Hidden Vulnerabilities

The coverage limits matter enormously because undersizing them creates false security. Small Los Angeles businesses typically start around $1,740 annually for basic cyber liability, but this often includes sublimits that devastate protection when needed most. Social engineering fraud coverage, for instance, frequently sits at only $50,000 to $100,000 within a $1,000,000 first-party limit, leaving a business that falls victim to wire-transfer fraud with minimal recovery. If an attacker tricks your accounting department into wiring $200,000 to a fraudulent vendor account, that $50,000 sublimit covers only a quarter of the loss.

Network security liability specifically protects against claims from third parties alleging your systems failed to protect their data, plus it covers your legal defense costs and any damages awarded-this protection stands separate from first-party breach response costs and remains non-negotiable for any business handling customer information.

Business Interruption and Regulatory Coverage

Business interruption coverage helps recoup lost income during a covered cyber event, which matters intensely because recovery timelines stretch weeks for ransomware incidents. A manufacturing firm losing production for 30 days faces exponential losses that notification costs never capture.

Healthcare providers in Los Angeles should demand explicit HIPAA penalties coverage because standard policies exclude regulatory fines, yet HIPAA violations carry penalties up to $1.5 million per violation category. California’s CCPA and CPRA laws similarly impose penalties that traditional coverage ignores, making privacy liability a mandatory add-on for any business operating in the state.

Declarations Pages Reveal Your True Protection

The declarations page reveals exactly what you purchased and what sublimits apply-this single document determines whether your coverage matches your actual risk or leaves you exposed. Many LA businesses never review their declarations carefully, discovering only after a breach that their ransomware coverage has a $250,000 sublimit or that social engineering fraud isn’t included at all.

Establishing a protocol to report incidents within 30 to 90 days of discovery matters because delays forfeit benefits entirely. Some carriers provide 24/7 breach response support and crisis management services as part of the policy, which accelerates recovery and preserves customer trust far more effectively than attempting incident response alone. These response resources help you navigate the complex steps required after a breach strikes, making the difference between a managed recovery and operational chaos.

Selecting the right provider requires more than comparing premium quotes-it demands understanding what each carrier actually covers and how they respond when your business faces a real incident.

How to Choose the Right Cyber Insurance Provider

Identify Your Specific Threats and Coverage Needs

Selecting a cyber insurance carrier demands more rigor than comparing premium quotes alone, because the cheapest policy often excludes the coverage you actually need. Start by identifying what specific threats your Los Angeles business faces, then verify that each carrier you evaluate covers those exact scenarios with adequate limits and minimal sublimits. A healthcare provider cannot accept a policy that excludes HIPAA penalties, just as a retailer handling payment cards cannot settle for a plan with ransomware incident recovery costs projected to exceed $265 billion annually by 2031.

Request declarations pages from every carrier before committing, then cross-reference the coverage against your actual data exposure. If you store 50,000 customer records and notification costs run $200 to $300 per record, you need first-party coverage exceeding $10 million, not $1 million. Most Los Angeles small businesses start around $1,740 annually for basic cyber liability, but undersizing limits to save $300 per year creates catastrophic exposure when a breach hits.

Evaluate Claims Response and Support Quality

Claims response separates carriers that genuinely help from those that delay and dispute. Contact each carrier’s claims department directly and ask how they respond to a ransomware incident-specifically, do they provide 24/7 breach response support, assign a dedicated adjuster, and offer crisis management resources immediately or only after investigation concludes? Carriers offering integrated incident response services including forensics, customer notification, and crisis management typically charge slightly higher premiums but accelerate recovery substantially, because these resources activate within hours rather than days.

Verify that the carrier holds an AM Best rating of A- VII or better, confirming financial strength to pay claims during industry-wide incidents when multiple businesses file simultaneously. This financial strength matters intensely because you need confidence that your carrier can actually pay when catastrophe strikes.

