Your company’s leadership faces real legal and financial risks. Directors and officers can be personally liable for decisions made on behalf of the business, and California’s regulatory environment makes this threat especially serious.

At Tower Insurance Associates, Inc., we’ve seen firsthand how D&O liability protection California can shield your executives from devastating personal losses. The right policy covers legal defense costs, settlements, and judgments that could otherwise drain company resources or personal assets.

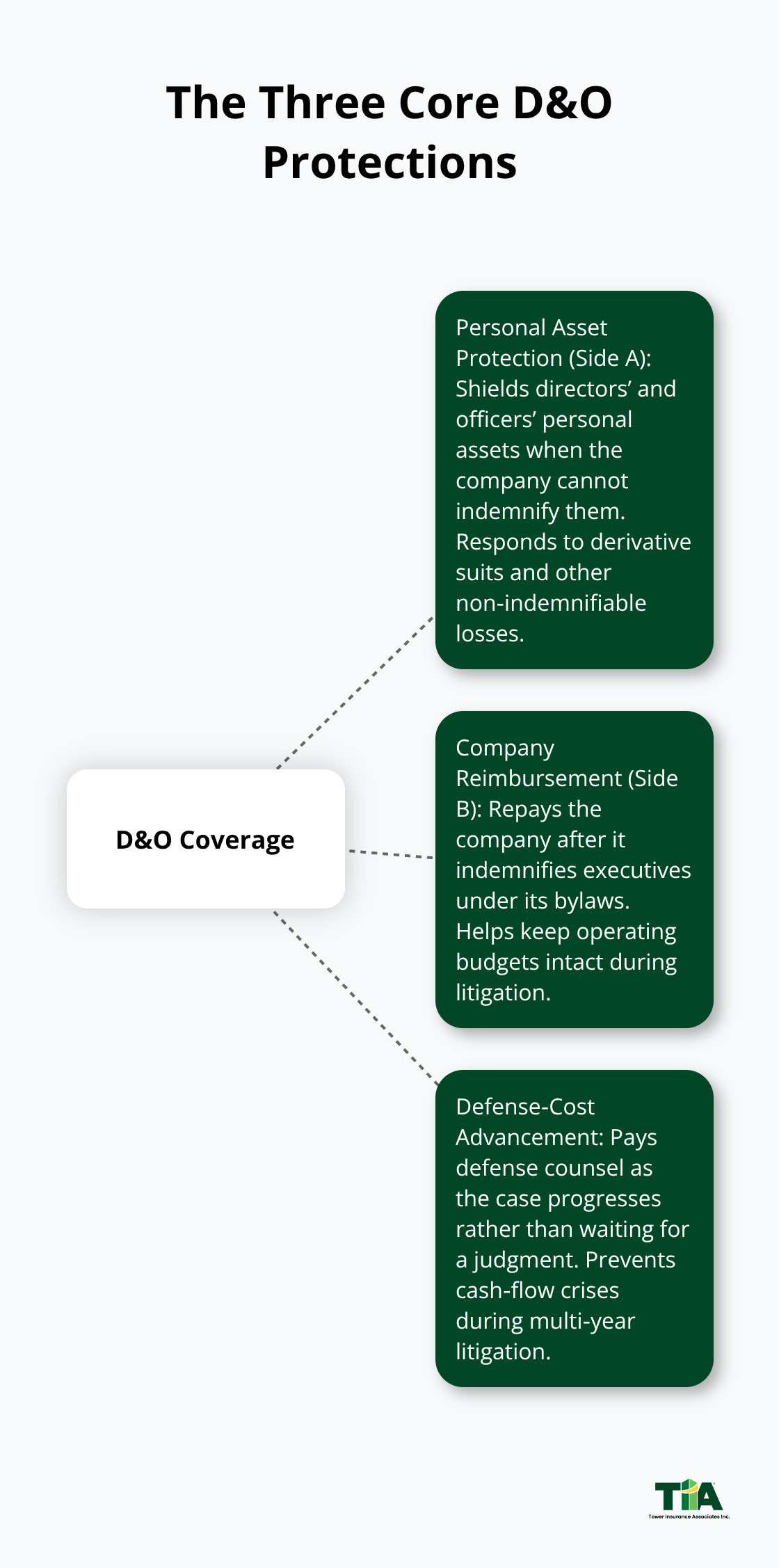

What D&O Coverage Actually Protects

D&O liability insurance in California provides for all the legal and defense costs in case of an accusation of deceitful and fraudulent practices against an executive. Most executives don’t fully understand these protections until they face a lawsuit.

Personal Asset Protection for Directors and Officers

The first protection covers your directors and officers personally. When a shareholder files a derivative action or an employee sues for wrongful termination tied to a board decision, the company often cannot indemnify the individuals involved. D&O steps in to cover defense costs and any judgments or settlements against the executive’s personal assets. California law under Civil Code § 5800 provides some statutory protection for volunteer HOA directors, but for-profit company executives get no such shield. A director facing a settlement without D&O insurance watches their personal savings disappear. This personal asset protection (called Side A coverage) has become more valuable in recent years because derivative actions now increasingly include monetary damages rather than just injunctive relief, expanding the non-indemnifiable exposure that Side A protects.

Company Reimbursement for Defense and Settlements

The second protection reimburses your company for defense expenses and settlements it pays on behalf of executives. When the company indemnifies a director or officer under its bylaws, D&O reimburses those costs so the company’s operating budget stays intact. This matters enormously in practice because most boards authorize indemnification in their governing documents, making D&O the financial backstop that prevents leadership decisions from draining operational resources.

Upfront Defense Cost Coverage

The third protection covers legal defense costs upfront, which is critical. Your company or the individual doesn’t wait for a settlement or judgment to get reimbursed-D&O insurers typically pay defense counsel directly as the case progresses, preventing cash-flow crises during multi-year litigation.

Claims That D&O Actually Covers

D&O covers negligence claims tied to supervision, poor record-keeping, failure to document board reports, and absence from critical meetings. It also covers embezzlement claims, breach of fiduciary duty, regulatory noncompliance, HR management failures, and misappropriation of intellectual property. Lawsuits between directors and officers within the same company are excluded, and if fraud is proven, the insured typically must repay defense costs. Criminal acts are excluded entirely.

Understanding the Coverage Gaps

California companies should understand that D&O policies contain specific exclusions that affect your protection strategy. If you need to evaluate whether your company’s current coverage aligns with your actual risk exposure, the next section examines how California’s unique regulatory and litigation landscape creates specific D&O needs that generic policies often miss.