Leverage Security Controls to Reduce Premiums

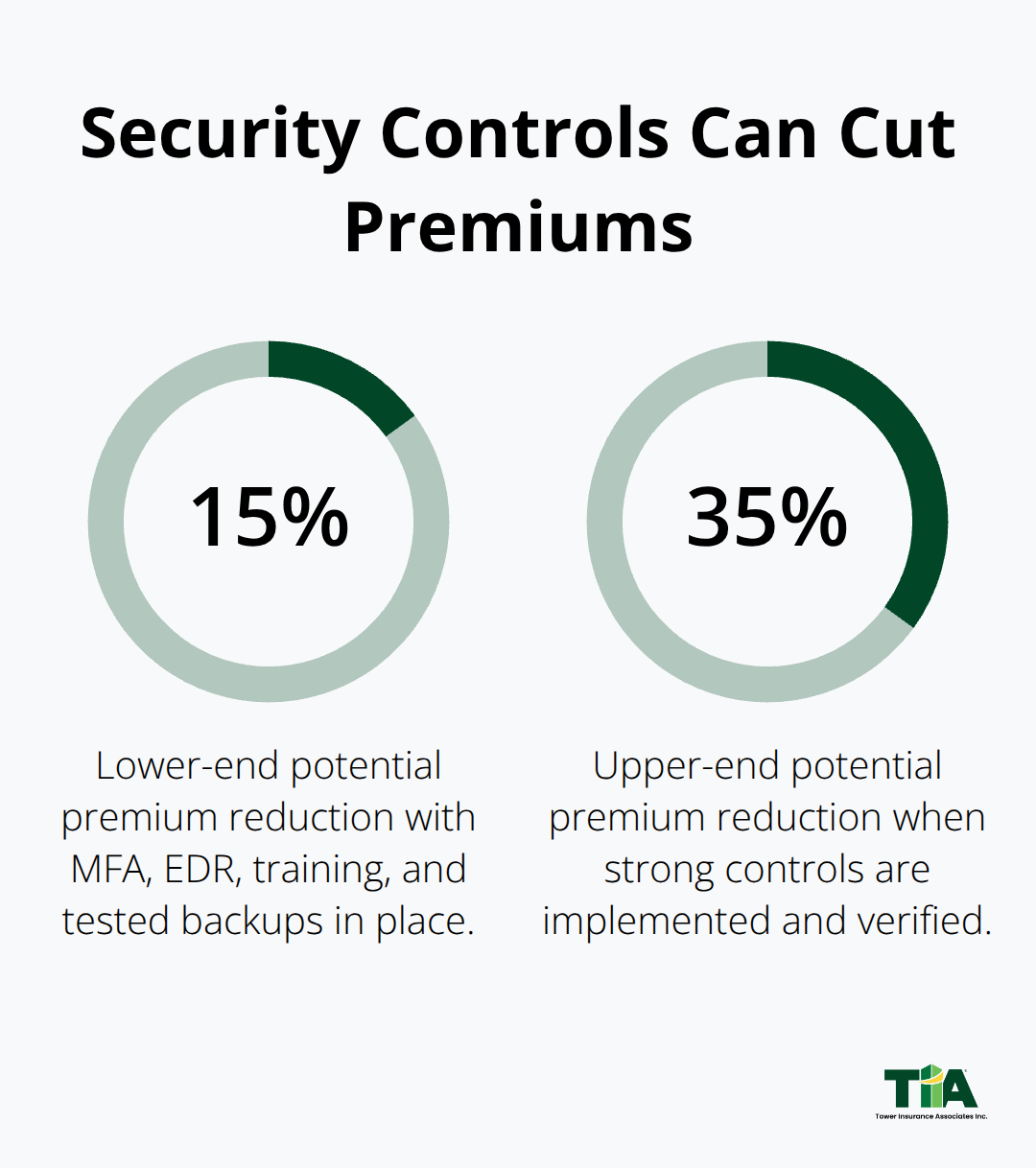

When comparing quotes, request premium breakdowns showing exactly what controls reduce your rate. Multi-factor authentication, endpoint detection and response, regular employee training, and tested backups can collectively reduce premiums by 15 to 35 percent, so investing in these controls before purchasing coverage lowers costs while strengthening protection.

This approach creates a win-win outcome: your business becomes more secure while your insurance costs drop.

An independent agency can match your specific risk profile against insurance quotes from multiple insurers rather than steering you toward a single option, and we advocate for you during claims rather than disappearing after the sale closes.

Final Thoughts

Los Angeles cyber coverage protects your business from threats that grow more sophisticated every year, yet most companies delay action until a breach forces their hand. Ransomware attacks cost $4.35 million on average, notification expenses run $200 to $300 per record, and regulatory fines under California’s CCPA and CPRA laws compound the damage substantially. First-party coverage reimburses your internal recovery costs while third-party coverage shields you from customer lawsuits and regulatory penalties, and you need both working together under a single policy to avoid exhausting limits on the first incident.

Selecting the right carrier demands more than comparing premiums alone. Review declarations pages carefully to confirm sublimits don’t cripple your protection, verify that coverage matches your specific threats, and confirm the carrier offers 24/7 breach response support that activates immediately when disaster strikes. Multi-factor authentication, endpoint detection, employee training, and tested backups reduce premiums by 15 to 35 percent while strengthening your defenses simultaneously (a combination that creates genuine competitive advantage).

We at Tower Insurance Associates, Inc. match your specific risk profile against multiple top-rated carriers to find Los Angeles cyber coverage that actually protects you rather than leaving gaps. Contact Tower Insurance Associates, Inc. to discuss your cyber coverage needs and receive a customized quote that reflects your actual exposure.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.