Why California’s Regulatory Pressures Make D&O Essential

Climate Disclosure Requirements Drive Board Liability

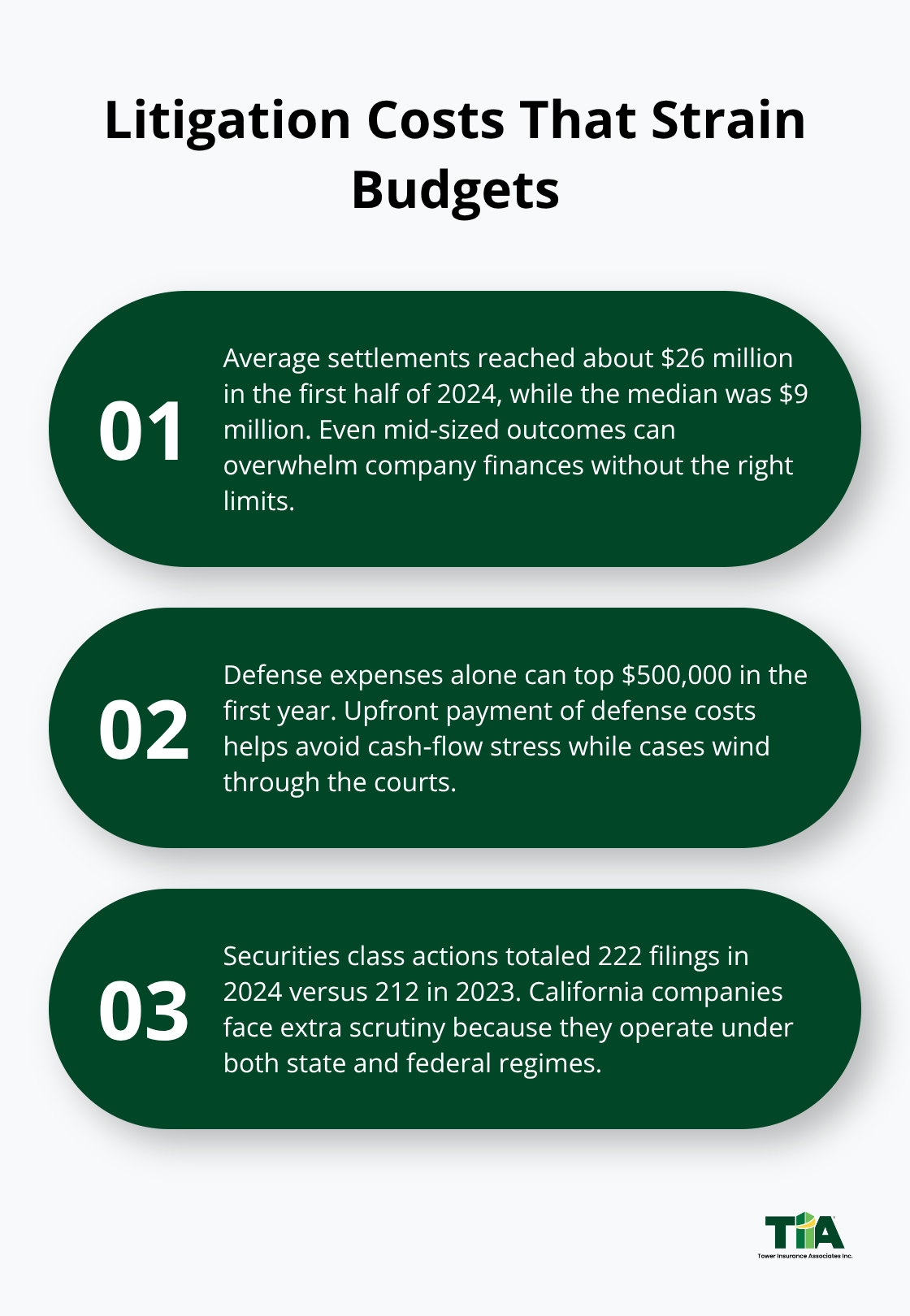

California’s regulatory environment creates direct, measurable exposure for company leadership that D&O insurance addresses head-on. The state imposes climate-disclosure requirements under SB 219 and SB 253 that demand executives disclose Scope 1 and 2 emissions with deadlines between 2025 and 2026, expanding the scope of board-level decisions that can trigger shareholder litigation. Securities class actions filed nationally totaled 222 in 2024, up from 212 in 2023, according to the WTW FINEX Observer, and California companies face heightened scrutiny because they operate under both state and federal disclosure regimes simultaneously. When a director or officer makes a misstep in climate reporting or governance disclosure, shareholders sue quickly.

Settlement Costs Exceed Most Company Budgets

The average settlement in these cases runs about $26 million in the first half of 2024, with a median of $9 million, which means even mid-sized claims devastate company finances and personal assets without proper coverage. California’s board diversity law added regulatory pressure that increases derivative-action risk, and activist investors now routinely target climate disclosures and governance practices. The cost of defending these claims alone-before any settlement or judgment-can exceed $500,000 in legal fees within the first year, money that drains operational budgets unless D&O coverage pays defense costs upfront.

Derivative Actions Now Include Monetary Damages

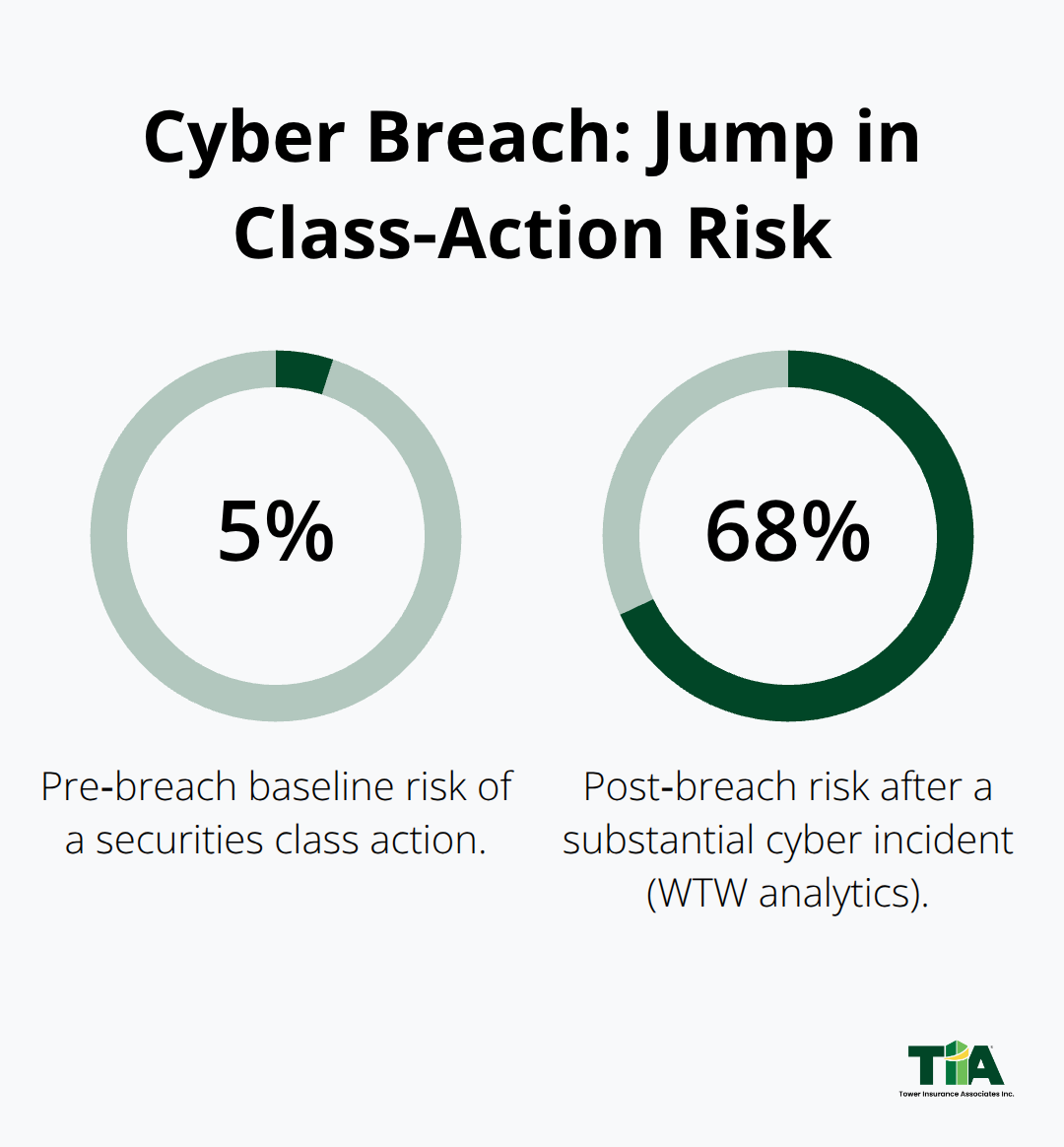

Shareholder and stakeholder litigation in California has shifted fundamentally in the past three years. Derivative actions now include monetary damages far more often than they did historically, meaning Side A personal-asset protection has become non-negotiable for directors and officers. Cyber incidents amplify this exposure dramatically: after a substantial breach, the risk of a securities class action rises from 5 percent to 68 percent according to WTW analytics, and boards face scrutiny over whether they implemented adequate controls or disclosed the incident timeline accurately.

Employee Litigation and Insolvency Risk

Employees increasingly file suits tied to board decisions on compensation, discrimination, and safety, and California’s pro-employee legal environment makes these claims harder to dismiss. When insolvency looms, directors face personal liability for unpaid wages and benefits, a threat that standard D&O coverage addresses directly. Bankruptcies rose to 22,762 filings in 2024, a roughly 33 percent year-over-year increase according to United States Courts data, and insolvency-related D&O claims follow. The practical reality is that California directors and officers cannot rely on company indemnification when the company faces financial distress, making Side A coverage the only genuine protection.

The True Cost of Uninsured Exposure

Without D&O insurance, a single shareholder lawsuit or regulatory investigation can cost your executives six figures in personal legal fees. That exposure grows every year as litigation becomes more frequent and settlements larger. The next section examines how to assess your company’s specific risk profile and select the right coverage limits to match your actual exposure.

Selecting the Right Coverage for Your Company’s Risk

Map Your Actual Exposure Before Shopping

Start by mapping your company’s actual exposure, not theoretical risk. The size of your board, the number of shareholders, your industry, and whether you’ve faced prior claims all determine what coverage you genuinely need. A 15-person board at a life sciences startup faces vastly different litigation risk than a 5-person board at a professional services firm, yet many companies purchase D&O policies based on what competitors carry rather than what their own operations demand.

We recommend conducting a structured risk assessment before shopping for quotes. List every regulatory filing your executives make, every employment decision that could trigger a wrongful-termination claim, every material transaction that shareholders might challenge, and every cyber vulnerability that could spark a breach-disclosure lawsuit. California companies operating under climate-disclosure requirements should specifically flag which executives own the emissions-reporting process and which board committees oversee climate governance. Document whether your company has faced shareholder activism, regulatory investigations, or prior employment litigation. This inventory becomes your underwriting foundation.

Evaluate Coverage Limits Against Real Settlement Data

Once you understand your actual exposure, evaluate coverage limits against settlement data. The average securities class action settlement in 2024 was $43 million, meaning a $10 million limit provides minimal protection for larger firms. However, smaller companies with 50 or fewer employees and no public shareholders often operate safely with $2 million to $5 million in limits.

The critical decision involves Side A personal-asset coverage, which protects directors and officers when the company cannot indemnify them. This limit should not sit subordinate to Side B reimbursement limits; if your Side A sits at $5 million but Side B claims consume $3 million, your executives face personal liability for claims above $2 million. Try selecting Side A limits that match or exceed your anticipated defense costs plus potential settlements. Defense costs alone in a shareholder derivative action typically reach $500,000 to $1.5 million before any judgment, making undersized limits dangerous.

Structure Deductibles and Retention Strategically

Deductibles and retention levels significantly impact both premium and practical protection. A $100,000 deductible reduces premium by roughly 15 to 25 percent compared to a $25,000 deductible, but forces your company to fund defense costs upfront until the deductible exhausts. For California companies facing cyber-related D&O exposure, this matters enormously because breach-response legal fees accumulate rapidly.

Try selecting a deductible your company can absorb without operational stress; if your annual cash reserves cannot cover three months of operations plus a $100,000 deductible, you’ve created hidden insolvency risk. This calculation prevents you from purchasing a policy that looks affordable on paper but strains your finances when a claim actually occurs.

Compare Policy Terms Across Multiple Carriers

Policy terms vary dramatically between carriers, and this variation drives outcome more than premium alone. Some insurers exclude coverage for claims arising from employment practices violations unless you purchased a separate employment-practices liability endorsement, while others include this coverage at no additional cost. Cyber-incident disclosure costs sit outside standard D&O at some carriers but bundle within the policy at others. California-specific climate-disclosure defense costs may or may not trigger coverage depending on how your policy defines covered claims.

Request sample policies from at least three carriers and have qualified counsel review the definitions of covered offense, defense-cost advancement procedures, and exclusion language. Ask specifically whether the policy covers defense costs for regulatory investigations by the California Attorney General or the SEC, and whether it covers costs to defend board minutes and governance documentation in shareholder litigation. Some carriers offer higher sublimits for specific exposure categories like cyber incidents or employment claims, which can provide targeted protection without inflating your overall limit.

Build Underwriter Relationships and Demonstrate Risk Management

Carriers differ in underwriting appetite; life sciences, cannabis, and cryptocurrency-adjacent businesses face capacity constraints, and newer entrants into the D&O market sometimes offer better terms for hard-to-place risks. Build relationships with underwriters before you need a renewal quote. Carriers respond more favorably to applications from companies that maintain robust board records, conduct regular cyber-risk assessments, and document governance improvements.

If your board lacks diversity or has high turnover, expect underwriters to ask detailed questions about recruitment and retention strategies. If your company has experienced a cyber incident, expect underwriters to request tabletop-exercise results and evidence that the board actively oversees IT controls. Respond promptly to underwriting questionnaires and provide documentation rather than vague assurances. This approach signals serious risk management and often yields better pricing and terms than companies that treat underwriting as a box-checking exercise.

Final Thoughts

D&O liability protection in California protects your leadership from devastating personal losses when shareholders or regulators file suit. The regulatory environment, settlement costs, and frequency of litigation make this coverage a core governance requirement, not a peripheral expense. Your directors and officers face real personal liability when the company cannot indemnify them, and California’s climate-disclosure mandates, board diversity pressures, and pro-employee legal landscape amplify that exposure every year.

Start with a structured risk assessment that maps your actual exposure rather than relying on industry benchmarks. Document your board size, shareholder base, regulatory obligations, and prior litigation history, then evaluate your coverage limits against real settlement data and ensure your Side A personal-asset protection matches your anticipated defense costs plus potential judgments. Structure your deductible at a level your company can absorb without operational strain, and compare policy terms across multiple carriers to identify exclusions that matter to your specific business.

At Tower Insurance Associates, Inc., we help California companies secure D&O coverage that matches their actual risk profile and budget constraints. Contact us to discuss your company’s specific exposure and receive a quote that reflects your real governance and litigation risk.

Disclaimer: This blog post is for general informational purposes only and does not represent actual coverage, policy terms, or legal requirements. Insurance details vary by individual and jurisdiction. Please consult a licensed insurance professional for advice specific to your situation.